We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Mortgage broker - ask me anything

Comments

-

Hi,

I've got a recommendation from a broker for the following mortgage borrowing £127,999.00 The £999 is the fees added onto the mortgage. HSBC Fixed 3.19% 64 months £542.23 Fee £999.00

I was advised this was the cheapest deal for me. I had a look at alternative deals as well and I found this one again with HSBC Fixed 3.44% 64 months £555.63 Fee £0, this one is also listed as one that was considered by the broker but as it wasn't the cheapest I wasn't recommended this one.

I'm sure I must be missing something but wouldn't the second one be cheaper? The extra I'm paying over 64 months looks to be £857.60? Unless I've badly messed up my maths the deal with no fee works out slightly cheaper.

I'm not very clued up with finance or any good at maths so go easy on me! Would appreciate if someone could explain why the first deal is cheaper?

Thanks0 -

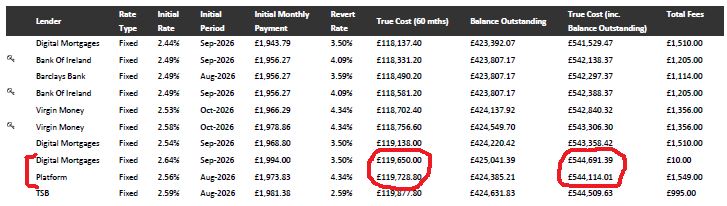

@Deleted_User The difference is probably because you are going by the 'total-cost' while the broker is going by the 'total-cost including balance outstanding at the end of 5 years', which is a truer measure. The below snapshot is from an EoR (evidence of research) that I send clients showing why I've recommended a specific product and how it stacks up with the competition.Deleted_User said:Hi,

I've got a recommendation from a broker for the following mortgage borrowing £127,999.00 The £999 is the fees added onto the mortgage. HSBC Fixed 3.19% 64 months £542.23 Fee £999.00

I was advised this was the cheapest deal for me. I had a look at alternative deals as well and I found this one again with HSBC Fixed 3.44% 64 months £555.63 Fee £0, this one is also listed as one that was considered by the broker but as it wasn't the cheapest I wasn't recommended this one.

I'm sure I must be missing something but wouldn't the second one be cheaper? The extra I'm paying over 64 months looks to be £857.60? Unless I've badly messed up my maths the deal with no fee works out slightly cheaper.

I'm not very clued up with finance or any good at maths so go easy on me! Would appreciate if someone could explain why the first deal is cheaper?

Thanks

If you look at the two deals that I've marked on there, you may get an idea of what I'm talking about.

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

Could you tell me if its normal that no soft/hard searches are showing on our file after submitting a mortgage application?

There is a soft search showing from the mortgage broker on 14/7 however our application was submitted 15/7 and nothing showing from the lender (hsbc).

Automated valuation was also done on 15/7 & hsbc requested upto date payslips from my husband 22/7.

0 -

@esiuol_1 I wouldn't worry too much about it. Searches showing up on the report can often be delayed, show the wrong dates, show up twice, etc. If a full application has been submitted with HSBC, you can rest assured that a hard-check on your Experian report has taken place or the HSBC DIP soft-check has been updated to a hard-check.Esiuol_1 said:Could you tell me if its normal that no soft/hard searches are showing on our file after submitting a mortgage application?

There is a soft search showing from the mortgage broker on 14/7 however our application was submitted 15/7 and nothing showing from the lender (hsbc).

Automated valuation was also done on 15/7 & hsbc requested upto date payslips from my husband 22/7.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

Hi

Do you have an opinion on how proportunity compares to Help 2 buy? Do you or many other brokers work with the likes of Proportunity?

Thanks0 -

Few questions:

- I am looking to purchase a house which I don't think will be on market long. I have been put in touch with a mortgage broker from the company selling the house.

- The broker was first advising me against a mortgage and then has been a bit difficult with trying to arrange to meet them.

- I'm now worried I'm going to miss out on this property. How long does a mortgage in principle take to get?

With regards to my situation:

- 3 bedroom house with garage for 90k (Northern Ireland)

- Have a deposit of up to 20k

- Joint income roughly around 43k (34k + 9k)

- Higher income person has 300 pound unsettled ccj from a parking ticket due to drop off in December

Firstly the broker said it wouldn't be possible to get a mortgage unless I settle the ccj and that will take 30-60 days.

Then they said it would only be possible with a 20k deposit but would result in 100 pounds per month extra interest fees compared to average mortgage. And she doesn't recommend it.

As we were in discussion over email she said it would be better to see her in person and that she can meet in person in the evening. So I then suggested doing this and she said she's busy every evening until the day after the viewing.

I was always planning to buy after December when the Ccj drops but this house looks perfect for me right now and I really want to be in with a chance. But to me it just feels like the broker is trying to put me off it and also put of seeing me,

Call me cynical but I'm even beginning to think that she has personal interests herself or something influencing this advice. She knows that I know the family who inherited and are selling the house too and that they'd look favourable on me.

Is this normal behaviour/advice? Would you advise someone against potentially paying an extra 100 per month on mortgage in interest and advise them to continue renting which has even more dead money?

So to ask:

- How quick can I get a mortgage in principle

- Do you think I can get a mortgage given the above info? (You know as much as my broker)

- If yes to the above then how can I find an alternative broker

0 -

@kizzy1926 From a cost point of view, H2B is miles cheaper than Proportunity or any other similar products. Primarily because H2B is government backed, which means the risk for lenders is minimal, and the equity loan being interest-free for 5 years and capped hikes from that point. For example, the Prop equity loan interest rate is typical 6-8% fixed for the first 5 years and then variable after that.kizzy1926 said:Hi

Do you have an opinion on how proportunity compares to Help 2 buy? Do you or many other brokers work with the likes of Proportunity?

Thanks

Comparing Proportunity to H2B, the main differences are that Prop doesn't have as many restrictions - you can use it for non new-builds, don't need to be an FTB, etc.

Plenty of brokers work with Proportunity but you can use them direct as well.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

@thehatchetman Quick thoughts on your questions -TheHatchetMan said:Few questions:

- I am looking to purchase a house which I don't think will be on market long. I have been put in touch with a mortgage broker from the company selling the house.

- The broker was first advising me against a mortgage and then has been a bit difficult with trying to arrange to meet them.

- I'm now worried I'm going to miss out on this property. How long does a mortgage in principle take to get?

With regards to my situation:

- 3 bedroom house with garage for 90k (Northern Ireland)

- Have a deposit of up to 20k

- Joint income roughly around 43k (34k + 9k)

- Higher income person has 300 pound unsettled ccj from a parking ticket due to drop off in December

Firstly the broker said it wouldn't be possible to get a mortgage unless I settle the ccj and that will take 30-60 days.

Then they said it would only be possible with a 20k deposit but would result in 100 pounds per month extra interest fees compared to average mortgage. And she doesn't recommend it.

As we were in discussion over email she said it would be better to see her in person and that she can meet in person in the evening. So I then suggested doing this and she said she's busy every evening until the day after the viewing.

I was always planning to buy after December when the Ccj drops but this house looks perfect for me right now and I really want to be in with a chance. But to me it just feels like the broker is trying to put me off it and also put of seeing me,

Call me cynical but I'm even beginning to think that she has personal interests herself or something influencing this advice. She knows that I know the family who inherited and are selling the house too and that they'd look favourable on me.

Is this normal behaviour/advice? Would you advise someone against potentially paying an extra 100 per month on mortgage in interest and advise them to continue renting which has even more dead money?

So to ask:

- How quick can I get a mortgage in principle

- Do you think I can get a mortgage given the above info? (You know as much as my broker)

- If yes to the above then how can I find an alternative broker

1. I can't comment on your broker's processes, but once I get all the info and documents required from the client, I do the DIP within 1 day. The result is usually instantaneous. On the odd occasion, it may be "referred" for a manual review which can take 1-2 working days depending on the lender.

2. Looking to borrow 70k at 80% LTV, 43k income, only blemish one 5+ year old unsat CCJ for £300. Sounds more than doable in England, Wales and Scotland. I don't do NI mortgages so can't factor that in.

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

K_S said:

@thehatchetman Quick thoughts on your questions -TheHatchetMan said:Few questions:

- I am looking to purchase a house which I don't think will be on market long. I have been put in touch with a mortgage broker from the company selling the house.

- The broker was first advising me against a mortgage and then has been a bit difficult with trying to arrange to meet them.

- I'm now worried I'm going to miss out on this property. How long does a mortgage in principle take to get?

With regards to my situation:

- 3 bedroom house with garage for 90k (Northern Ireland)

- Have a deposit of up to 20k

- Joint income roughly around 43k (34k + 9k)

- Higher income person has 300 pound unsettled ccj from a parking ticket due to drop off in December

Firstly the broker said it wouldn't be possible to get a mortgage unless I settle the ccj and that will take 30-60 days.

Then they said it would only be possible with a 20k deposit but would result in 100 pounds per month extra interest fees compared to average mortgage. And she doesn't recommend it.

As we were in discussion over email she said it would be better to see her in person and that she can meet in person in the evening. So I then suggested doing this and she said she's busy every evening until the day after the viewing.

I was always planning to buy after December when the Ccj drops but this house looks perfect for me right now and I really want to be in with a chance. But to me it just feels like the broker is trying to put me off it and also put of seeing me,

Call me cynical but I'm even beginning to think that she has personal interests herself or something influencing this advice. She knows that I know the family who inherited and are selling the house too and that they'd look favourable on me.

Is this normal behaviour/advice? Would you advise someone against potentially paying an extra 100 per month on mortgage in interest and advise them to continue renting which has even more dead money?

So to ask:

- How quick can I get a mortgage in principle

- Do you think I can get a mortgage given the above info? (You know as much as my broker)

- If yes to the above then how can I find an alternative broker

1. I can't comment on your broker's processes, but once I get all the info and documents required from the client, I do the DIP within 1 day. The result is usually instantaneous. On the odd occasion, it may be "referred" for a manual review which can take 1-2 working days depending on the lender.

2. Looking to borrow 70k at 80% LTV, 43k income, only blemish one 5+ year old unsat CCJ for £300. Sounds more than doable in England, Wales and Scotland. I don't do NI mortgages so can't factor that in.

Thank you so much for replying. It's reassuring to hear that I could get a mortgage in principle quite quickly.

Yeah I thought given everything else on my record and the amount were looking to borrow that a mortgage should be possible so was surprised by the brokers advice.

Might try using another broker which a family member has used in the past instead. Thanks for all your help.0 -

My husband and I are planning on starting a family in the next year or two, but what worries me, is that our fixed rate mortgage is due to end Feb 2025, and I would likely be on maternity (statutory) leave when we look to remortgage!

So my bank statements/ pay slips would be vastly different on maternity leave, in comparison to what they typically would be working full time.

Would this effect our remortgage? or would my pre-maternity pay slips/ bank statements be taken into account?0

![[Deleted User]](https://us-noi.v-cdn.net/6031891/uploads/defaultavatar/nFA7H6UNOO0N5.jpg)

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.8K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards