We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Mortgage broker - ask me anything

Comments

-

@turtletowers A DIP/AIP is based on two things - what you input on the form and your credit history. So in theory, you *could* potentially get an AIP based on entering future income but its usefulness is very limited as it doesn't guarantee the rate, doesn't guarantee how much you can borrow, the numbers might be off and it will probably expire before you sort out the UC and maintenance. Plus you will only be able to submit a full application once you have all the evidence required by the lender for UC and child maintenance income.turtletowers said:I’ve separated from my husband. He has moved to a rental property for 3 months while we sort out long term logistics.

He wants to buy me out of the family home, but in order to obtain a mortgage I will be relying on work income, Universal Credit and child maintenance payments from him.

Until we have finalised the sale of the house to him, he has agreed to keep paying the share of the family bills as normal (he wants us to take the rental costs out of overall equity eventually)

Therefore I have not yet made a claim of any benefits nor is he specifically transferring maintenance payments to me.

My question is - How flexible are lenders about offering an agreement in principle when a Universal Credit claim is not yet processed or maintenance payments have been agreed but not yet commenced?It feels like in order to get a head start on the process I would need to sever financial ties with him sooner and claim benefits but that feels wrong when we don’t need the benefit yet as we have the agreement that he will continue to contribute to the mortgage and bills until ownership and equity are transferred.I want to be viewing properties but feel I will be misleading vendors if I need to wait 3 months post equity release to be approved for a mortgage.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

@fkhan95Fkhan95 said:Hi,

I wanted to know if accord mortgages accept DLA (in name of child) as a source of income.

Also, are there any additional barriers to their boost LTI (upto 5.5 I believe?) apart from the >60k income requirement?

Thanks

DLA - for affordability, not afaik

Boost LTI - depends on LTV, background debt and Accord 'credit-scoring'. You may get a very rough indication by plugging in the numbers on the Accord affordability calc. Your broker will most likely need to run a DIP to be sure of whether that is an option.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

Hi,

I'm in the process of re-mortgaging and despite the rate increases it's going to be useful as it'll allow us to roll in some credit card debt at a much lower interest rate. We have a formal offer from the new lender and solicitors are proceeding with the documentation.

We're in a pinch this month (which should sort itself in a month or two when the mortgage goes through) and two credit card lenders have offered to pause interest payments for 3 months but it will show as a mark on my credit score.

My question is does this affect the mortgage offer? I'm guessing not as a formal offer has been issued and we are proceeding but I want to be certain before I do this.0 -

@ByzantineByron

Will it affect the mortgage offer - impossible to say for sure

Can it affect the mortgage offer prior to completion - absolutely. If the lender system does an updated soft-check/re-score prior to releasing funds, and the report that the lender checks (Experian or Equifax) now shows you missing credit payments for the most recent month, this could be construed as a material change in your circumstances leading to your offer being withdrawn. You would have no comeback against that.

If you want to be certain, hold on until after completion.ByzantineByron said:Hi,

I'm in the process of re-mortgaging and despite the rate increases it's going to be useful as it'll allow us to roll in some credit card debt at a much lower interest rate. We have a formal offer from the new lender and solicitors are proceeding with the documentation.

We're in a pinch this month (which should sort itself in a month or two when the mortgage goes through) and two credit card lenders have offered to pause interest payments for 3 months but it will show as a mark on my credit score.

My question is does this affect the mortgage offer? I'm guessing not as a formal offer has been issued and we are proceeding but I want to be certain before I do this.

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

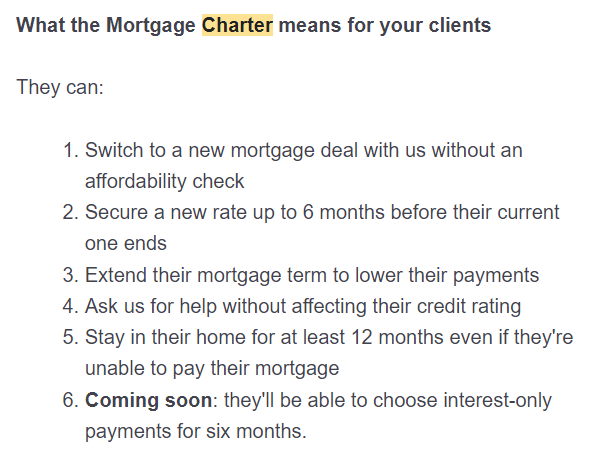

Virgin money called them still saying 120 days and not honoring the 6 months switch.K_S said:@silvercar

1 - nothing new with mainstream lenders, though yet to be seen if PT eligibility criteria (eg: no recent/current arrears on the mortgage) will be loosened

2 - There are lenders with 3-4 months product switch window, so if that extends to 6 months, that's an improvement for those borrowers

3 - the devil lies in the detail. If this involves an affordability check then it's similar to what it is now, though some lenders already extend to stated retirement age or 70 without full underwriting. If it a more blanket policy (eg: extend to lower of stated retirement age and 70 without full underwriting ) then it's an improvement

4 - as it is now

5 - not likely to mean anything in practice

6 - definitely a big change and from what I've heard it looks like it will be something like a PT, you go on the website, click the option and it's done.silvercar said:

Surely 1, 2 and 4 are nothing new. 5 would have happened by default anyway given that customers would always had a few months before the lender resorted to repossession and the legal processes would have taken another few months. So the new item is 3, with 6 coming soon.K_S said:

@homesaver234 Nationwide's update on the Mortgage Charter, it was sent out today to brokers and full details are on their consumer website herehomesaver234 said:Have you found any way to get Nationwide or Barclays to honour their comittment to provide the new Mortgage Charter switch to interest-only?

Both have refused me. Nationwide even denied it has agreed to the charter, saying the Govt. info that it has agreed is wrong!

When does the new mortgage charter start? On the gov website states from the 10th July

Called virgin money with the intention of mortgaging on the 5th August, current deal ends 01/02/2024 and they are still saying reportage is 120 days before 4th October but advisor said can have 6 months interest only or increase the term. I would like to select a fix rate ASAP, later when my 1.64% ends then will opt for interest only but my propriety now is to fix as soon as I can before BOE increase rates further.

0 -

Hola,

1) Is there a 'better-than-rest' comparison site to use / what's the deal with comparison sites?

To explain:

I hop on to a comparison site and unless it's Uswitch (which asks 1000 questions to give me no info at the end!) it gives me a set of results with my details.

I hop on Nationwide (current lender), put in the same details & it gives me a slightly different set of results for the same terms. Not massively but different all the same.

I log in to my Mortgage Manager on Nationwide, same details & it gives me a slightly different set of results again. Again - slightly, not massively.

So....

When I'm wanting to compare, to see if it'd be better for me to jump ship to a different lender or not, it's a little difficult because it's not really a fair comparison?

2) Are there any legal implications of a family member loaning you an amount (say £10k) to overpay a mortgage?

I'm not talking about setting up a pay back agreement. I'm talking about is it perfectly fine, no problems at all as far as banks are concerned, for someone to just go here you are, I have this £10k spare, I want to help you & pay me back over time as you can?

3) Depending on #2, I'm looking at a few options:

* lock in again on a fixed term with no cash injection

* lock in again with a £10k injection reducing the term from approx 20 to 17yrs & taking 78k to 68k.

* lock in again with said £10k injection but leave term as is, which puts monthly payments £45 dearer than if I drop the term to 17yrs.

* as the first lock in - with no cash injection, but look to see about increasing SIPP (let's not get in to workplace pension for this - employee & employer pay in the minimum as that's all the employer will pay in) contributions.

* obviously other options too - money in to savings.

Is it possible really to say over the time what would be more financially beneficial long term (so end of mortgage)? I should pay the mortgage off by about age 64 I think it is & an aimed retirement age of 65 & being 40 now.

4) What's this rate that is spoken of? I hear rates could hit 6% or whatever but when I hop on Nationwide to get a rate quote, it's saying APRC of 7.0% on a 5yr fixed, 5.9% on a 10yr - bit of a difference. Though the 'initial' rate is 5.59% on a 5yr, 4.99% on a 10yr. What are they referring to when they throw these numbers about?

5) I'm likely to see the MA who I dealt with last time to run some questions by him for specific advice since I appreciate it can't be given here.

I assume there's nothing wrong with me securing in a (10yr say) fixed deal now before seeing him which I assume could be changed after seeing him if a better deal had appeared on the market?

6) with securing in a deal - if I secure it today assuming NO overpayment but later on decide to go ahead and overpay (before the deal kicks in), is that possible?

Or is it that since I'll have made an alteration to 'the agreement' then the agreement/deal is scrapped and I'll have secured nothing?🤐🤐🤐

0 -

Virgin money called them still saying 120 days and not honoring the 6 months switch.

Oww...When does the new mortgage charter start?

Good question.

Govt. says: "The lenders ... will move quickly over the coming days and weeks to implement the Charter and will provide Government with an update on progress by Friday 30 June."

https://www.gov.uk/government/publications/mortgage-charter/mortgage-charter

but I have seen no such update reported. Have anyone else?

Some lenders have reported direct to borrowers e.g. NatWest "We're looking at how we could help and will update on 17th July. "0 -

Hi, our 23 year old DD is beginning to think about getting on the housing ladder but she is on a 12 month temp contract covering maternity leave. Her employer has said that there is every likelihood of a permanent position being available for her at the end of the 12 months. She is earning c£23k with no debts or finance and very healthy savings which would fund a 20%+ deposit. Would a lender consider her for a mortgage if we were put on as guarantors? We have a 29k mortgage (<10% LTV) and are in our late 40s earning c£70k combined.Mortgage Aug 22 £280,000

Current mortgage £28,0000 -

@kandfs_mamkandfs_mam said:Hi, our 23 year old DD is beginning to think about getting on the housing ladder but she is on a 12 month temp contract covering maternity leave. Her employer has said that there is every likelihood of a permanent position being available for her at the end of the 12 months. She is earning c£23k with no debts or finance and very healthy savings which would fund a 20%+ deposit. Would a lender consider her for a mortgage if we were put on as guarantors? We have a 29k mortgage (<10% LTV) and are in our late 40s earning c£70k combined.

Setting aside the issue of whether or not the numbers add up -

Sole mortgage based on daughter's income: if this is her very first fixed term contract, then her options are likely to be very limited, if any

Joint Borrower Sole Proprietar (3 of you on the mortgage, only your daughter on the deeds): A decent number of mainstream lenders will consider under their JBSP criteria as long as parents meet criteria and affordability (based on lender's calculations) for the loan amount required.

Skipton is one of those lenders and their affordability criteria may give you a very rough idea of whether or not the numbers add up under JBSP.

https://www.skipton-intermediaries.co.uk/tools-and-support/Calculators/affordability-calculator

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

Ty KS, affordability calculator is showing more than 4x what we would need to borrow. For clarity DD has worked full time on permanent contracts in hospitality for 2 years but this current fixed contract job is a change of career for her.Mortgage Aug 22 £280,000

Current mortgage £28,0000

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.3K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards