We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

GMP pension estimate and revaluation in deferrment

Comments

-

Please come back and let us know the outcome. Sounds as if it is the proverbial 'human error' !WobblyDog said:Brynsam said:OP - did you transfer in benefits from another scheme, or pay voluntary contributions?When I started the job it was a Civil Service post, so I was in the Civil Service pension scheme. When my employer was privatised, my pension was transfered to a private sector DB scheme run by the employer. The pension statement I have dated April 2000 (after privatisation) says "PCSPS Credit: 5years 305days".I didn't pay voluntary contributions.I'm beginning to suspect that the person who wrote the 2013 letter transposed the GMP and non-GMP figures. That would give a GMP pension at 65 that's quite close to the £30/week COPE estimate, and I've read that "COPE estimate" should approximately match the GMP pension.I think I will send a scan of the 2013 letter to the pension scheme asking them if it's correct.0 -

Hi, hope I'm not hijacking this thread but after reading it I had a look at my other half's deferred pension and tried to work out the figures. It seems similar to Wobblydogs. Can someone help with the calculations? I'm pretty confused.

In 2017 when he enquired about it and asked for a statement he was sent the following:

Deferred pension at 1996 = £2767.97

Deferred pension at 2017 = £5689.20

Benefits in the scheme are based on completed pensionable service and final pensionable salary. Pensionable service is 8 years and 4 months and final salary £19930.18.

On the date of leaving the scheme you have earned a deferred pension of £2767.97 a year, which becomes payable at your normal pension date of 2030.

The pension shown above will increase from your date of leaving the scheme to age 62.

Your gmp of £438.36 will increase at 7% a year compound between your date of leaving and age 62.

Your benefits above your gmp will increase by the rise in cost of living in the UK or 5% a year compound, whichever is the lower, over the period between your date of leaving and age 62.

Is it possible to work out the formula they have used to understand how the pension has gone up over the last 21 years from these figures? It would be helpful to predict roughly what his final pension per year would be when he reaches 62 (he is currently 52).

Any help appreciated (in idiot form please, I'm not the best at maths)! Thanks

Just my opinion, no offence 🐈0 -

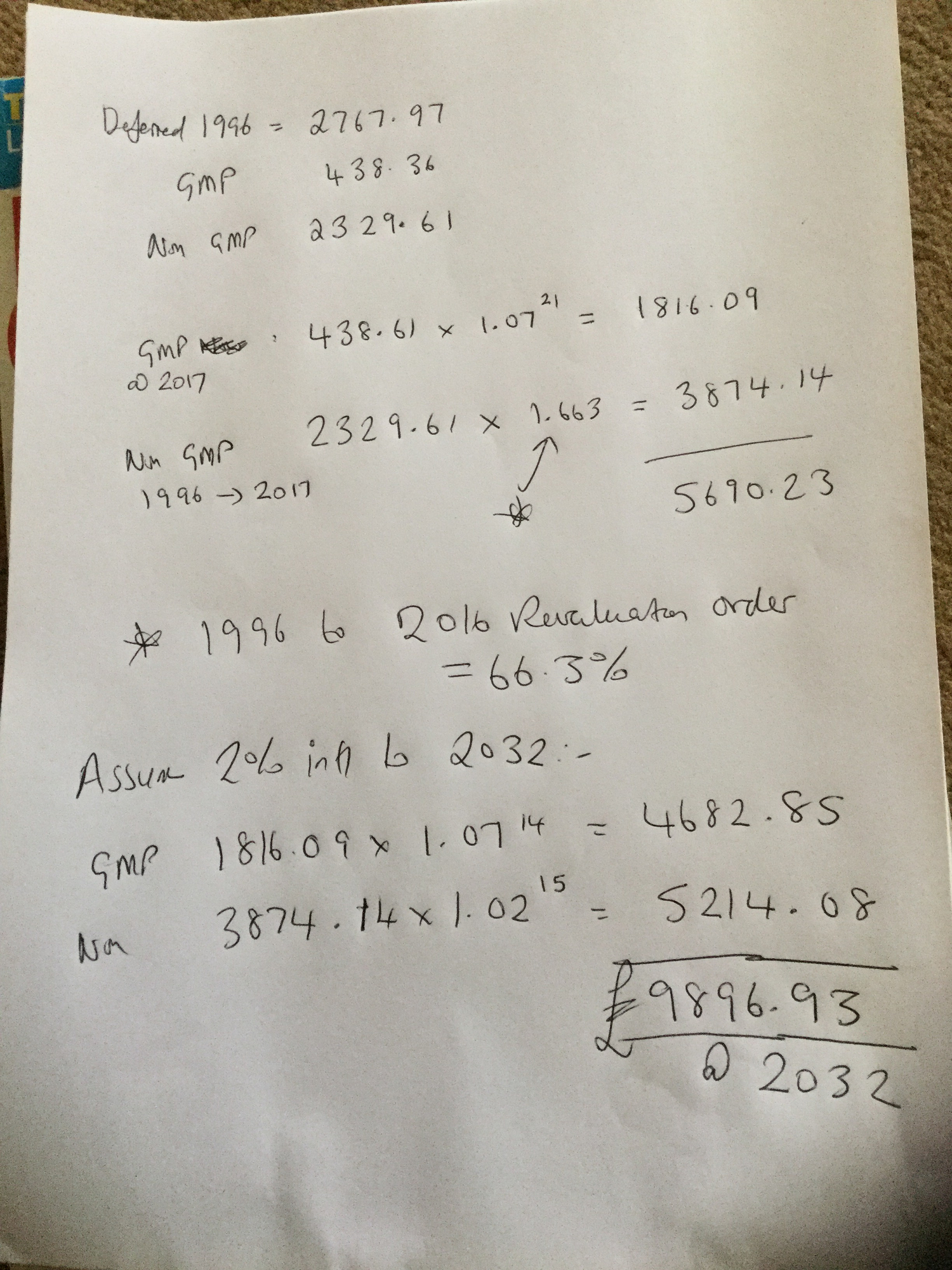

I can get within £1 of your 2017 figure ...Black_Cat2 said:Hi, hope I'm not hijacking this thread but after reading it I had a look at my other half's deferred pension and tried to work out the figures. It seems similar to Wobblydogs. Can someone help with the calculations? I'm pretty confused.

In 2017 when he enquired about it and asked for a statement he was sent the following:

Deferred pension at 1996 = £2767.97

Deferred pension at 2017 = £5689.20

Benefits in the scheme are based on completed pensionable service and final pensionable salary. Pensionable service is 8 years and 4 months and final salary £19930.18.

On the date of leaving the scheme you have earned a deferred pension of £2767.97 a year, which becomes payable at your normal pension date of 2030.

The pension shown above will increase from your date of leaving the scheme to age 62.

Your gmp of £438.36 will increase at 7% a year compound between your date of leaving and age 62.

Your benefits above your gmp will increase by the rise in cost of living in the UK or 5% a year compound, whichever is the lower, over the period between your date of leaving and age 62.

Is it possible to work out the formula they have used to understand how the pension has gone up over the last 21 years from these figures? It would be helpful to predict roughly what his final pension per year would be when he reaches 62 (he is currently 52).

Any help appreciated (in idiot form please, I'm not the best at maths)! Thanks It may be worth £9,896 in 2032 if the non GMP increases at 2% pa.

It may be worth £9,896 in 2032 if the non GMP increases at 2% pa.

GMP revalues every April so assume 14 years for that and 15 for non GMP from 2017.5 -

I did 2032 for some reason. For 2030 just redo my figures replacing 14 by 12 and 15 by 13.Black_Cat2 said:Apologies missed your end bit. Thank you 🐈😁1 -

Deferred pension at 1996 looks OK too. In fact it is spot on ...

£19,930.18 x 8.333 / 60 = £2,767.971 -

I have calculated it to be £9101.79 per year with your workings out. Couldn't have done it without you tyvm. Hopefully the company/scheme will still be going in 10 years time 😁Just my opinion, no offence 🐈0

-

There's always the Pension Protection Fund if it isn't!Black_Cat2 said:I have calculated it to be £9101.79 per year with your workings out. Couldn't have done it without you tyvm. Hopefully the company/scheme will still be going in 10 years time 😁1 -

Or the scheme may be 'bought out' with an insurance company (the trustees pay an insurer the amount necessary to cover members' benefits in full). Don't panic if that appears on the horizon!Black_Cat2 said:Hopefully the company/scheme will still be going in 10 years time 😁Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!1 -

That is very unlikely because it is such an expensive option. It can happen though.Marcon said:

Or the scheme may be 'bought out' with an insurance company (the trustees pay an insurer the amount necessary to cover members' benefits in full). Don't panic if that appears on the horizon!Black_Cat2 said:Hopefully the company/scheme will still be going in 10 years time 😁1 -

(he is currently 52).

Has he obtained a state pension forecast? Have you?

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards