We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Mortgage broker - ask me anything

Comments

-

@iamiam Potentially, though the max borrowing with £850 rent might be a bit less than 170k.IAMIAM said:Moving into rented and travelling for work for 3-5 years.

Moving mortgage to BTL (170k LTV with 230k VAL).

Ideally interest only.

Rental Income would be £850 PCM

Salary would be circa 50k min.

Is this doable?

Your options will depend on the timing - whether you want to apply before moving out (very few options if any) or after.

The smoothest route would be to move out+get a CTL, get a tenant in and then remortgage to BTL.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

Thanks. Second question too. Are offset mortgages worthwhile when interest rates are rapidly increasing? What are current rates like on 170k 75% LTV with 50k in offset account (ie 120k being charged interest)0

-

@mrbounce In most cases it doesn't.MrBounce said:

Does that mean new application?K_S said:

@mrbounce Congratulations!MrBounce said:We have had our Halifax Resi approved (Finally!)...

The offer is valid until end of Sept..

We aren't part of a chain however the sellers are downsizing and still haven't found anywhere...

Do lenders extend offers if things don't complete by the offer expiry date?

The offer extension policy/process differs from lender to lender. With Halifax, if you haven't completed by 30 Sep, you'll have to pick a new product.

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

@iamiam I don't really have a general opinion on that, whether or not offsets make sense will depend on the borrower's needs/circumstances.IAMIAM said:Thanks. Second question too. Are offset mortgages worthwhile when interest rates are rapidly increasing? What are current rates like on 170k 75% LTV with 50k in offset account (ie 120k being charged interest)

For current rates, you could do a full search with filters using a comparison site like Moneyfacts.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

What happens when contacting a broker? Is it all done online or will there be face to face meetings? Do brokers have offices or would they expect to come to my home?

Sorry if they are stupid questions.Debt Free: 01/01/2020

Mortgage: 11/09/20240 -

@jami74 The channels of communication vary from broker to broker.Jami74 said:What happens when contacting a broker? Is it all done online or will there be face to face meetings? Do brokers have offices or would they expect to come to my home?

Sorry if they are stupid questions.

For example, if you go with Habito the process is -> You fill in an online fact-find (personal and financial details required for the mortgage), then you 'speak' to an adviser over live-chat who then goes away and gives you a mortgage recommendation. Any further communication is usually over email/chat though you can ask to speak over the phone as well. There's no option for face to face appointments.

To take my example, I give advice over phone/video calls and email, I don't offer any face to face appointments. My clients are from across the country and I work flexibly through the week including weekends and evenings to match the availability of clients.

Yet another example would be Estate Agent based brokers who may offer face-to-face and phone appointments.

At present, I personally don't know of any brokers who visit the home of the client but have heard of it anecdotally.

I've waffled a lot! Essentially what I'm trying to say is you should be able to find a broker that suits the way that you would like to communicate.I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

Hello. I was wondering if I could please have some input on my situation?

My partner and I applied for a mortgage with Santander last month through a broker, however, they changed their lending policy midway through the application, averaging my income over 2 years rather than taking my latest year. This led them to come back stating:

We've declined the application because the company or business accounts don't meet our lending policy.

My broker then advised we apply with Aldermore. We received a DIP that was accepted and the full application went in on May 5th. In hindsight, I feel this might have been a bit of a sledgehammer approach going from a high street lender to Aldermore.

New build: £450,000

Deposit: £130,000

LTV: 72%

My situation is:

Company Director owning over 25% of the company. Trading for 5 years. Always profitable.

2020/21:

Salary from company: £8,000

Company net profit: £144,683

My share of net profit: £37,617

2021/22:

Salary from company: £46,371

Company net profit: £264,191

My share of net profit: £68,689

My partner is full time employed earning £16,500 year base and £5,000 year commission (this is regular and paid monthly).

Both have excellent credit scores.

I have a loan of £200 / month.

No dependants.

Since our application went in with Aldermore, Santander have reconsidered and asked for some more documents which I provided.

Having been rejected from Santander originally, I am wondering what our chances are with Santander and Aldermore?

We are up against time with the developer and need to get this sorted.

I guess I am looking for my mind to be put at ease that we will get a mortgage offer.

Thanks for taking the time to read.0 -

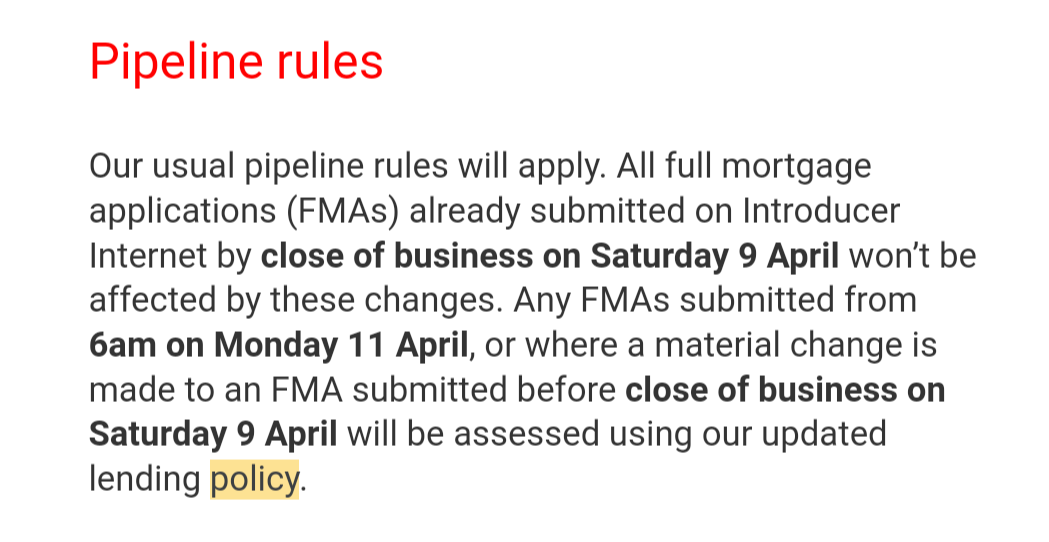

@logon94 This was the Santander notification to brokers re pending applications for this change from latest to average.

So if your full application was submitted on/before Saturday 9 April, your chances of the decision being overturned are better than if the application was submitted after 9 April.

It's not clear to me from the numbers as to why you need affordability to be based on the latest year figures? Even with the average of 80k+20k+ you should more than comfortably be able to meet the required borrowing of 320k with lenders who will use the sal + share of net profit figure as opposed to sal+divs. I personally don't understand the jump from Santander to Aldermore, but that's just based on the limited info in your post.

With regard to your income (sal + share of np), it's going from 45k in 20/21 to 115k in 21/22, so you can expect Aldermore (other lenders as well) to probe the reason for the sharp increase.

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

@K_S thanks so much for your reply. The full application went in on March 22nd, so well before the changes came into effect. I got the decline notification on April 14th.

I am confused as well to be honest as the income and deposit is there to support the £320k we need to borrow.

From your experience, do Aldermore take sal + share of net profit into account? Looking at their lending criteria, it does say sal + dividends or sal + share of net profit:

The increase profit has been due to the company revenue and profits doubling each year since 2018. And the increase in salary is due to the company being able to afford to pay a higher salary this year, rather than me taking a small salary and retaining it in the company profits in previous years.

I have provided my broker with the full, signed company accounts so the lenders have a full picture. I'm just concerned that Aldermore with throw it out.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.8K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards