We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Lowell Default Date

ScottishBarry

Posts: 6 Forumite

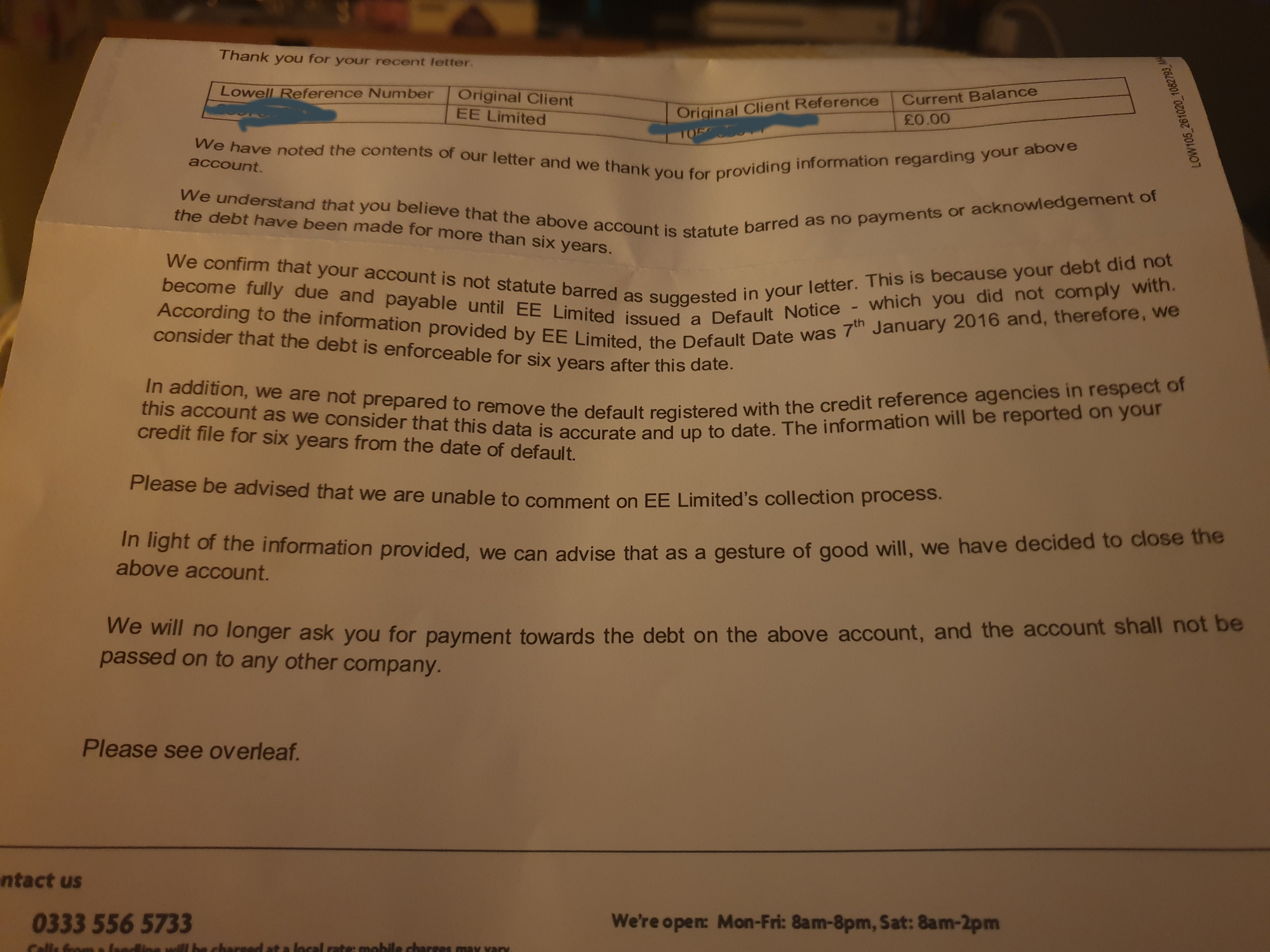

I put up a post a few months back regarding an alleged debt owed to Lowell Originally EE from September 2008.

I recieved a letter today that says Lowell will no longer be chasing the debt but is refusing to move the Default date.

What is my best course of action should I leave this now and wait until January 2022 until this is off my credit file or is there someone else I can complain to.

I have never acknowledged this debt in the letter they sent in May they gave me details of a phone contract that I took out years later. I have asked them to provide any payments or acknowledgements from September 2008 to March 2015 they have ignored this in every letter.

Any help would be fantastic

I recieved a letter today that says Lowell will no longer be chasing the debt but is refusing to move the Default date.

What is my best course of action should I leave this now and wait until January 2022 until this is off my credit file or is there someone else I can complain to.

I have never acknowledged this debt in the letter they sent in May they gave me details of a phone contract that I took out years later. I have asked them to provide any payments or acknowledgements from September 2008 to March 2015 they have ignored this in every letter.

Any help would be fantastic

0

Comments

-

Wasn't aware the Samsung Galaxy S5 was available in September 2008!0

-

Yeah I know the details in the letter from april was from a contract that was took out in 2014. They have never told me what phone I took in 2008 what was the monthly payments, I have no idea how a phone contract in 2008 would be anywhere near £1200.0

-

Your off the hook, i`d be grateful and leave it at that.

I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter0 -

The last payment was August 2015, default was issued within 6 months, nothing to be done about that. Just see the default out and be happy it's essentially gone.0

-

So I should just accept that they have offered no proof that any payment was made between 2008 and August 2015.ldhme said:The last payment was August 2015, default was issued within 6 months, nothing to be done about that. Just see the default out and be happy it's essentially gone.0 -

It says it was part of their findings, my point was that if they have proof that was the last payment (although this should be visible on your credit report if your EE account is still on there) then the default would be correct.ScottishBarry said:

So I should just accept that they have offered no proof that any payment was made between 2008 and August 2015.ldhme said:The last payment was August 2015, default was issued within 6 months, nothing to be done about that. Just see the default out and be happy it's essentially gone.

If you want to challenge their findings and have them provide this proof then that is of course something you can do.

Is it worth it though? Considering that you have to get a final decision letter off them stating they won't move the default date. Then you'll have to escalate the complaint to the Ombudsman during CoVid and wait 4 months for it to be assigned to a case handler. Then they BEGIN the investigation, who knows how long that could take, a month maybe, how long has it taken you to get this far. Then IF they side with you, they will be instructed to move the default date within 28 days. Then it can take up to 8 weeks for the CRA's to update this info.

So in reality if it goes your way the default will be removed from your file 6 months early at best. As it stands they've settled the account and said they will not chase you for the debt, so at this point you are the one who is potentially appearing unreasonable (in their eyes) if you were to go ahead with this.

It won't cost you anything other than time though so it's up to you.0 -

Making payments or not to an account has nothing to do with the account actually being recorded as defaulted on your credit file.The issue of a default is entirely at the discretion of the lender, accounts can go dormant for years without a default been issued.Guidelines state a default can be registered after between 3/6 missed contractural payments, it does not state they have to default you, but it is concidered good practice to do so.The complaints process can be a long one, as said above, I believe its the ICO who would deal with such matters regarding credit files, you have had a good result thus far, it won`t cost you anything to continue, but it might take a while.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.8K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards