We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Mortgage broker - ask me anything

Comments

-

@dil1976 Imho when you're ready to start viewing.dil1976 said:I am well on my way to saving my deposit and should be have it all saved by about May or June all being well. How soon should I start talking to a broker so i can find out in depth how much I can borrow etc before putting offers inI am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

You haven’t put enough information on this post.poppyegg22 said:Hi,

am I better using a mortgage advisor/broker or going direct to the bank myself? What are the pros and cons?

On your other post you have stated you’re first time buyers with some late payments on your credit file with a 10% deposit and looking to borrow approx 3.5 x salary

Personally I’d use a broker; they’ll make sure they match you with correct lender for your circumstances and ‘hold your hand’ through the process

I believe you’ll need to mention to them any AIPs you’ve already obtainedMFW 2026 #5007/03/25: Mortgage: £67,000.00

Mortgage:

04/04/26: £33,500

07/03/26: £34,418.15

16/01/26: £56,794.25

02/01/26: £60,223.17

12/08/25: Mortgage: £62,500.00

12/06/25: Mortgage: £65,000.00

18/01/25: Mortgage: £68,500.14

27/12/24: Mortgage: £69,278.38

Savings: £20,0000 -

Did you get sorted?Kernower said:

Thank you for the response.K_S said:Kernower said:Hi,

Just a general query. It appears that my broker is offering me a deal that appears to be more expensive than what I could get directly off the lender’s website.

Is this a regular occurence with brokers?

Same lender, same advance, same term but 0.55% lower rate, £60 a month cheaper.

What benefits am I getting by going via the broker?

Thanks.@kernower No. This most definitely is NOT a regular occurence with brokers. It's most likely a misunderstanding or not comparing like for like (eg: one product with fee and the other no fee, etc). If you can tell me what exactly are the two products that you are comparing, I might be able to throw some light on it.Or else, just ask the broker the same question of why it looks like you get a significantly better deal going direct to the lender.

Broker offered £160k over 18 yrs on a 5 yr fix from Nationwide with no lender fee (but a broker’s fee) at 1.99% for £882 a month with Nationwide.

Directly on Nationwide the same advance, period, fix with a lender fee comes to 1.44% and £841 a month.

Granted I would have to pay a lender’s fee of £999, but if I hadn’t gone via the Broker (who takes a fee also) I would have a mortgage that costs £1,400 less over the 5 yr period. Both deals revert back to the same SVR.

I appreciate that the broker has searched the whole of market and believes that this os the best product, but I had presumed that the most appropriate deal would come from products that weren’t available directly to Joe Public.

Therefore, I presume that I could go with the lender directly but end up paying the product fee and the broker’s fee (as they’ve made a recommendation). Which still provides a saving on the overall cost of the mortgage.

That 1.99% is £3k more expensive than the 1.44% fee based for the same payment.

Using the monthly costs + fee gives a very misleading result if you got that as £1,400.

At the end of the 5years you owe ~£3k less

£160k 1.99% £882pm £121,130

£161k 1.44% £882pm £118,1740 -

Hi, I was wondering if a broker can assist please. Do you have a timescale for mortgage applications with Ipswich Building Society?0

-

decs2021 said:Hi, I was wondering if a broker can assist please. Do you have a timescale for mortgage applications with Ipswich Building Society?@decs2021 I haven't used them in ages, but these are the published service levels on their intermediary website https://ipswich-intermediaries.co.uk/

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

0 -

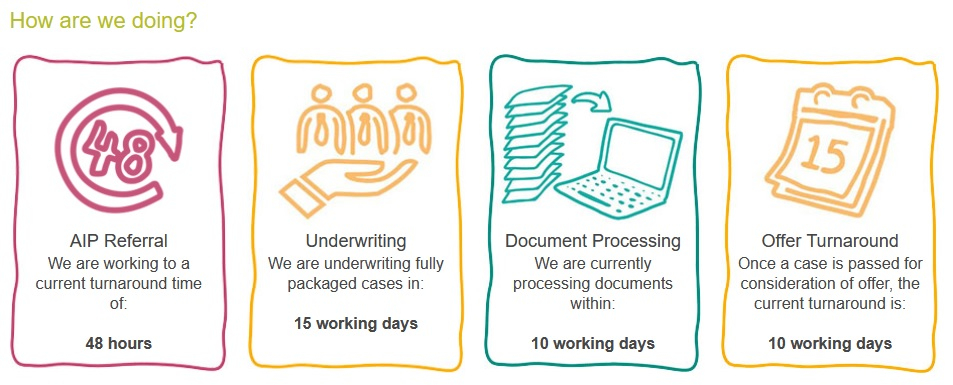

Thanks for that. I am assuming those images are in the same order as the process? Ahh if only they had guidance on the valuation on there! I guess all in all we are looking at month from submitting to offer.K_S said:

0 -

Hello! Thanks for this thread. Much appreciated.

Not one for now, but helpful for understanding my long-term future.

I'm joint-holder of a mortgage with nearly ex-wife. The divorce process starts soon as we've been separated for two years. It's amicable, and because I earn a lot more than her (I'm on six figures, she's just doing part-time work for spending money) I'm going to put a Mesher order on the property as part of the divorce agreement so that she can stay there with our 7yr old son, so essentially I have to mentally write that property/asset off as mine, despite the fact that I pay 100% of the mortgage and likely always will.

My question is about what the implications are for me buying a property of my own at some point in the future. As a mortgage holder I obviously won't qualify for any first-time buyer or help to buy offers, I assume, but will it prevent me from getting a normal mortgage? And how does this impact affordability scores, etc?

I guess my question is whether I'll be renting for life now!

Thanks very much in advance.0 -

@havelt The background mortgage will have an impact on your affordability for a future purchase. How much of an impact will depend on your income, your financial commitments (running costs of your ex's house plus anything else), your deposit and how much you want to borrow. It won't by itself "prevent" you from a future mortgage to buy a house to live in.HaveIt said:My question is about what the implications are for me buying a property of my own at some point in the future. As a mortgage holder I obviously won't qualify for any first-time buyer or help to buy offers, I assume, but will it prevent me from getting a normal mortgage? And how does this impact affordability scores, etc?

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1 -

Hi, is it true that childless couples get better mortgage deals than one with a child/children?0

-

HamSoulo said:Hi, is it true that childless couples get better mortgage deals than one with a child/children?@hamsoulo Not quite. A couple with no dependents *may* have a higher max borrowing than a couple that do.As per lender calulcations, the number of dependents (and associated costs such as childcare) may bring down your affordability and affect how much you can borrow.

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.9K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.7K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.4K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards