We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Mortgage broker - ask me anything

Comments

-

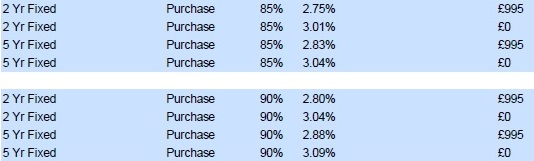

@fsl13 Currently, it's only around a 0.05% difference in interest rates between 85% LTV and 90% LTV products.FSL13 said:@K_S

What you said makes total sense to me. So basically I save 1.5k but would still need to find the other 4k (initial cost of work would be 5.5k but other things would need doing medium term for 2k) initially to do the work.

How much extra would a mortgage cost based on 90% LTV than 85% LTV for a 123k house? Would a better bet to try get a loan or pay for the work on a credit card (I have really good credit and have 10k of unused CC credit)

But depending on whether NatWest allow you to pick a 90% LTV product that was available back when you applied (probably a lower rate than today), or force you to pick one that is currently available (see below) that difference in rates might be higher.

Just to be clear, these are the intermediary rates, I don't know if the direct rates are lower/higher at present as it can sometimes vary with NatWest.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

Hi I'm toying with the idea of renting both a new place ( to try out an area ) but also to stay on the ladder renting my existing property out. My current property is valued about £420k with mortgage of £250k left. I currently pay about £1500 PCM, and could rent out for about the same ( possibly a bit more ). My fixed rate deal elapses at the end of the year ( currently there is a £5k ERC ).

Does it make sense to approach my current lender now about renter, or way and then have the whole market to choose from?0 -

@de_612183 Well, if you're moving into rented you won't have the whole market to choose from as you won't be an 'owner-occupier' which is a very common criteria for BTL lenders. You may still have potential mainstream lenders though, so it shouldn't necessarily mean a higher rate.DE_612183 said:Hi I'm toying with the idea of renting both a new place ( to try out an area ) but also to stay on the ladder renting my existing property out. My current property is valued about £420k with mortgage of £250k left. I currently pay about £1500 PCM, and could rent out for about the same ( possibly a bit more ). My fixed rate deal elapses at the end of the year ( currently there is a £5k ERC ).

Does it make sense to approach my current lender now about renter, or way and then have the whole market to choose from?

From the point of view of maximising your BTL lender pool, the boxes you want to tick are -

- have moved out of the house and in to the rented place

- changed all your accounts to the rental address

- credit report to reflect the above changes

- have tenants in the property

Just to clear the above aren't all necessary conditions, but will maximise your options.

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

Can I change jobs between applying for a mortgage and completion?

0 -

@zerofax You can, but what impact (if any) it has on the mortgage offer will depend on the specifics and the policies of the lender that you are with. For example Barclays will need to see one payslip from the new job while Halifax will be happy with the future contract.Zerforax said:Can I change jobs between applying for a mortgage and completion?

There may be other issues as well, for example if your affordability depended on a variable component of income from your current job - annual bonus, quarterly commission, etc.

I would recommend speaking to your broker or (if direct) the lender to under the ramifications specific to your case.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

Hi, wondering if anyone can advise.

Had a mortgage offer in Feb, due to complete in August....I have used my credit card to make purchases for the house which has now increased by overall debt by around £3k.

Am I better off using some of my deposit money to clear the credit card? I am worried that my lender will do another credit search and withdraw my mortgage offer?

So I'm wondering whether I should clear down the credit card debt so if they do run another search it will be the same as when they approved me, and then use my credit card in August to pay the shortfall of deposit to complete?

Hope that makes sense, in a way I am just moving funds from my bank account onto the credit card balance. Has anyone else experienced this or have any advice? I'm having sleepless nights now thinking at any moment a new hard search will be done!

Thank you0 -

K_S said:

@zerofax You can, but what impact (if any) it has on the mortgage offer will depend on the specifics and the policies of the lender that you are with. For example Barclays will need to see one payslip from the new job while Halifax will be happy with the future contract.Zerforax said:Can I change jobs between applying for a mortgage and completion?

There may be other issues as well, for example if your affordability depended on a variable component of income from your current job - annual bonus, quarterly commission, etc.

I would recommend speaking to your broker or (if direct) the lender to under the ramifications specific to your case.

Thanks - really helpful. Sounds like Halifax would be best for us. Actually would be taking a small mortgage and so if I did take a new job, I'd probably only be borrowing 1x salary multiple (without worrying about variable components).

0 -

I have an AIP from NatWest, via a broker. Yesterday I had an offer on a property accepted and the estate agent advised that their broker recommends I steer away from NatWest as they are taking 18 weeks to process applications. Are they weight and should I go elsewhere? We have been matched with NatWest due to our circumstances ( husband self employed and a couple of late payments all over or almost 3 yrs ago ?0

-

@Mrs6653 This is NatWest's average service levels at the momentMrs6653 said:I have an AIP from NatWest, via a broker. Yesterday I had an offer on a property accepted and the estate agent advised that their broker recommends I steer away from NatWest as they are taking 18 weeks to process applications. Are they weight and should I go elsewhere? We have been matched with NatWest due to our circumstances ( husband self employed and a couple of late payments all over or almost 3 yrs ago ?

https://www.intermediary.natwest.com/intermediary-solutions/service-levels.html?intcam=HP-B-TB-DEF-Default

Initial assessment - 7 working days

Underwriting - 8 working days

Assessing any further information (won't be required for every application, only where there are queries) - 5 working days

As you can see above, if everything goes smoothly, you can get through in a couple of weeks. 13% of applications go to offer within 7 working days and 37% within 14 working days.

If there are queries, every to and fro can add 5 working days (1 week) to the process. So to get to 18 weeks you would have to be extraordinarily unlucky with the number of queries that arise and a lot of to and fro.

NatWest is a mainstream lender and while they are one of the slower high-street lenders at the moment, there is simply not enough reason to avoid them if they are the right lender for you, both criteria and rate wise.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

Hi

im 55, single and finally debt free with a clear credit score for past 6 years. im wanting to buy a small house, around here can get small house for around 100k, now kids all left home (currently renting), I have a 6k deposit at the moment, what are my chances of getting a mortgage? im an nhs nurse in a substantive post earning 39k/yr, with intention of moving up to a higher band in next year or so. Do i stand a chance with a small deposit and 12 years left to work til i retire? or do i need a much bigger deposit?

i pay into nhs pension scheme & have life insurance.

thanks for any advice") wading through the treacle of life!

wading through the treacle of life!

debt 2016 = £21,000. debt 2021 = £0!!!!0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.8K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.4K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards