We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Mortgage overpayment question

I currently have a mortgage with NatWest which I took out a five year fixed deal at 2.9%. I am just over a year into the mortgage and I have made a lump sum overpayment of 10%. I thought making an overpayment would reduce the time on my mortgage and I would just carry on paying my usual monthly payments. I’ve had a letter saying that they will be reducing my monthly payments so I will still have the same amount of time left on my mortgage. I have just spoke to NatWest who told me that if I wanted to carry on paying my regular payments I would need to apply for a new mortgage with them. Could anybody tell me if this is correct and if it is what’s the best way of me paying off my mortgage earlier. I know whilst I’m in the 5 year deal there would be a penalty to pay if I paid it all in 1 lump sum. I was going to pay the 10% I’m allowed each year and the balance at the end of the 5 years so I don’t pay any penalties. But by them only reducing my monthly payments i think I will not only pay more as a lump sum each year but also pay more at the end.

Should I just save the extra money I would have paid and use it for my overpayment next year?

Hope all this makes sense?

Comments

-

The problem is as you have done the 10% if you keep the payment the same that is more overpayments, not all lenders allow those, if you want to keep the payments the same you have to reduce the term which requires the mortgage to go through validation again.

The reality is it makes a tiny difference to the amount of extra interest you pay.

The real term is determined by the payments not the contractual term which just sets a contractual payment

On 2.9% over 20 years

per 100k with a 10% overpayment the extra interest is just under £9 in the first yearamount rate payment owing interest £100,000.00 2.90% £549.60 £96,255.23 £2,850.49 £90,000.00 2.90% £494.64 £86,629.70 £2,565.44 £90,000.00 2.90% £549.60 £85,961.40 £2,556.60

Just save the difference(£660) and add it to the other saving to do the next 10%0 -

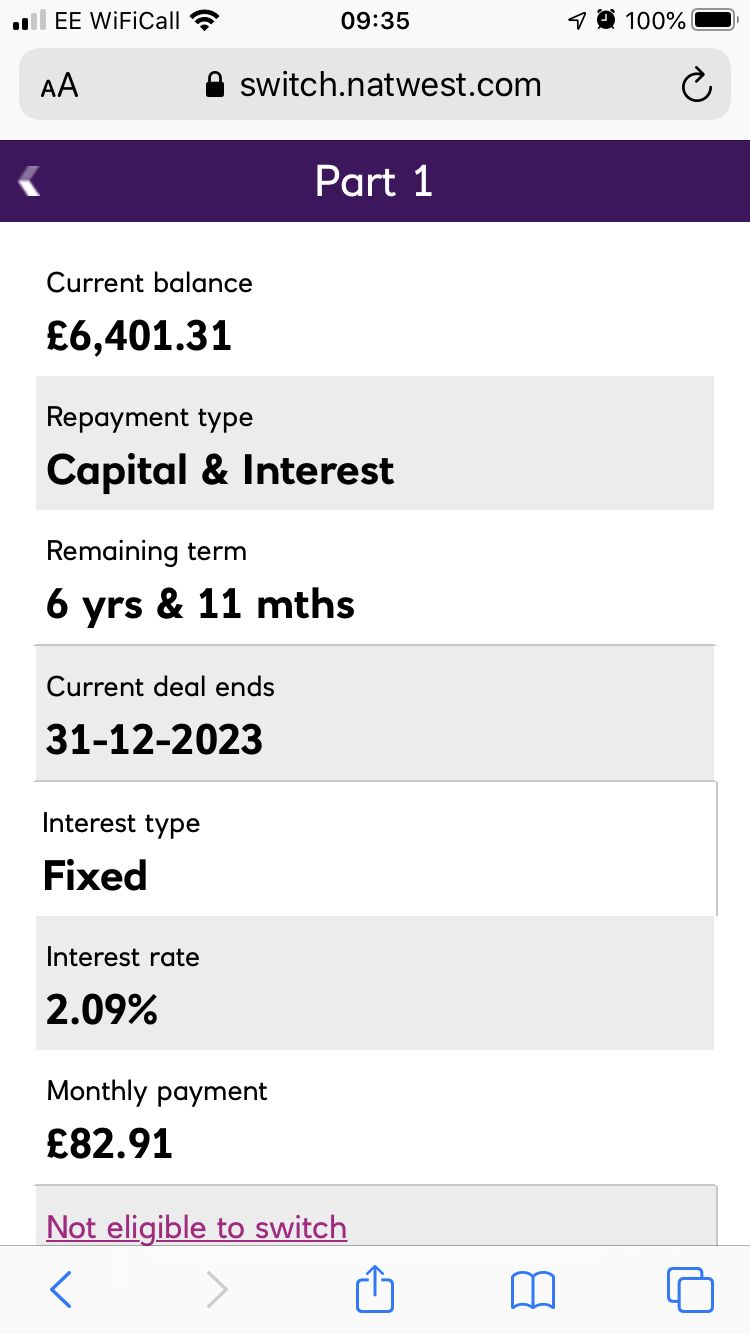

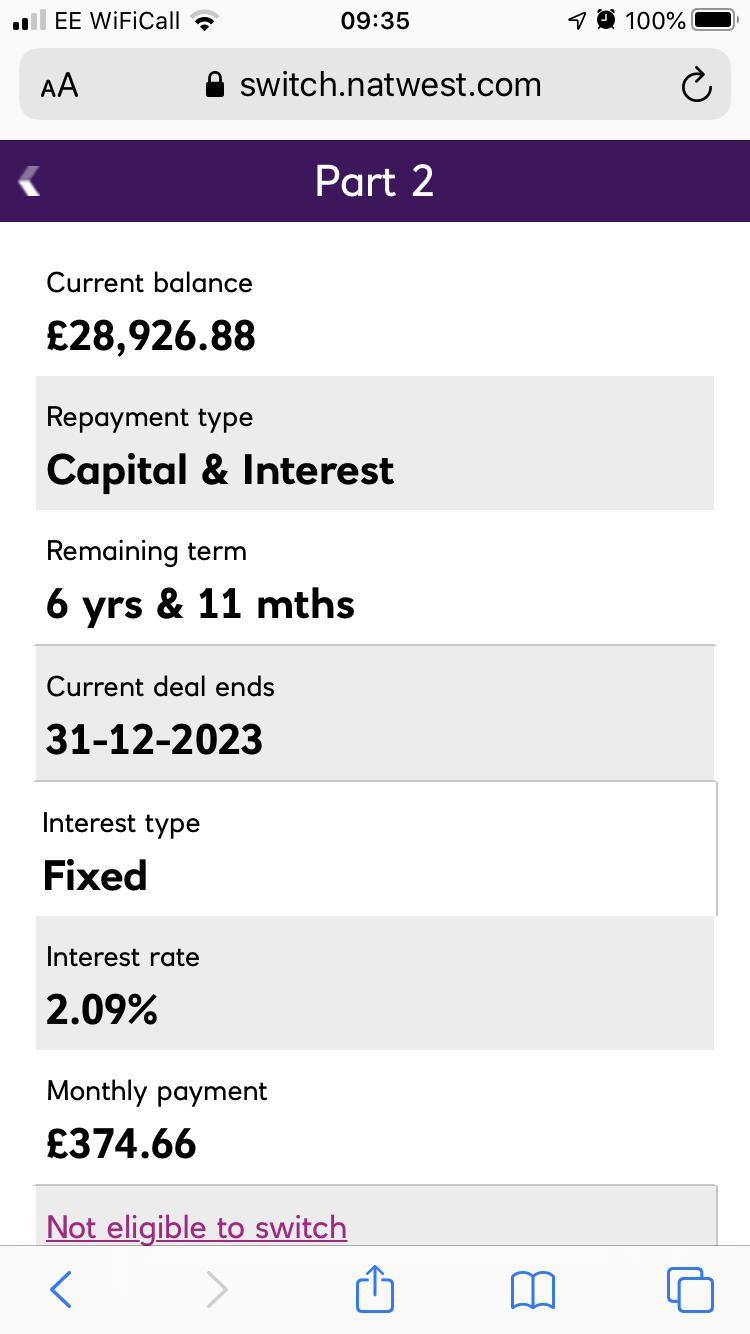

Thanks for the info. I currently have 6 years 11 months remaining on my mortgage which I am currently paying 2.9%.I owed approx £38190.00 which I paid £3819.00 as a lump sum earlier this month. It’s changed my payments from £511.00 per month to £454.00 per month. As I said I will be paying 10% each year until my deal comes to an end in January 2024 which I will then pay the balance.Should I just save the £57.00 difference each month or look at amending the terms (and is this an easy process).

Thanks again0 -

Put the £57 aside and use the money to overpay again at the earliest opportunity.1

-

What is your LTV?

that rate is very high for a 5y taken out only a year ago.0 -

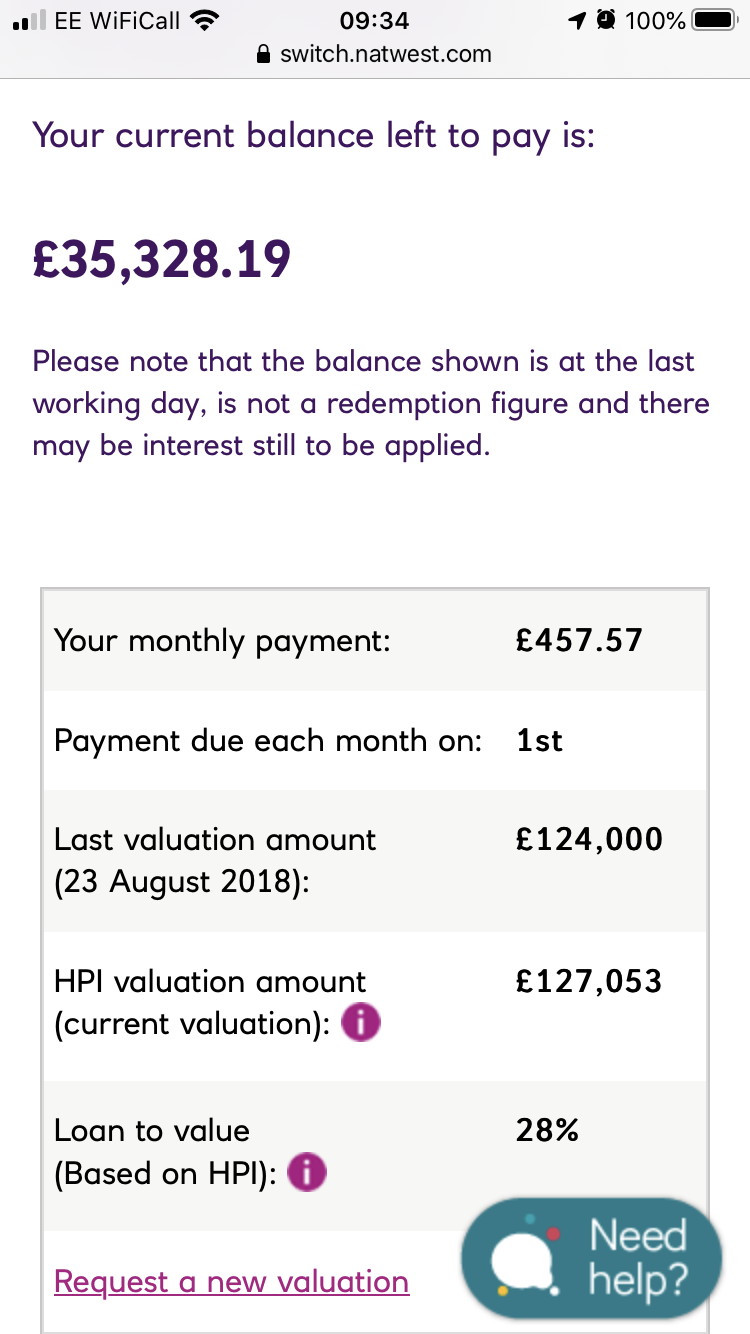

Sorry getmore4less you’re correct it’s 2.09%. When I took it out it in September 2018 my house was valued at £130,000 and we took out a £50,000 mortgage. We now owe £35,328.00 with our overpayments taken into account. We are in the position where we could pay it off in full if we wanted to but I don’t like paying any unnecessary fees like the early repayment charges so was looking for the best way to pay it back without charges.getmore4less said:What is your LTV?

that rate is very high for a 5y taken out only a year ago.

Thanks0 -

What's the ERC now?0

-

If you can pay it all off now - would the ERC be less than paying the interest for 5 years?1

-

When considering paying it off early, you will minimise your losses by doing so immediately after the anniversary of the initial advance when the ERC will be lower.0

-

your numbers don't look right. for 6y 11m full term and 2.09%

6y 11months 2.09% before and after the 10%calvr1ch said:Thanks for the info. I currently have 6 years 11 months remaining on my mortgage which I am currently paying 2.9%.I owed approx £38190.00 which I paid £3819.00 as a lump sum earlier this month. It’s changed my payments from £511.00 per month to £454.00 per month. As I said I will be paying 10% each year until my deal comes to an end in January 2024 which I will then pay the balance.Should I just save the £57.00 difference each month or look at amending the terms (and is this an easy process).

Thanks againamount rate payment owing interest £38,190.00 2.09% £494.58 £33,003.74 £748.68 £34,371.00 2.09% £445.12 £29,703.36 £673.81 £34,371.00 2.09% £494.58 £29,104.13 £668.09

~£6 difference in interest and a payment difference of ~£50

but you now say

We now owe £35,328.00 with our overpayments taken into account

where has the extra £1k come from

When does your ERC drop to 3%? (then 2%, then 1%)

you can get savings products over 1.09% so unlikely paying it all of and paying the ERC will be better than just running the deal to the end with max ERC free overpayments.0 -

My ERC drops to 3% in January then it drops 1% every January onward. Sorry I have just been estimating figures. Below is screen shots of my account.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards