We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Understanding Pension Revaluation Orders

garmeg

Posts: 771 Forumite

These are the latest rates for non GMP as at 31/12/2019

The last column only appears from 2009 which I guess is when the revaluation changed from RPI to CPI if the scheme rules were worded to allow for it.

Two questions ...

(1) Because CPI is lower than RPI I would expect the figures in the last column (CPI) to be lower than the second column (RPI) but they are the same - why?

(2) The revaluation is capped at 2.5% or 5% depending on scheme rules but i dont see different rates depending on the cap used - perhaps the cap hasn't bitten post 2009.

Confused!

Two questions ...

(1) Because CPI is lower than RPI I would expect the figures in the last column (CPI) to be lower than the second column (RPI) but they are the same - why?

(2) The revaluation is capped at 2.5% or 5% depending on scheme rules but i dont see different rates depending on the cap used - perhaps the cap hasn't bitten post 2009.

Confused!

0

Comments

-

See https://www.oldmutualwealth.co.uk/Adviser/literature-and-support/knowledge-direct/pensions/escalation-and-revaluation/defined-benefit-occupational-pensions/ and scroll down to the bit about revaluing in deferment.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0

-

Thanks.Marcon said:See https://www.oldmutualwealth.co.uk/Adviser/literature-and-support/knowledge-direct/pensions/escalation-and-revaluation/defined-benefit-occupational-pensions/ and scroll down to the bit about revaluing in deferment.

This doesnt explain the two factors and why they are currently the same. Also doesnt show how the cap levels apply - are they year on year or over the whole deferred period. Legislation is unclear. I am trying to quantify the current level of a deferred pension I have and the rules seem unclear for non GMP. Surprisingly the GMP calculation is easier!0 -

Nothing to do with CPI/RPI. Those figures both include the change to CPI which was in 2011, not 2009. It's the cap change. This year they're the same because it never exceeds 2.5% pa compounded going backwards. But if you look at 2018 revaluation order https://www.legislation.gov.uk/uksi/2018/1218/madeyou can see there's a difference in the 2 year period because CPI compounded over 2 years, of 2.4% and 3%, which is 5.5%, exceeded 2.5% compounded which is 5.1%.

0 -

garmeg said:

Thanks.Marcon said:See https://www.oldmutualwealth.co.uk/Adviser/literature-and-support/knowledge-direct/pensions/escalation-and-revaluation/defined-benefit-occupational-pensions/ and scroll down to the bit about revaluing in deferment.

This doesnt explain the two factors and why they are currently the same. Also doesnt show how the cap levels apply - are they year on year or over the whole deferred period. Legislation is unclear. I am trying to quantify the current level of a deferred pension I have and the rules seem unclear for non GMP. Surprisingly the GMP calculation is easier!The figures are for the period of deferment. Complete years of deferrment are used, for instance if you left the scheme in Aug 2010 and you took the pension in July 2020, that would only be 9 complete years and you'd get the 9 year figure (2011-2019 inclusive) whereas if you take the pension in Sept 2020 that's 10 complete years and you'd get the 10 year figure (2010-2019). They're worked out by compounding the Sept CPI figure (or RPI pre 2009) for the relevant years.If the scheme uses RPI still then you'd get a different figure, worked out in the same way but based on Sept RPI compounded, this will likely be higher.This can lead to some strange effects for instance if you left in a year when inflation was high, and inflation is now low, then you're likely to see the pension drop on 1st Jan every year then rise on the anniversary of you leaving the scheme.0 -

Thats great thanks. Some schemes are still having to revalue at RPI because of the wording in the scheme rules. Is there a separate revaluation order table for these schemes, because they definitely need one and my scheme is one of the unlucky ones (lucky for the members though!).zagfles said:Nothing to do with CPI/RPI. Those figures both include the change to CPI which was in 2011, not 2009. It's the cap change. This year they're the same because it never exceeds 2.5% pa compounded going backwards. But if you look at 2018 revaluation order https://www.legislation.gov.uk/uksi/2018/1218/madeyou can see there's a difference in the 2 year period because CPI compounded over 2 years, of 2.4% and 3%, which is 5.5%, exceeded 2.5% compounded which is 5.1%.

I also see that compounding is over the whole period because 1.024 x 1.025 = 1.0496 < 1.051 = 1.025 x 1.025. This is to the members advantage, eg 9 years of no inflation and one year of 20% would yield a total increase of 2.5% over 10 years if each year was separate (1 x 1 x ... x 1.025) or 20% (min (1.025^10, 1.20)) if the calculation was over the whole period0 -

Don't think they publish an RPI table, but you can work it out by compounding the Sept RPI from the relevant years. Cap unlikely to take effect unless you've only got a few years of deferment and inflation rises a lot.

1 -

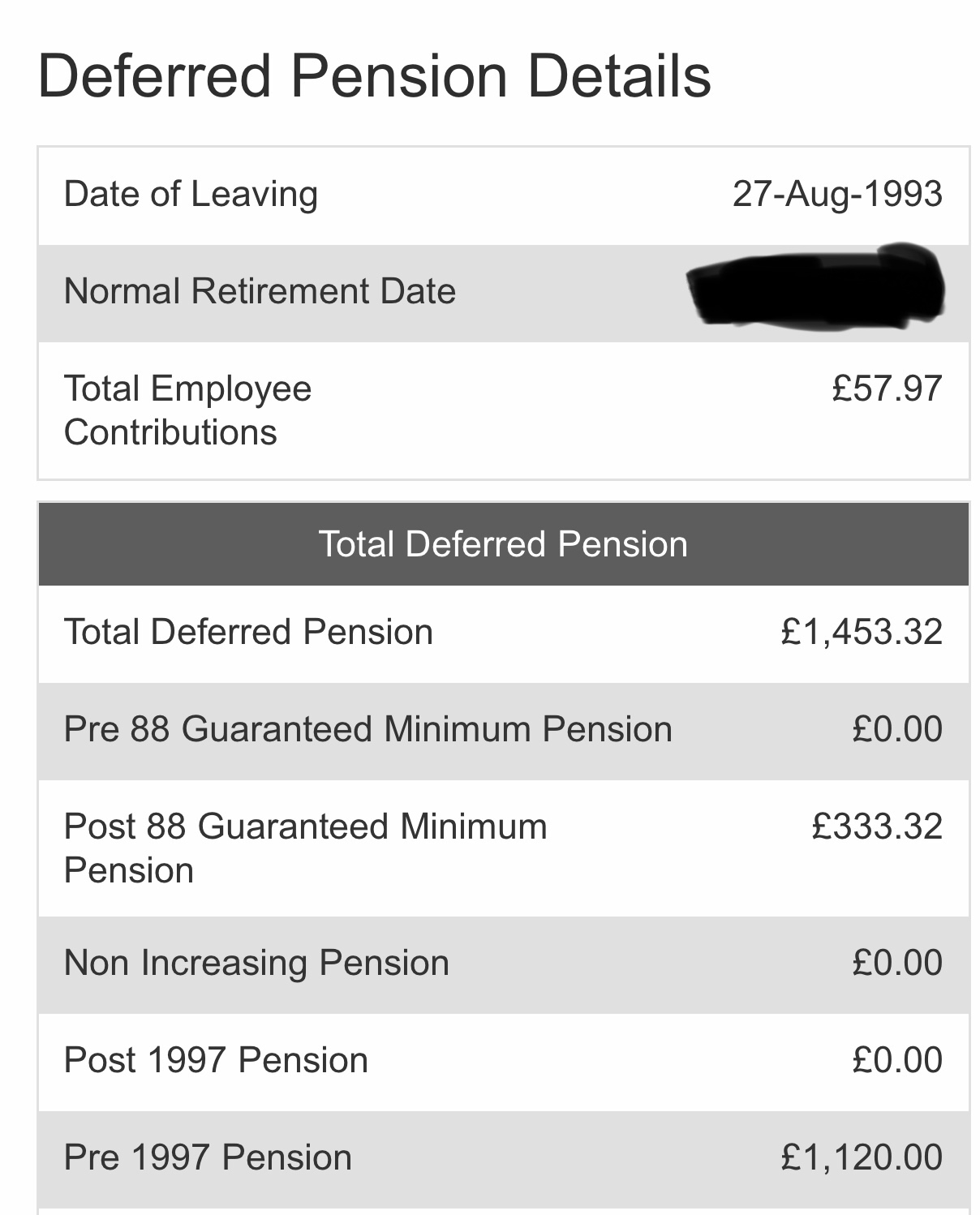

I deferred in 1993 and have 7% GMP revaluation - kerching!zagfles said:Don't think they publish an RPI table, but you can work it out by compounding the Sept RPI from the relevant years. Cap unlikely to take effect unless you've only got a few years of deferment and inflation rises a lot.0 -

Indeed. Downside is no indexation in payment on pre 1988 GMP, so when you get to about 120 you might have lost all those increases to inflation...garmeg said:

I deferred in 1993 and have 7% GMP revaluation - kerching!zagfles said:Don't think they publish an RPI table, but you can work it out by compounding the Sept RPI from the relevant years. Cap unlikely to take effect unless you've only got a few years of deferment and inflation rises a lot.

0 -

Thanks zagflieszagfles said:

Indeed. Downside is no indexation in payment on pre 1988 GMP, so when you get to about 120 you might have lost all those increases to inflation...garmeg said:

I deferred in 1993 and have 7% GMP revaluation - kerching!zagfles said:Don't think they publish an RPI table, but you can work it out by compounding the Sept RPI from the relevant years. Cap unlikely to take effect unless you've only got a few years of deferment and inflation rises a lot.

The post 1988 GMP is significantly greater than the pre 1988 GMP as I joined the scheme in January 1988. It has an equalised NRA of 60 too.

The pre 1988 GMP in 1993 was about £50 per annum. The post was about £250 and the non GMP just over £1,000.0 -

Seems all my GMP is post 88 so looks like a waiting period applied before joining.

0

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.5K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards