We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Mortgage broker - ask me anything

Comments

-

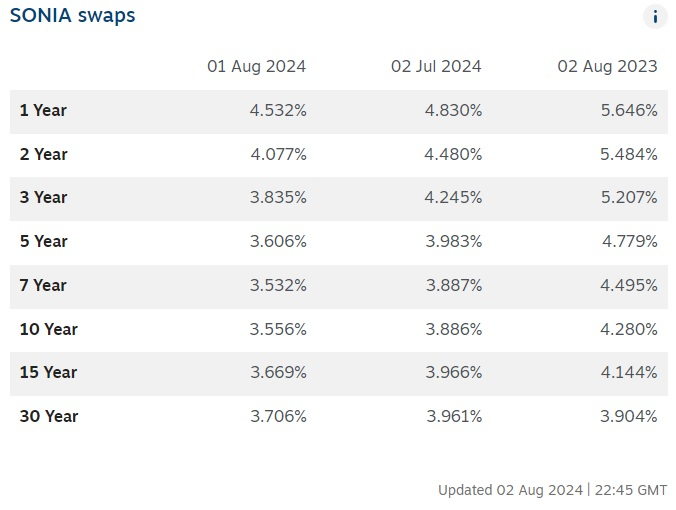

@DA1991 Given the movement downward in swap rates (https://www.chathamfinancial.com/technology/european-market-rates) since the rate-cut, and other lenders starting to cut, I would expect Nationwide (and all large lenders tbh) to follow at some point.Da1991_ said:Will nationwide lower their mortgage rates after the interest rate cut yesterday

You can keep an eye here for any upcoming rate cuts https://www.nationwide-intermediary.co.uk/news

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

I have an ltd which I own 100% (and don't take any income from) and my wife is it's only director receiving salary. My wife has an ltd which she owns 100% (and doesn't take any income from) and I'm it's only director receiving salary. Technically we are each other's employees. Will it be possible to bypass the self-employment rules and apply for a joint mortgage being employees without owning the business by only producing payslips and bank statements? We can afford mortgage payments, it's the document part that's a bit tricky. It's about playing the system. I'll appreciate if somebody can shed some light and why not help with this.The journey of a thousand miles begins with one step.0

-

@radoslaff I think you can guess the answer to the question you’ve posed.radoslaff said:I have an ltd which I own 100% (and don't take any income from) and my wife is it's only director receiving salary. My wife has an ltd which she owns 100% (and doesn't take any income from) and I'm it's only director receiving salary. Technically we are each other's employees. Will it be possible to bypass the self-employment rules and apply for a joint mortgage being employees without owning the business by only producing payslips and bank statements? We can afford mortgage payments, it's the document part that's a bit tricky. It's about playing the system. I'll appreciate if somebody can shed some light and why not help with this.It’s very unlikely that such an application would get past even the employer verification stage (usually includes a CH check for non household-name employers) without being flagged high risk and triggering further checks.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

It is only showing with Experian, not Equifax. I will try another Broker. I went through my usual broker and he found a small lender willing to lend the full amount, but when they went to progress this, this had showed on my credit file since the DIP. I then approached Santander as my current mortgage is with them (joint mortgage with ex partner) but they will only give a 80% LTV....... I have a 16% deposit and have no means of making it up to the 20%.K_S said:

@taradiamond1I'm assuming the decline was at soft-check DIP/AIP stage? If so don't stress too much, the decline by itself won't have any lasting impact.Taradiamond1 said:Hi, Post Office loans have made a mistake on my account with them and reported said mistake to the credit agencies, resulting in a failed mortgage application today. Post Office loans have sent me an email confirming the error (my credit score says I am in £4k of arrears, I settled in full in May and they actually owe me £300) and are treating it as an urgent complaint, its been 2 weeks already and likely to be another week to review my case, then up to 28 days for this to show in my credit reports. My seller is getting tetchy as he wants a quick sale. I am really stuck as its the only house in my price range that has come up in years! Help!!

If your mortgage application is with a large mainstream lender, then you probably will need to get the credit report fixed before applying again. If it's with a smaller lender, you may have the option to get them to manually adjust for the error based on the communication that you have from Post Office loans.

Is the loan showing on both Experian AND Equifax? If it's only showing on one of them, then you might have options.

All the best, I hope it works out!

Buth the small lender and Santander show on my credit file.

I will find another broker!

Many thanks0 -

@taradiamond1 Doesn’t sound insurmountable but do try and not add any more hard checks to your report. When you speak to a broker make sure you have your full latest Experian and Equifax reports to hand and do share what’s happened to now so they have the full picture.Taradiamond1 said:

It is only showing with Experian, not Equifax. I will try another Broker. I went through my usual broker and he found a small lender willing to lend the full amount, but when they went to progress this, this had showed on my credit file since the DIP. I then approached Santander as my current mortgage is with them (joint mortgage with ex partner) but they will only give a 80% LTV....... I have a 16% deposit and have no means of making it up to the 20%.K_S said:

@taradiamond1I'm assuming the decline was at soft-check DIP/AIP stage? If so don't stress too much, the decline by itself won't have any lasting impact.Taradiamond1 said:Hi, Post Office loans have made a mistake on my account with them and reported said mistake to the credit agencies, resulting in a failed mortgage application today. Post Office loans have sent me an email confirming the error (my credit score says I am in £4k of arrears, I settled in full in May and they actually owe me £300) and are treating it as an urgent complaint, its been 2 weeks already and likely to be another week to review my case, then up to 28 days for this to show in my credit reports. My seller is getting tetchy as he wants a quick sale. I am really stuck as its the only house in my price range that has come up in years! Help!!

If your mortgage application is with a large mainstream lender, then you probably will need to get the credit report fixed before applying again. If it's with a smaller lender, you may have the option to get them to manually adjust for the error based on the communication that you have from Post Office loans.

Is the loan showing on both Experian AND Equifax? If it's only showing on one of them, then you might have options.

All the best, I hope it works out!

Buth the small lender and Santander show on my credit file.

I will find another broker!

Many thanks

Good luck!I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

Hi,

I find myself in a very difficult position.

In brief, me and my partner had been due to exchange on a property in a national park last week. However, this has been paused as the property has a section 157 covenance on it which none of us were aware of.

We are currently appealing to the council for consent to move forward, however it now seems that our lender will not lend on these properties.

I’m looking on what we should do next - is there any way around this section 157, and how likely is it to get a mortgage on these properties? The vendors are in a difficult financial situation, which could ruin them if this does not go ahead.

thanks0 -

@welly2125 I’ve come across maybe a handful of these over the past decade so can’t claim to have a wealth of first hand experience! I’m pretty sure it’s always been placeable with a mainstream lender.Welly2125 said:Hi,

I find myself in a very difficult position.

In brief, me and my partner had been due to exchange on a property in a national park last week. However, this has been paused as the property has a section 157 covenance on it which none of us were aware of.

We are currently appealing to the council for consent to move forward, however it now seems that our lender will not lend on these properties.

I’m looking on what we should do next - is there any way around this section 157, and how likely is it to get a mortgage on these properties? The vendors are in a difficult financial situation, which could ruin them if this does not go ahead.

thanks

But assuming that this is some kind of local residency restriction (eg: buyer must have worked/lived in a certain area for X number of years prior to purchase), it will rule out some lenders but not all. It’ll also depend on exactly how onerous the restrictions are.Your best bet is to speak to a local broker (who in theory should be pretty familiar with this) who can give you an realistic idea of your options to get a mortgage to buy the property.

All the best!I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

Hi There 👋🏻

I’ve tried to locate an answer to this and found one comment on a thread so wanted to ask whether this was a ‘thing’.

Me and my partner are looking to move next year. I have been on a DMP managed via step change for the last 6 years and shortly the defaults will fall off my account.. albeit the DMP will still be active.

We’ve been lucky in that our current house value/equity has increased since we moved here a few years ago which will leave us with a significant amount of money for a large deposit (potentially 40%) as well as some additional funds left over.. which brings me to my next question.

Would any lenders offer a better rate if an agreement was made to clear the remaining DMP debt? As mentioned I did see one individual post advising they had received this providing the lender received confirmation within 30 days the debt had been cleared.

Im aware we could still get a mortgage with a DMP through a specialised broker - we’re looking at a mortgage of 2.5x salary, with as I mentioned at least a 30-40% deposit but would just like the weight finally lifted.Any advice would be appreciated.

Many Thanks0 -

Hi! I wondered if you could help me. We're looking to remortgage in November and want to pay off enough that we can hit the 75% ltv rate. How do we go about finding the value of our property as online valuations seem way off. We're with Barclays and have been told it will be a desktop valuation as it's only a rate switch. Thank you0

-

What a great post you have added.I just posted a new thread. So thought I would ask here and jump on.I wondered if you had any experience with TML and if they did a final credit check prior to completion.Nope I’ve not taken out any new credit or alike, I wouldn’t dare! Obtaining this mortgage is of the most importance to me. I’m just such a worrier and just won’t rest my nerves until I have those keys in my hand0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards