We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

750k Drawdown at 58

Comments

-

You can certainly create a robust retirement plan where the retiree understands what they can spend and what might need to be adjusted (and how this will be done) if poor market outcomes are experienced and the chances (given historical outcomes) that this might happen.SouthCoastBoy said:You have asked the question nobody can really answer. It is one of the main disadvantages of a DC scheme, there will always be a risk of running out of money. Personally I have modelled 3.5% growth rate, inflation at 2.5%, and then projected out on a yearly basis until I am 90. Then alter the variables and understand the impact. Ultimately all guesswork, nobody can guarantee anything. I think the key is to be flexible and have a cash reserve so you never draw down to 0. One thing I have noticed, with inlaws and my mother, is that when you get to post 80 the amount of required disposable income appears to decrease, so drawdown may not necessarily be linear. Also if you plan to give/leave money to kids etc. maybe do it earlier rather than later (not advice, just a thought) as if you go into a home all assets could be potentially swallowed up in care home fees. Unfortunately my mum has dementia and is now in a care home so we have first hand experience of this. Same happened to my grand parents.

https://www.kitces.com/sample-withdrawal-policy-statement-wps-from-jon-guyton/

If you are modelling this in a sheet you might want to think about non-linear returns, especially in early retirement.

0 -

Not sure that historic US centric outcomes are of value at the current time for a whole variety of reasons.BritishInvestor said:

You can certainly create a robust retirement plan where the retiree understands what they can spend and what might need to be adjusted (and how this will be done) if poor market outcomes are experienced and the chances (given historical outcomes) that this might happen.SouthCoastBoy said:You have asked the question nobody can really answer. It is one of the main disadvantages of a DC scheme, there will always be a risk of running out of money. Personally I have modelled 3.5% growth rate, inflation at 2.5%, and then projected out on a yearly basis until I am 90. Then alter the variables and understand the impact. Ultimately all guesswork, nobody can guarantee anything. I think the key is to be flexible and have a cash reserve so you never draw down to 0. One thing I have noticed, with inlaws and my mother, is that when you get to post 80 the amount of required disposable income appears to decrease, so drawdown may not necessarily be linear. Also if you plan to give/leave money to kids etc. maybe do it earlier rather than later (not advice, just a thought) as if you go into a home all assets could be potentially swallowed up in care home fees. Unfortunately my mum has dementia and is now in a care home so we have first hand experience of this. Same happened to my grand parents.

https://www.kitces.com/sample-withdrawal-policy-statement-wps-from-jon-guyton/

If you are modelling this in a sheet you might want to think about non-linear returns, especially in early retirement.1 -

Each year take out 100/(100 - age) % of that year's start fund value.Thrugelmir said:

Not sure that historic US centric outcomes are of value at the current time for a whole variety of reasons.BritishInvestor said:

You can certainly create a robust retirement plan where the retiree understands what they can spend and what might need to be adjusted (and how this will be done) if poor market outcomes are experienced and the chances (given historical outcomes) that this might happen.SouthCoastBoy said:You have asked the question nobody can really answer. It is one of the main disadvantages of a DC scheme, there will always be a risk of running out of money. Personally I have modelled 3.5% growth rate, inflation at 2.5%, and then projected out on a yearly basis until I am 90. Then alter the variables and understand the impact. Ultimately all guesswork, nobody can guarantee anything. I think the key is to be flexible and have a cash reserve so you never draw down to 0. One thing I have noticed, with inlaws and my mother, is that when you get to post 80 the amount of required disposable income appears to decrease, so drawdown may not necessarily be linear. Also if you plan to give/leave money to kids etc. maybe do it earlier rather than later (not advice, just a thought) as if you go into a home all assets could be potentially swallowed up in care home fees. Unfortunately my mum has dementia and is now in a care home so we have first hand experience of this. Same happened to my grand parents.

https://www.kitces.com/sample-withdrawal-policy-statement-wps-from-jon-guyton/

If you are modelling this in a sheet you might want to think about non-linear returns, especially in early retirement.

So at age 60 take 2.50%, at age 70 take 3.33% and at age 80 take 5.00%.

As good a plan as anything else. 😀1 -

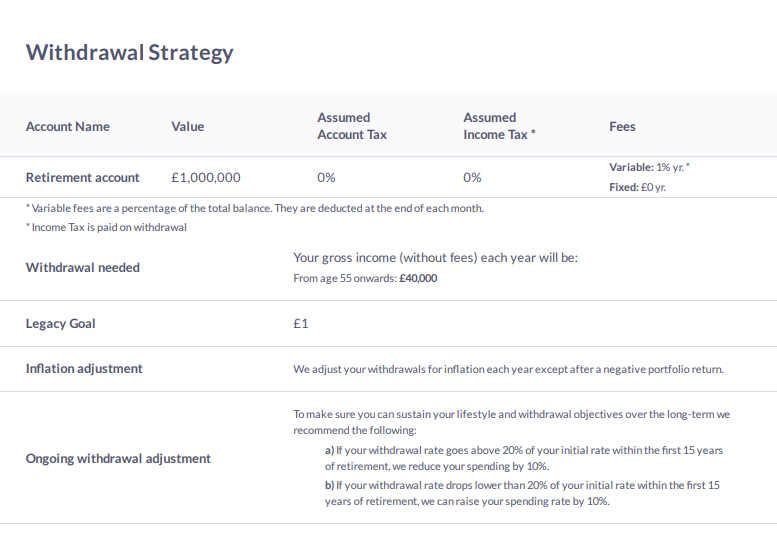

Given that a 40 year plan using UK investments can sustain 5.5% before costs and perhaps 5% after them (the effect varies in the studies) if the Guyton-Klinger rules are used, 5% isn't high. That's based on historic UK sequences in Abraham Okusanya's study The golden rule: working out a safe withdrawal rate and 65% equities. The choice of withdrawal rules matters a lot. 5% is too high for constant inflation-adjusted income, the 4% rule, where 3.2% after allowing for costs is more like it.garmeg said:It is a 25% greater drawdown than the oft-quoted 4% safe withdrawal rate which in itself is a bit toppy at age 58.

I am 56 and retiring soon with a much smaller SIPP. I wouldn't take 4% as drawdown let alone 5%. I would have to think very hard about how much to actually take. More research needed by myself I think.

Drawdown: safe withdrawal rates introduces the research into how much can safely be withdrawn. Short term you can go higher safely if you're doing something like paying yourself the state pension before it starts, that then being cut back when it does.

0 -

I'd say that's exactly the wrong way round, for multiple reasons.garmeg said:

Each year take out 100/(100 - age) % of that year's start fund value.Thrugelmir said:

Not sure that historic US centric outcomes are of value at the current time for a whole variety of reasons.BritishInvestor said:

You can certainly create a robust retirement plan where the retiree understands what they can spend and what might need to be adjusted (and how this will be done) if poor market outcomes are experienced and the chances (given historical outcomes) that this might happen.SouthCoastBoy said:You have asked the question nobody can really answer. It is one of the main disadvantages of a DC scheme, there will always be a risk of running out of money. Personally I have modelled 3.5% growth rate, inflation at 2.5%, and then projected out on a yearly basis until I am 90. Then alter the variables and understand the impact. Ultimately all guesswork, nobody can guarantee anything. I think the key is to be flexible and have a cash reserve so you never draw down to 0. One thing I have noticed, with inlaws and my mother, is that when you get to post 80 the amount of required disposable income appears to decrease, so drawdown may not necessarily be linear. Also if you plan to give/leave money to kids etc. maybe do it earlier rather than later (not advice, just a thought) as if you go into a home all assets could be potentially swallowed up in care home fees. Unfortunately my mum has dementia and is now in a care home so we have first hand experience of this. Same happened to my grand parents.

https://www.kitces.com/sample-withdrawal-policy-statement-wps-from-jon-guyton/

If you are modelling this in a sheet you might want to think about non-linear returns, especially in early retirement.

So at age 60 take 2.50%, at age 70 take 3.33% and at age 80 take 5.00%.

As good a plan as anything else. 😀1. Typically you want more money at an earlier age, this does the opposite.

2. It takes no account of SP kicking in when the amount taken could decline.

3. It's too simple (see my sig). Better a base amount to cover living costs and then a variable amount based on need, want , previous growth or decline.4 -

My point was more around the WPS rather than the numbers contained within. I use global data from a UK POV but the WPS logic/format is still valid:Thrugelmir said:

Not sure that historic US centric outcomes are of value at the current time for a whole variety of reasons.BritishInvestor said:

You can certainly create a robust retirement plan where the retiree understands what they can spend and what might need to be adjusted (and how this will be done) if poor market outcomes are experienced and the chances (given historical outcomes) that this might happen.SouthCoastBoy said:You have asked the question nobody can really answer. It is one of the main disadvantages of a DC scheme, there will always be a risk of running out of money. Personally I have modelled 3.5% growth rate, inflation at 2.5%, and then projected out on a yearly basis until I am 90. Then alter the variables and understand the impact. Ultimately all guesswork, nobody can guarantee anything. I think the key is to be flexible and have a cash reserve so you never draw down to 0. One thing I have noticed, with inlaws and my mother, is that when you get to post 80 the amount of required disposable income appears to decrease, so drawdown may not necessarily be linear. Also if you plan to give/leave money to kids etc. maybe do it earlier rather than later (not advice, just a thought) as if you go into a home all assets could be potentially swallowed up in care home fees. Unfortunately my mum has dementia and is now in a care home so we have first hand experience of this. Same happened to my grand parents.

https://www.kitces.com/sample-withdrawal-policy-statement-wps-from-jon-guyton/

If you are modelling this in a sheet you might want to think about non-linear returns, especially in early retirement.

0 -

For me (and I have no qualification or experience in this field) I break things down into 3 distinct parts and create mini 'pots' from there.

I plan to retire in 12 years at 50. I will be mortgage free.

Part 1. 50 to 67 (no state pension) I want £30k per year before tax.

£30k X 17 years = £510k

Pot 2. I still want £30k gross per year but I now have the state pension so from 67 -80 I need to contribute £21k of my own money to get to £30k.

£21k X 13 years = £273k

Pot 3. 80 to 85 £26k will be enough for me. State pension plus £17k of my money. After 85 my spends will be nominal and house downsizing will be an option if I'm not dead.

£17k X 5 = £85k

All 3 pots added together = £868k

I have kept things simple and based all figures on my investment returns equaling inflation no better which I think is a safe way of doing things.

Simple, yes, crude , undoubtedly but I'm happy with my formula.

Obviously my numbers are in today's prices, 12 years later the pot size and annual drawdown would need to be more due to inflation between now and then.

For the OP or anyone in the verge of retirement I believe my way makes sense.1 -

I think you'd need to be very happy with potential the cuts in real income if using Guyton-Klinger and if a poor series of returns was encountered in early retirement, especially if the guardrails were applied annually.jamesd said:

Given that a 40 year plan using UK investments can sustain 5.5% before costs and perhaps 5% after them (the effect varies in the studies) if the Guyton-Klinger rules are used, 5% isn't high. That's based on historic UK sequences in Abraham Okusanya's study The golden rule: working out a safe withdrawal rate and 65% equities. The choice of withdrawal rules matters a lot. 5% is too high for constant inflation-adjusted income, the 4% rule, where 3.2% after allowing for costs is more like it.garmeg said:It is a 25% greater drawdown than the oft-quoted 4% safe withdrawal rate which in itself is a bit toppy at age 58.

I am 56 and retiring soon with a much smaller SIPP. I wouldn't take 4% as drawdown let alone 5%. I would have to think very hard about how much to actually take. More research needed by myself I think.

Drawdown: safe withdrawal rates introduces the research into how much can safely be withdrawn. Short term you can go higher safely if you're doing something like paying yourself the state pension before it starts, that then being cut back when it does.2 -

I’m with AnotherJoe on this. Whilst that sounds a nice simple mathematical formula, in my mind, it misses the point of retirement. I also suspect there is a huge amount of truth in the 3 phases of retirement - go-go, slow-go and no-go.AnotherJoe said:

I'd say that's exactly the wrong way round, for multiple reasons.garmeg said:

Each year take out 100/(100 - age) % of that year's start fund value.Thrugelmir said:

Not sure that historic US centric outcomes are of value at the current time for a whole variety of reasons.BritishInvestor said:

You can certainly create a robust retirement plan where the retiree understands what they can spend and what might need to be adjusted (and how this will be done) if poor market outcomes are experienced and the chances (given historical outcomes) that this might happen.SouthCoastBoy said:You have asked the question nobody can really answer. It is one of the main disadvantages of a DC scheme, there will always be a risk of running out of money. Personally I have modelled 3.5% growth rate, inflation at 2.5%, and then projected out on a yearly basis until I am 90. Then alter the variables and understand the impact. Ultimately all guesswork, nobody can guarantee anything. I think the key is to be flexible and have a cash reserve so you never draw down to 0. One thing I have noticed, with inlaws and my mother, is that when you get to post 80 the amount of required disposable income appears to decrease, so drawdown may not necessarily be linear. Also if you plan to give/leave money to kids etc. maybe do it earlier rather than later (not advice, just a thought) as if you go into a home all assets could be potentially swallowed up in care home fees. Unfortunately my mum has dementia and is now in a care home so we have first hand experience of this. Same happened to my grand parents.

https://www.kitces.com/sample-withdrawal-policy-statement-wps-from-jon-guyton/

If you are modelling this in a sheet you might want to think about non-linear returns, especially in early retirement.

So at age 60 take 2.50%, at age 70 take 3.33% and at age 80 take 5.00%.

As good a plan as anything else. 😀1. Typically you want more money at an earlier age, this does the opposite.

2. It takes no account of SP kicking in when the amount taken could decline.

3. It's too simple (see my sig). Better a base amount to cover living costs and then a variable amount based on need, want , previous growth or decline.

I believe we will (notwithstanding Covid!) want to do and travel more in our late 50s to 60s. Less in our 70s, and perhaps almost none from mid-80s on. Based on what we have seen around us.Accordingly, there may be a need for 5% withdrawals for some time (we have other smaller DB pots to help reduce that, kicking in at different times). The ability to “tighten belts” will be a feature of our plans where needed.

Biggest risk to that, as BritishInvestor suggests, is the SOR, and having Covid apply some pressure early on is perhaps a good thing from that viewpoint (every cloud, eh!).

I’m with Billy2Shots on the logic of differing amounts....I use a spreadsheet modelling to allow me to factor in those differing amounts, include inflation and also to show our different pots kicking in (including State pension). I don’t think of them as differing pots, but do model dropping one needs a few times over the periods from mid-50s to an optimistic century.

Oh, and on the side issue of inheritance, one goal I have is for us to trickle money to ours throughout by slipping regular money to their ISAs and pension pots. Maybe they can benefit from the magic of compounding.If, as I hope, we might live long and fruitful retirements, ours might be in their 50s or even 60s when we pop our clogs. Nicer for them to have enjoyed some of the money whilst we are around to try to help guide them to wisely using (mostly saving!) it, rather than be suddenly left with a lump at a time when they too are old and grey!!Plan for tomorrow, enjoy today!0 -

garmeg said:

Each year take out 100/(100 - age) % of that year's start fund value.Thrugelmir said:

Not sure that historic US centric outcomes are of value at the current time for a whole variety of reasons.BritishInvestor said:

You can certainly create a robust retirement plan where the retiree understands what they can spend and what might need to be adjusted (and how this will be done) if poor market outcomes are experienced and the chances (given historical outcomes) that this might happen.SouthCoastBoy said:You have asked the question nobody can really answer. It is one of the main disadvantages of a DC scheme, there will always be a risk of running out of money. Personally I have modelled 3.5% growth rate, inflation at 2.5%, and then projected out on a yearly basis until I am 90. Then alter the variables and understand the impact. Ultimately all guesswork, nobody can guarantee anything. I think the key is to be flexible and have a cash reserve so you never draw down to 0. One thing I have noticed, with inlaws and my mother, is that when you get to post 80 the amount of required disposable income appears to decrease, so drawdown may not necessarily be linear. Also if you plan to give/leave money to kids etc. maybe do it earlier rather than later (not advice, just a thought) as if you go into a home all assets could be potentially swallowed up in care home fees. Unfortunately my mum has dementia and is now in a care home so we have first hand experience of this. Same happened to my grand parents.

https://www.kitces.com/sample-withdrawal-policy-statement-wps-from-jon-guyton/

If you are modelling this in a sheet you might want to think about non-linear returns, especially in early retirement.

So at age 60 take 2.50%, at age 70 take 3.33% and at age 80 take 5.00%.

As good a plan as anything else. 😀Hmmm - Mrs Notepad's mum is 96, now how much money should she be taking out...0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.6K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.7K Work, Benefits & Business

- 603.2K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards