We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Pension tranfer - what would you do?

Comments

-

Mine is currently sitting at £142 a week and if I continue to contribute for the next 7 years or for 7 years prior to 2042 then it will max out at £175.20.xylophone said:Has your fiancee any pension provision of her own?

Have you checked your state pension position?

Has she?

https://www.google.com/search?q=state+pension+forecast+uk&oq=state&aqs=chrome.1.69i59l3j69i57j46j0j46l2.3910j0j15&sourceid=chrome&ie=UTF-80 -

You are lucky you can transfer but its generally been said transferring isn't necessarily a good idea.Cypruseast said:I know this type of debate has probably been done to death but I am keen to get other's views on this matter. Ok so the long and short of it is I am 44 yrs of age, I have two pensions - a DB pension (from a previous employer) and a DC pension (with current employer). The scenarios are as per below:DC Pension- Contributing £13.75k per annum (about 22% of salary) - NB I have increased this amount from about 12% per annum over the past 9 months- Current value £273k after some 12 yrs of contribution and growthDB Pension- Normal Retirement Date 31/01/41- Start date 05/07/98- Date of leaving the scheme 12/08/07- Annual pension at date of leaving £7.75k per annum- Estimated annual pension on normal retirement date of £10.4k per annum (31/01/41)- Estimate annual pension on retirement date of 31/01/38 £9.0k- Transfer Value (current estimate) £349.5kBasically as we all know life has it's twists and turns and I find myself in the situation of having a new partner who I am due to marry next year. My partner is more than 10 years younger than me and was not with me when I left my DB pension scheme. According to the terms of the scheme a spouse would retail 2/3rds of my pension upon my death, but this reduces based on the two factors which ultimately will effect my spouse. So, she will get a very significantly reduced spousal pension and added to that as far as I can see there are no lump sum benefits payable from the scheme if I die before taking my pension.I expect to be gainfully employed for the next 17-18 yrs and would ideally like to retire in and around early 2038 when I will be nearly 63 yrs of age. Other aspects are I have a child of 1, 10 and a step daughter whom is 11.Based on the above I previously reviewed the option to transfer out my DB benefit payment to my current DC scheme (or other). I felt that based on my personal situation or certainly the impact that it could have on my spouse and other dependents, that it may be in all of our interests to look at moving that pension to allow for hopefully some growth over the next 18 years but obviously given the 11 yr age gap and the pension scheme rules that my wife and dependents could benefit for a longer period of time from my pension (s) if outside of the DB scheme. The UK life expectancy is say approx. 84 yrs of age for a man of my current age. So by that stage assuming life doesn't change my wife to be is going to be 73 yrs of age with a life expectancy of a further 15yrs ahead of herself. Based on appox £9k per annum and assuming I achieve my life expectancy I would release £138k of value from my pension and the rest would die with me, whereas I could release some £350k now to invest for the next 18yrs in a way that my wife would be able to access even after my death (assuming that comes first).I did (eventually) find a company that was prepared to offer the necessary financial advice required as it was over 30K and complete the transfer approx 12 months ago for a reasonable rate. However, very quickly prior to getting a locked in value at the then transfer rate of about £356k the transfer value reduced by £50k in a couple of weeks so I shelved the idea. It has slowly been increasing over the past 12 months and is currently close to what it was a year ago so the question has arisen again on what to do - do I leave well enoigh alone and have the security of a DB pension that will die with me or take the cash and re-invest so my family can potentially benefit from a longer time frame from it....So what would you do?1 -

Only quoting the above for brevity.Cypruseast said:DB Pension- Normal Retirement Date 31/01/41- Start date 05/07/98- Date of leaving the scheme 12/08/07- Annual pension at date of leaving £7.75k per annum- Estimated annual pension on normal retirement date of £10.4k per annum (31/01/41)- Estimate annual pension on retirement date of 31/01/38 £9.0k- Transfer Value (current estimate) £349.5k

I dont understand why a pension of £7.75k pa in 2007 only grows to £10.4k pa in 2041.

I am more inclined to believe that the £10.4k pa figure is the value now?1 -

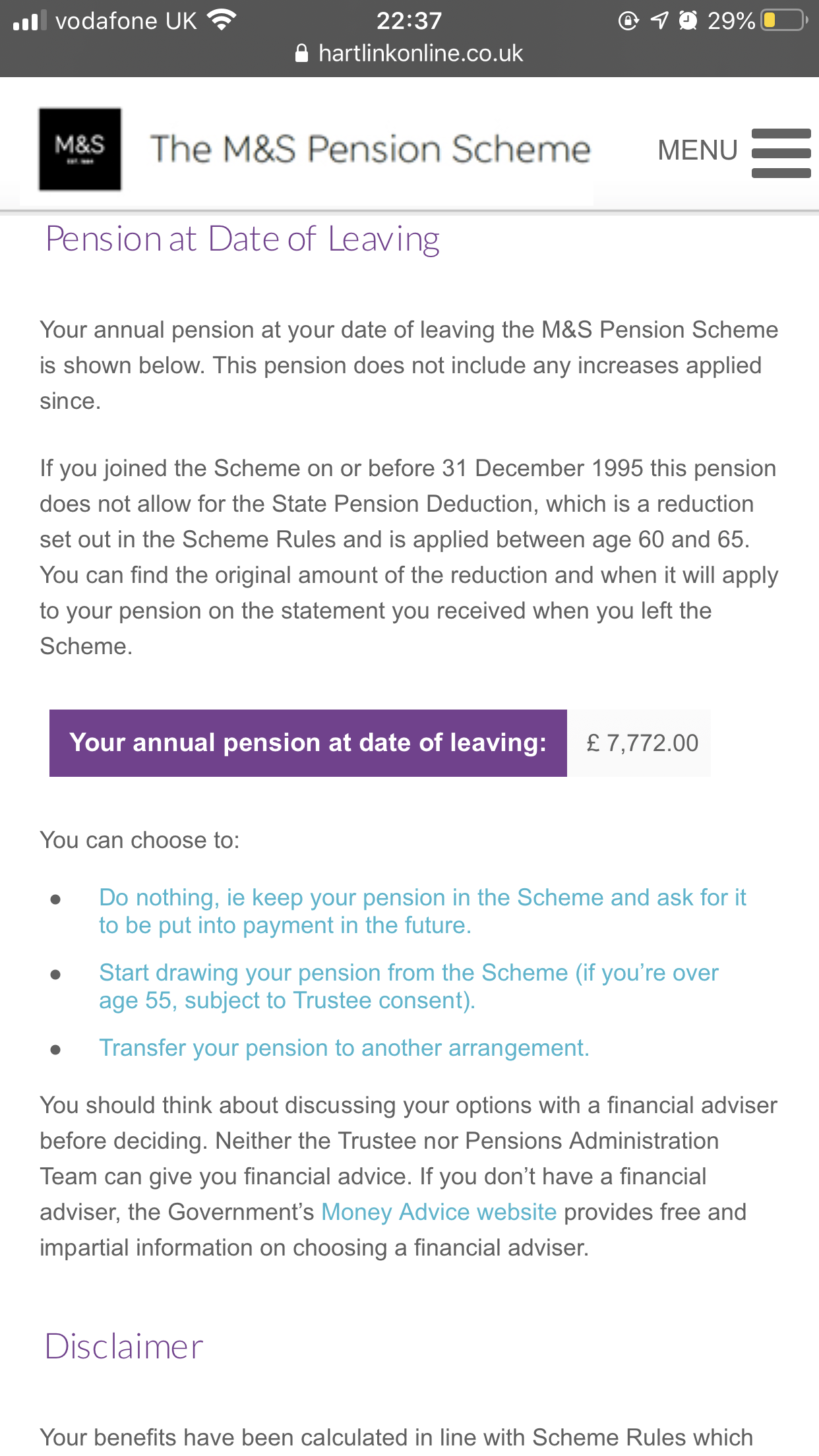

Below is the attached information from their website...garmeg said:

Only quoting the above for brevity.Cypruseast said:DB Pension- Normal Retirement Date 31/01/41- Start date 05/07/98- Date of leaving the scheme 12/08/07- Annual pension at date of leaving £7.75k per annum- Estimated annual pension on normal retirement date of £10.4k per annum (31/01/41)- Estimate annual pension on retirement date of 31/01/38 £9.0k- Transfer Value (current estimate) £349.5k

I dont understand why a pension of £7.75 pa in 2007 only grows to £10.4k pa in 2041.

I am more inclined to believe that the £10.4k pa figure is the value now?

0 -

I suspect that the £10.4k figure is the value now.

If we increase the 2007 figure by 2% per year up til now (a reasonable, possibly understated, inflation assumption for the 13 year revaluation period) then the £7.75k becomes £10.2k

As they do not know what future revaluation rates will be i think they are ignoring it.

At least the £10.2k gives you a reasonable idea of your final oension in today's money terms. And it is close to the £10.4k they are quoting.1 -

I suggest leaving it where it is for now and reconsidering much closer to age 55 or if UK interest rates start to rise. There are two main sets of reasons for this suggestion:

1. The transfer value normally increases the closer you get to being able to take the income, without you bearing investment risk. Higher interest rates normally decrease transfer values.

2. The lifetime allowance, which I'll pretend is a million for simplicity.

At present the DB would use 20 * 10422 = 208k, leaving 702k for the DC.No problem today since it's 273k but what about growth? UK market has grown at around 5% plus inflation so say you get 4% plus inflation. 11 years of that takes you to 54% growth to 420k. 19 years would add 110% in growth to 575k. But that's assuming you make no more pension contributions and you probably will.

Say you transfer now, taking you to 622k of DC. 11 years takes that to 957k and 19 to 1310k and a substantial lifetime allowance charge even with no more pension contributions.

At this point it looks as though keeping the DB income even with a reduced spousal payment and considering retiring closer to 55 might be worthwhile. ISA investing can be used to further supplement retirement investing.

1 -

And you could consider opening a SIPP for your partner to cover her if the spouse pension is lost.

0 -

I suspect that the £10.4k figure is the value now.

I am sure it is . However in the original post the OP took the transfer value of £350K today added 2.5% pa for 21 years and got £550K, from which he could generate an income of up to £25K .

This ignored the effect of inflation over the next 21 years , which would roughly bring home back where he started ( unless he generated more growth with better/riskier investments )

Anyway the LTA argument of James D pretty much knocks the idea on the head anyway . I was wavering with my DB transfer value a couple of years ago but as it would have pushed me over the LTA , it was a non starter for that reason,

0 -

Regardless of LTA it is always useful to have a decent (and this amount is) guaranteed income on top of the state pension anyway.Albermarle said:I suspect that the £10.4k figure is the value now.I am sure it is . However in the original post the OP took the transfer value of £350K today added 2.5% pa for 21 years and got £550K, from which he could generate an income of up to £25K .

This ignored the effect of inflation over the next 21 years , which would roughly bring home back where he started ( unless he generated more growth with better/riskier investments )

Anyway the LTA argument of James D pretty much knocks the idea on the head anyway . I was wavering with my DB transfer value a couple of years ago but as it would have pushed me over the LTA , it was a non starter for that reason,

0 -

I would agree and I would most likely not have taken the CETV without the LTA issue for this reason.garmeg said:

Regardless of LTA it is always useful to have a decent (and this amount is) guaranteed income on top of the state pension anyway.Albermarle said:I suspect that the £10.4k figure is the value now.I am sure it is . However in the original post the OP took the transfer value of £350K today added 2.5% pa for 21 years and got £550K, from which he could generate an income of up to £25K .

This ignored the effect of inflation over the next 21 years , which would roughly bring home back where he started ( unless he generated more growth with better/riskier investments )

Anyway the LTA argument of James D pretty much knocks the idea on the head anyway . I was wavering with my DB transfer value a couple of years ago but as it would have pushed me over the LTA , it was a non starter for that reason,

The LTA issue just made the decision easier.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards