We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Paralyzed with indecision.

I'm a 30 year old male, married, my wife is 33. I think we're doing quite well financially, but I feel a bit "lost", I'm unsure what the "best" thing is to focus on. Our situation is as follows:

- Combined (take home) pay: £550.00 weekly

- Bills: £200.00 weekly

- No debt (except mortgage)

- Mortgage balance: £91,000.00 (2.80% interest) (27 years remaining) (Remortgaging August 2022) (House value approx: £120,000.00)

- My current pension value: £26,000.00

- Wifes pension value: £10,000.00

- Vanguard ISA value: 16,000.00

- Emergency Fund: £5,000.00

- Spending money: £2,600.00

The purpose of the Vanguard ISA is to "offset" the balance of the mortgage, over time I'd like the ISA value to become equal to the balance of the mortgage, because at that point, we can choose to pay off the mortgage entirely, if we wanted too (or had too). I'm unsure if it's the "best" decision though. I'm just looking for some outside perspective, is there anything you see that can be improved on? Is my ISA a poor idea? Are the pensions lagging? Should I be focusing more on the pensions? Is giving the money to the mortgage lender a better idea instead of the ISA? I feel like my only "obstacle" left is the mortgage, but focusing entirely on it could come at a huge opportunity cost? There's just so many options, I guess I'm just looking for some advice from people who know better.

Thanks

Comments

-

Aw, I'm so sorry you are worrying because you seem to be doing great, to me. But then I'm someone who made a complete hash of finances when my marriage broke down and has been trying to catch up ever since! I have learned a lot though, from all my mistakes. In your position, I'd contact an accountant or a financial adviser and ask if I could have a one-off appointment to discuss matters. That may well put your mind at ease, even if you have to pay for the privilege.

You and your wife are so very young, you need to be enjoying life, instead of worrying about things that you don't really need to, by the looks of your post.

And that's my advice, for what it's worth.

Please note - taken from the Forum Rules and amended for my own personal use (with thanks) : It is up to you to investigate, check, double-check and check yet again before you make any decisions or take any action based on any information you glean from any of my posts. Although I do carry out careful research before posting and never intend to mislead or supply out-of-date or incorrect information, please do not rely 100% on what you are reading. Verify everything in order to protect yourself as you are responsible for any action you consequently take.1 -

How much are you putting in your pensions each month? Are you putting enough in to get the maximum employers contribution (that should be an absolute minimum amount to put in)Your mortgage Rate seems high hopefully you can get it lower in two years time. Is the ERC too high to make it worthwhile to do it now? If it is then any you do pay off now is at an effective "savings" rate of 2.8% better than you'd get elsewhere by far.

i agree, focussing entirely on your mortgage does cut off opportunity costs longer term.

Overall I'd say you seem to be doing well.One other focus - what can you do to increase your earnings ?1 -

The better idea would be to use the 16k in the ISA to reduce your mortgage now.

It would increase your cash flow slightly and give you the option of maintaining current mortgage repayments and clear mortgage earlier. I would urge you to put clearing the mortgage as your number one financial objective.

Check t&c's with mortgage provider..._1 -

The Vanguard ISA isn't an appropriate vehicle to "offset" the mortgage. It is a capital at risk vehicle whereas the mortgage is not. At any given point the Vanguard ISA may drop 30, 40, 50% whereas your mortgage cost is fixed. That said, it's not a bad thing you have this ISA, you just may need to be more flexible with it - in that in the future if the balance of it is close to matching a mortgage, then you simply wait out any volatility if you're wanting to pay off the mortgage but the ISA value has declined, which may take years. If you aren't content with being more flexible then the Vanguard ISA isn't appropriate and you should move it to a non-capital at risk vehicle instead. Ultimately the most efficient thing if you choose to do that will simply be to pay down the mortgage, which at 2.8% interest is more than what you will earn in any Cash ISA or savings account.

Apart from that, there's not a lot of leeway room for you I'm afraid. Your £2,000 a month combined take home with respect isn't a lot, and limits your ability to take advantage of tax efficient options, primarily because such options impact on cash flow and you may quickly find yourself in a position where you don't have enough to make ends meet and you're dipping into savings because you're saving/investing too much based on your salaries. This is likely to become more acute if you decide to have children, which will take a toll on your cash flow. So, what can you do to increase your income? You're both still relatively young, with ten years still until you reach the age when most people are reach their peak earnings., so it's not so much an issue now if you have a path to earning a bit more, at which point you'll likely want to increase pension contributions.

Only other thing is your bills - £800 a month, not including mortgage. Seems high to me considering gas, electricity, water, internet/phone, council tax should set you back about £300. What else are you paying out for? Possibly feels like you may be spending on car finance? If so - review whether the car(s) is/are necessary, failing that if you can share a car, failing that if you can get a less expensive car.

1 -

I’m slightly older (34) with a higher net worth (I say that not as competition but for context) but ratios are not dissimilar and I find myself asking similar questions.

Advice on here does seem to be conflicting but for what it is worth I split my monthly savings 3 ways (often equally) - cash savings, S&S ISA and mortgage over payment (taking on board the advise above that higher pension is the most tax efficient approach and certainly worth putting in as much as you need to to get full employer contribution).It won’t be the most efficient approach but I sleep easy at night with it.3 -

I extend on this point. At your age, the best investments are yourselves. Worrying about what a few grand in the bank is making in interest is far inferior to using that money to help make your career go better. Education, training or items that buy you more time in life to focus on the things that are important if far more valuable.AnotherJoe said:One other focus - what can you do to increase your earnings ?1 -

It's good to be thinking about these things, getting some perspectives from top to bottom on your finances and setting yourself some goals. No one else will do it for you and it's in your own best interests to take responsibility. Being worried about it is part of the process and there is plenty of great advice on this forum to help you build your knowledge and get a plan you are comfortable with.

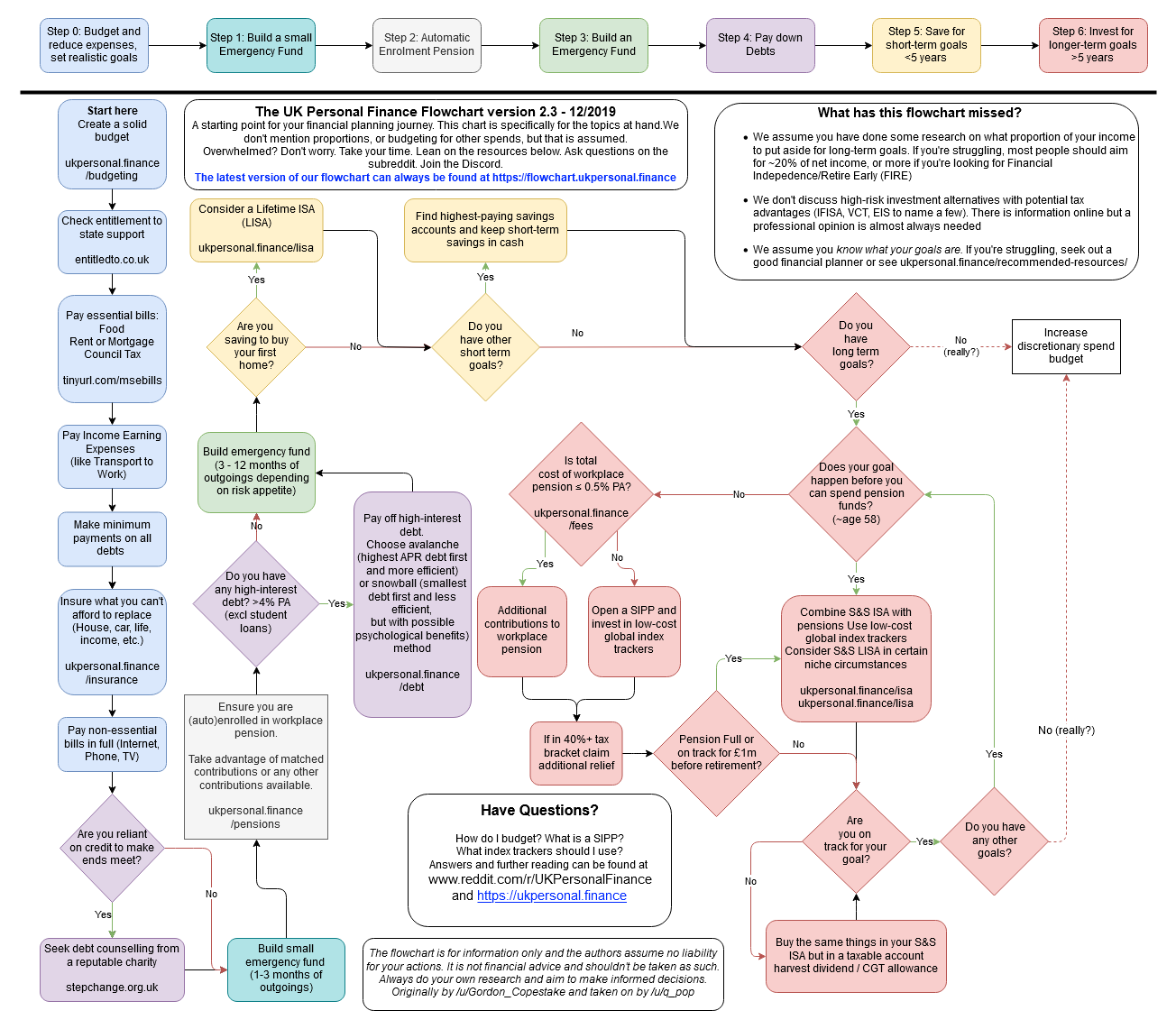

At a high level the typical steps are:

1. Clear Debts. Pay off high interest debt, credit cards etc.

2. Emergency fund. Build an emergency fund to cover all bills for 3-6 months - and store in a readily accessible account, perhaps a instant access saver account or, at the moment, NS&I income or premium bonds. Interest rates are low but the idea here is:- the money is readily accessible;

- the money is guaranteed (i.e. not invested);

- the money is not typically spent except in exceptional circumstances, defined by you. e.g. to cover your mortgage and bills in the event of losing your job? to cover car repairs? etc.

3. Maximize your pension contributions. You don't say whether you or your partner are still contributing to your pensions, or the type of pensions. Are they "direct contributions - DC"? Does your employer contribute? Can you maximize you or their contributions further? And lastly, where is the money invested? Pension providers (Legal and General, Scottish Widows, Standard Life etc.) offer a number of pension fund options so you must check which you are invested in.

4. Utilise your stocks and shares ISA. Invest in a method you are comfortable with. Investing is one option available to grow your money in accordance with your goals. You say you have a vanguard ISA but do you know where that money is invested? The ISA is just the tax free wrapper, Vanguard is the provider, and the money is actually invested in a fund or ETF of some sort. You should understand where your money is invested. You don't say how much you are able or willing to invest regularly, but you ISA allowance is currently 20k per year.

To help with points 3 and 4 (where should your money be invested) I would recommend watching this six part series of videos, and subsequently buying this book.

I pinched the below flow chart from a reddit page, but it outlines the above in more detail.

As for the "pay the mortgage vs invest the money" question, statistically speaking, based on empirical data available to date, it can be beneficial to invest money for a 20 year period and expect it to have greater net wealth than if you had used that money to pay off your mortgage. It is not guaranteed as is the nature of investing. Furthermore there is an emotional factor associated with paying off your mortgage that cannot be quantified in terms of "what's the best monetarily."

Hope that helps.

6 -

There's just so many options, I guess I'm just looking for some advice from people who know better.

Some people may well have more background knowledge than you but opinion and personality play a big role in how different people would behave in the same situation, and in the end you have to make your own decision. Just to add my bit .

Personally I would like to see more of the mortgage paid off first and then when you remortgage in two years it will be at a better LTV and you hopefully get an even lower interest rate and the advantage of having less debt . Then may be a better time to think about diverting more funds to investments. Maybe a tweak upwards of pension contributions could be a good idea though.

In the meantime review your actual investments within the pensions and S&S ISA. At your age pension investments should be ones with the potential for high growth as you can ignore the associated short term volatility that comes with this type of investment.

I'd contact an accountant or a financial adviser and ask if I could have a one-off appointment to discuss matters

Regarding this point made above , you do not want to see an accountant about personal finance . Quite probably they will not have a clue. If you do see an advisor , although not obviously necessary in your case, make sure it is an IFA ( I is for Independent) and do not go to your bank, building society.

2 -

I agree with this, and I disagree with the following sentence about paying off the mortgage - but that is my personal preference to extending leverage to get money into pension. Neither are wrong answers, just personal preferences based on age, income, assets, personality etc.Albermarle said:There's just so many options, I guess I'm just looking for some advice from people who know better.Some people may well have more background knowledge than you but opinion and personality play a big role in how different people would behave in the same situation, and in the end you have to make your own decision. Just to add my bit .

3 -

Dr0o said:Hello.

I'm a 30 year old male, married, my wife is 33. I think we're doing quite well financially, but I feel a bit "lost", I'm unsure what the "best" thing is to focus on. Our situation is as follows:

- Combined (take home) pay: £550.00 weekly

- Bills: £200.00 weekly

- No debt (except mortgage)

- Mortgage balance: £91,000.00 (2.80% interest) (27 years remaining) (Remortgaging August 2022) (House value approx: £120,000.00)

- My current pension value: £26,000.00

- Wifes pension value: £10,000.00

- Vanguard ISA value: 16,000.00

- Emergency Fund: £5,000.00

- Spending money: £2,600.00

The purpose of the Vanguard ISA is to "offset" the balance of the mortgage, over time I'd like the ISA value to become equal to the balance of the mortgage, because at that point, we can choose to pay off the mortgage entirely, if we wanted too (or had too). I'm unsure if it's the "best" decision though. I'm just looking for some outside perspective, is there anything you see that can be improved on? Is my ISA a poor idea? Are the pensions lagging? Should I be focusing more on the pensions? Is giving the money to the mortgage lender a better idea instead of the ISA? I feel like my only "obstacle" left is the mortgage, but focusing entirely on it could come at a huge opportunity cost? There's just so many options, I guess I'm just looking for some advice from people who know better.

Thanks")

Firstly, you are doing well.Probably it would be wise to put your thought and worry into your careers and lives rather than improving your financial management, which is already pretty good.

Secondly, your mortgage interest rate is rather high: take note of the comments on this and ask if anything is not clear.

Thirdly, I note that by the time you expect to pay off your mortgage you will be old enough to take out money from a SIPP or pension scheme. Because of the tax advantages to saving in such a scheme, you might consider putting enough money into your pension savings to cover the mortgage as well as providing a pension.

I doubt whether you would gain anything from a meeting with an accountant or financial advisor. The main thing that an IFA could do is suggest ways to invest your ISA and pension savings, but the amounts are relatively small and so it would not make much difference.

2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards