We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

The Government and Pension Protection fund are keeping 43 years of my fathers pension investment.

Lisa2108

Posts: 4 Newbie

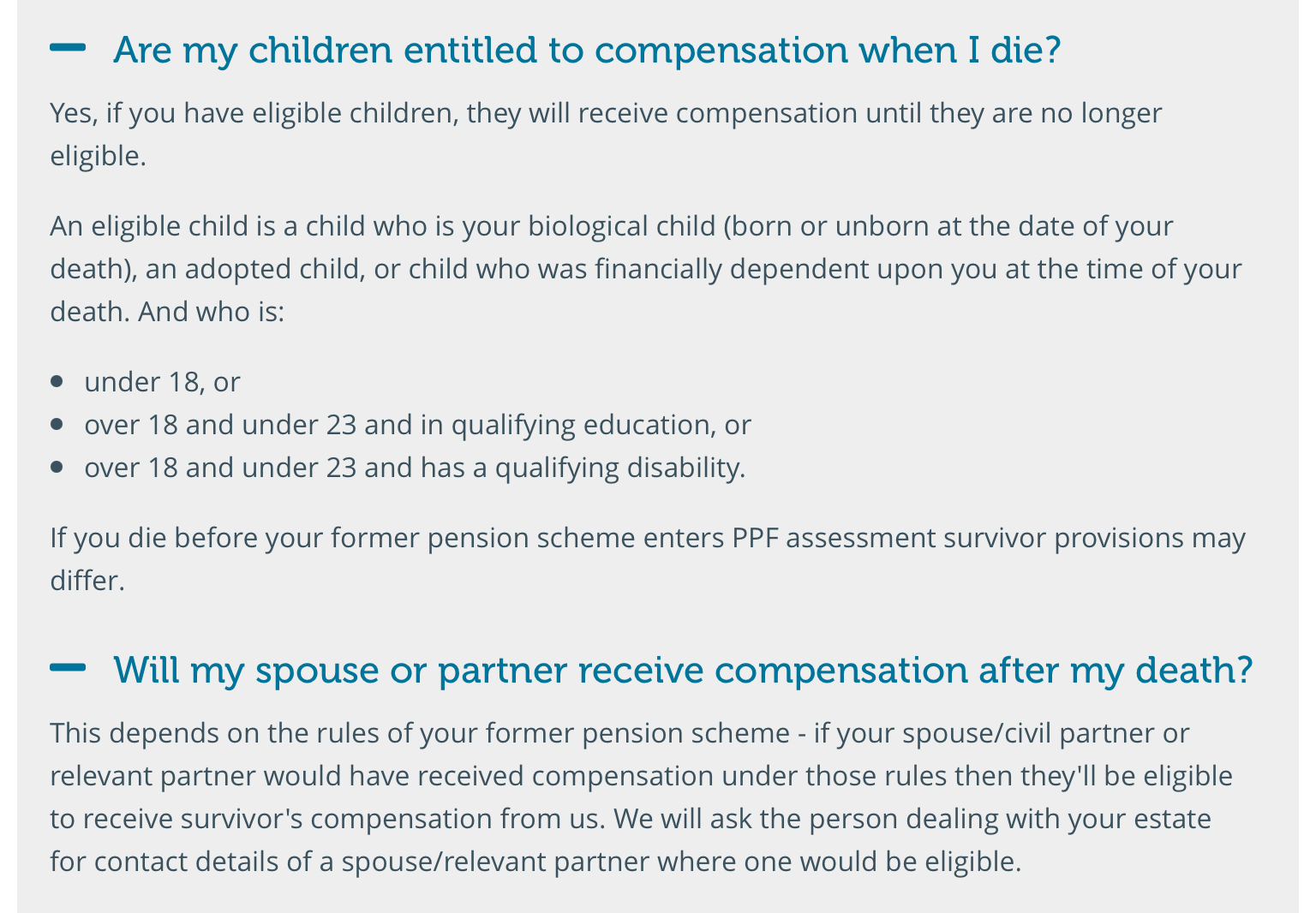

I am looking for people who have had and experience dealing with the pension protection fund, they have frozen my fathers pension benefits and now are expecting to keep over 43 years of his investment to themselves because he was not married and did not have children under the age of 21 in full time education.

My father worked for the same company all his life from the age of 19 until he was made redundant 43 years later.

He passed away at 62, 2 years into his pension, he had a death benefit on his pension, but the PPF wont pay it out.

Iv pleaded with the Government and the PPF to advise this cant be right, but they are not interested and are leaving the blame with each other.

Im ready to take legal action against them but would be good to know of anyone else who has had any bad experiences dealing with them.

Thank you LIsa

My father worked for the same company all his life from the age of 19 until he was made redundant 43 years later.

He passed away at 62, 2 years into his pension, he had a death benefit on his pension, but the PPF wont pay it out.

Iv pleaded with the Government and the PPF to advise this cant be right, but they are not interested and are leaving the blame with each other.

Im ready to take legal action against them but would be good to know of anyone else who has had any bad experiences dealing with them.

Thank you LIsa

0

Comments

-

3

-

yes i am aware of the rules, my father had a death benefit, im not trying to get compensation, wonder if it was your 43 years investment down the drain, you would think it was pretty standard? what is the point in paying into a pension?0

-

Firstly, I'm sorry for your loss.

This should have been clear in the pension rules from the onset. With a defined contribution pension there is a pot of money that belongs to the individual and can be inherited. A defined benefits scheme is more like an insurance policy, where everyone pays into one big pot and those that sadly pass early help to pay for those that live well beyond the average.

I can understand your frustration, but they really are two very different financial products.Think first of your goal, then make it happen!4 -

Yes I think the key thing is that your father didn't make a financial investment. He contributed to a pension scheme that would pay out benefits to all members in line with the scheme rules. The scheme rules have now been replaced by the ppf rules and these are being followed. They won't be making an exception for you. Pensions aren't there to provide an inheritance.4

-

Quite normal, that is how pensions are relatively cheap for the benefit they give, those that pass early pay the pensions of those that live to 100. Very few pensions have death benefits once in payment, they may have a survivor pension, and those that do usually only pay out to a spouse or children in fte. Upon entering the PPF some of the original rules may change, the other likely option would have been for the whole pension to be lost or severely reduced.

5 -

This is just how pensions work, no? For those who live long lives, they can pay out for 30-40 years; but if you die sooner, the payout ends.:heartpuls Mrs Marleyboy :heartpuls

MSE: many of the benefits of a helpful family, without disadvantages like having to compete for the tv remote") Proud Parents to an Aut-some son 3

Proud Parents to an Aut-some son 3 -

This is indeed how DB pensions work. If they were funded to cover pension payments to 100, with residual funds going to non-dependants in the event of an early death, these funds wouldn't exist because they would be too expensive.Tigsteroonie said:This is just how pensions work, no? For those who live long lives, they can pay out for 30-40 years; but if you die sooner, the payout ends.

Instead, the money crunchers work on the basis that those who sadly die in their 60s pay for those who live to their 90s+.3 -

I’m not sure why you think an exception should be made for you? This is how pensions work. Always a risk involved.3

-

Sorry for your loss, but don't shoot the messenger please.Lisa2108 said:yes i am aware of the rules, my father had a death benefit, im not trying to get compensation, wonder if it was your 43 years investment down the drain, you would think it was pretty standard? what is the point in paying into a pension?

In a defined benefit (DB) scheme, prople who die young offset the cost of people who live to be 80 plus. That is how DB pensions work, a pooling of (longevity and investment) risk.

Unlike a DC scheme, there is no individual pot, you get what the scheme rules say, no more and no less.

2 -

You won't find any lawyer to take on such a case, because it has zero chance of success. Once a scheme goes into the PPF, it becomes subject to the rules of the PPF and provided those have been correctly applied, that's the end of the matter. Others have explained above how a defined benefit scheme 'works' in terms of funding, which I hope has ensured that you now understand that aspect of things, however unpalatable.Lisa2108 said:

Im ready to take legal action against them but would be good to know of anyone else who has had any bad experiences dealing with them.

This is unlikely to make you feel much better, but until the PPF came into existence, an employer going bust could mean that the pension scheme also failed - and members could be left with nothing. As someone who over the years has had the task of relaying this desperately sad news to some of those affected by pre-PPF company insolvencies, I can only say that the current scenario definitely beats the old one hands down. Your father had the peace of mind during his retirement, however short, that his pension was safe and would be paid in accordance with PPF rules.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!11

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards