We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Mortgage broker - ask me anything

Comments

-

Do you know from your experience if HSBC ask for bank statements? Their website states only send in bank statements if and when requested.K_S said:

@lizzybeebum For the vast majority of applications, Halifax does not ask for bank statements, neither at the initial packaging stage nor at underwriting/assessment, so this is very unlikely to impact your application.Lizzybeebum said:Hello.

I have worked with a Broker to get an AIP with Halifax, despite 2 small defaults on my account from 2018.

My bank statements show 2 additional payments to Lowell and PRA group - debt collection agencies for very old credit card defaults that no longer show on my credit file. The monthly payments are small £5 and £18 - but the debt balance is quite high £4.7K and £3K.

Is this likely to impact my application or cause it get rejected?0 -

@jw2709 Off of the top of my head, I have had to upload bank statements for my recent HSBC apps. Couldn't say for sure whether it was all of them but it was definitely most of them.JW2709 said:

Do you know from your experience if HSBC ask for bank statements? Their website states only send in bank statements if and when requested.K_S said:

@lizzybeebum For the vast majority of applications, Halifax does not ask for bank statements, neither at the initial packaging stage nor at underwriting/assessment, so this is very unlikely to impact your application.Lizzybeebum said:Hello.

I have worked with a Broker to get an AIP with Halifax, despite 2 small defaults on my account from 2018.

My bank statements show 2 additional payments to Lowell and PRA group - debt collection agencies for very old credit card defaults that no longer show on my credit file. The monthly payments are small £5 and £18 - but the debt balance is quite high £4.7K and £3K.

Is this likely to impact my application or cause it get rejected?I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

My broker has referred to my application as a triage case due to my past CCJ and wife's late payment...do brokers normally use this term, if so what does it actually mean?0

-

@jw2709 I haven't come across that specific phrase in this context.JW2709 said:My broker has referred to my application as a triage case due to my past CCJ and wife's late payment...do brokers normally use this term, if so what does it actually mean?

With respect to mainstream lenders it probably just means something that needs to be run past the lender/BDM, or that is subject to lender/underwriter discretion, etc.

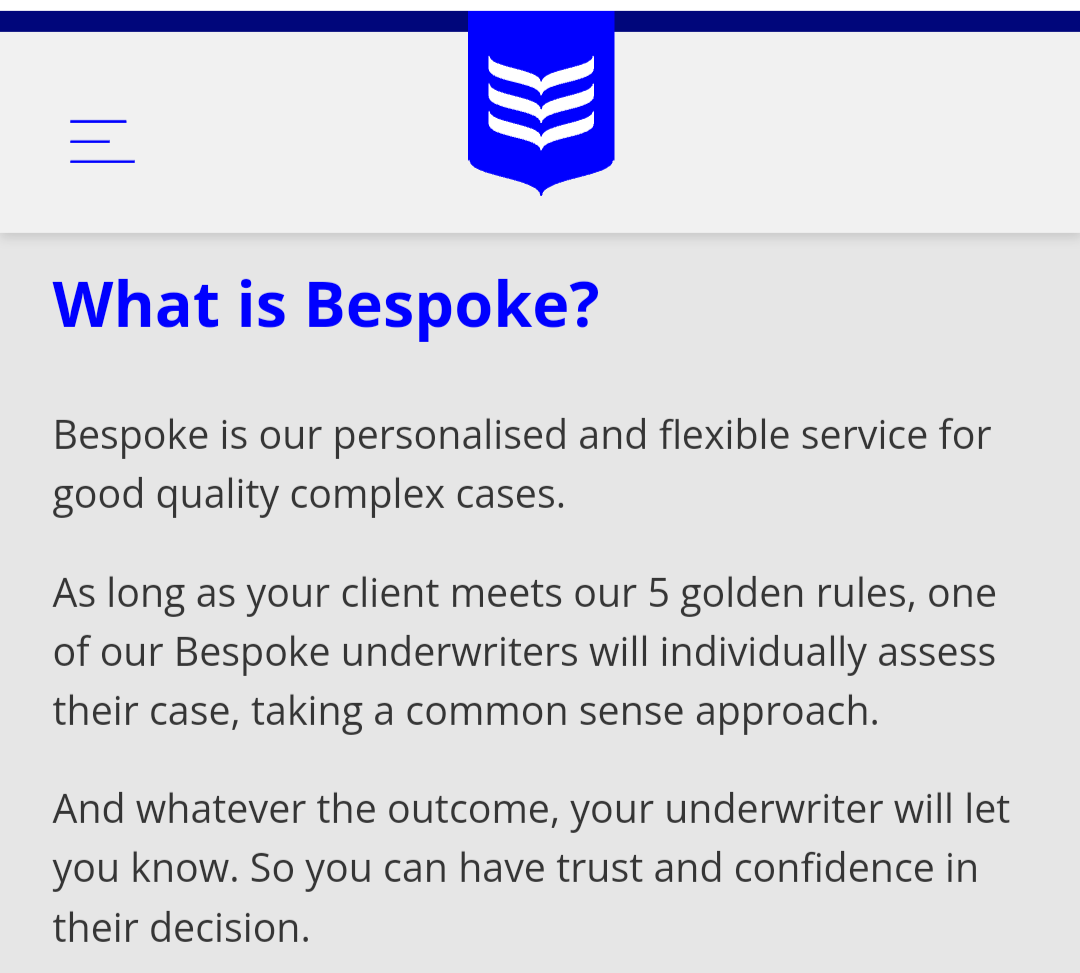

In the case of specialist/smaller lenders or bespoke products it could mean something like the below, or its equivalent

Or something like BOI's bespoke service

All the above is just an educated guess based on the context!I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

Hi all, I'm applying for a mortgage for a refurbished property (detached house) that's gone through substantial changes recently. I noticed that quite a few banks have a different LTV for refurbished properties as they consider them new builds and so offer lower LTVs. I'm a first time buyer and looking for a 90% LTV. Any advice as to which high street banks provide a 90% LTV for properties if they consider it a new build (as in recently refurbished/extended).

0 -

I will apologise in an advance as I feel like I've posted on here a few times, each time with bits of info.

This is my full current position and any advice would be greatly appreciated because I am worrying myself sick!

My position:

Income £54500K

Annual Bonus £10K (for the last 2 years)

Credit Card debt of £3600

Catalogue buy now pay later of £1600

Loan total £5600, balance of £2300 4 payments remain. Expecting to clear in Dec with bonus.

1 CCJ from 2019 for £450 satisfied in April this year (honestly reason for not settling earlier as I didn't realise the impact of non satisfied vs satisfied would have)

Wife

Income £27500

Credit card debt £5600

1 late payment on a catalogue in Jan 2021 (visible on all CRA)

2 late payments in 2019 (only visible on Transunion)

Property value £340K

Deposit £51K (15%)

Reached out to a broker. Shared full credit reports from CheckMyFile.

-Advised that we could possibly match with HSBC (to my surprise).

-Broker had a call with a BDM who advised to submit for an AIP.

-Broker advised AIP was referred and was ask to provide supporting info regarding reason for adverse credit along with full credit files

-Broker than advised HSBC happy with the reasons provided and AIP agreed but case will “triaged” and HSBC cannot provide a certificate for the AIP. (Noticed a soft check on credit file on the day I was advised this)

-Found a property, offer made and accepted.

-Through conversations with the broker, when asked about next steps and how long for a decision as I am still nervous about the credit check, he has said the AIP was a system decline and that my case is unusual due to adverse credit and that the full application will be submitted by HSBC (which I don’t fully understand).

-When questioned why are we using HSBC if they have declined at AIP he has said HSBC (or his contact there) have asked to submit and they will look in more detail when it goes through the underwriters and could be approved, but case needs to be looked at in more detail.

-Broker said the soft check they did is broadly the same as the hard check they will do but the hard check will leave a footprint. He has advised that he hopes to hear back by the end of the week.

-Advised affordability should be an issue.

I really don’t know where to go from here…I don’t want to be applying with a lender who is likely to reject us and leave a mark on our credit file and then feel massively deflated. I appreciate our broker is trying to get us the best rate through a high street lender, but I am nervous as hell and feel like we are probably wasting our time.

My broker fee is £499 and have paid £100 deposit and expect to pay the £399 balance when application goes in. I have questioned my broker in that if HSBC decline what do we do next and his was response was, there are other lenders we can look at and you will likely have to pay a higher rate and we’ll cross that bridge when we come to it.

Ultimately, I wouldn't have made an offer unless I felt like getting a mortgage was going to be possible and would have waited perhaps another 3-6 months and saved more of a deposit.

Any advice would be greatly appreciated.

0 -

Just posted this in a separate thread before seeing this one, apologies:

Had a mortgage offer at the end of August valid for 6 months at 5.43% but with rates dropping I would expect to be able to find something lower before completion. Any experience in this scenario? Would the bank (Halifax) change the rate upon request/threat to reapply elsewhere?

0 -

JW2709 said:Ultimately, I wouldn't have made an offer unless I felt like getting a mortgage was going to be possible and would have waited perhaps another 3-6 months and saved more of a deposit.

Any advice would be greatly appreciated.

@jw2709 I don't really have much to add that would be useful.Generally speaking, I just want to emphasise two points -- based on the info you have shared, the primary relevant issue is a <£500 4+ year old CCJ on your report. At 85% LTV, there is absolutely no reason to believe that you won't get one of the following: a mainstream mortgage (just one lender is all you need), a mainstream-ish product from a mainstream lender (eg: Accord cascade) or a mainstream/mainstream-ish rate from a smaller building society that doesn't credit score. I would expect option 1 to come through.- a decline and the hard-check that it leaves is very very unlikely to be the end of the road as far as your mortgage chances are concerned. I often get clients that come to me after having being declined and that (on its own) has never stopped them from getting a mortgage that they're happy with.Ultimately, if you trust the broker, go ahead with the app and see how it goes. Alternatively, reconfirm with the broker that they have tried alternate mainstream/high-street lender DIPs, or else run them yourself and then take it from there.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

First_Time_Buyer000 said:

Hi all, I'm applying for a mortgage for a refurbished property (detached house) that's gone through substantial changes recently. I noticed that quite a few banks have a different LTV for refurbished properties as they consider them new builds and so offer lower LTVs. I'm a first time buyer and looking for a 90% LTV. Any advice as to which high street banks provide a 90% LTV for properties if they consider it a new build (as in recently refurbished/extended).

@first_time_buyer000 Are you sure that the property would be seen as a 'new-build' by lenders? The reason I ask is the refurbished/converted as 'new build' category generally applies to things like one house being split into 4 flats, the local pub being converted into flats, a house being demolished and two new houses built on that land, etc.In my experience, the vast majority of houses that have been bought by a developer and refurbed will not be seen as a new property with LTV restrictions so you might well be worrying about a problem unnecessarily.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

@sfw Like the vast majority of other mainstream lenders, Halifax will happily switch you to a current rate. Contrary to what a lot of people think, switching to a lower rate does not affect lenders very much at all, so go for it if you want to!SFW said:Just posted this in a separate thread before seeing this one, apologies:

Had a mortgage offer at the end of August valid for 6 months at 5.43% but with rates dropping I would expect to be able to find something lower before completion. Any experience in this scenario? Would the bank (Halifax) change the rate upon request/threat to reapply elsewhere?

It involves their system 're-scoring' the app and then issuing the revised mortgage offer with the new product.

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards