We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

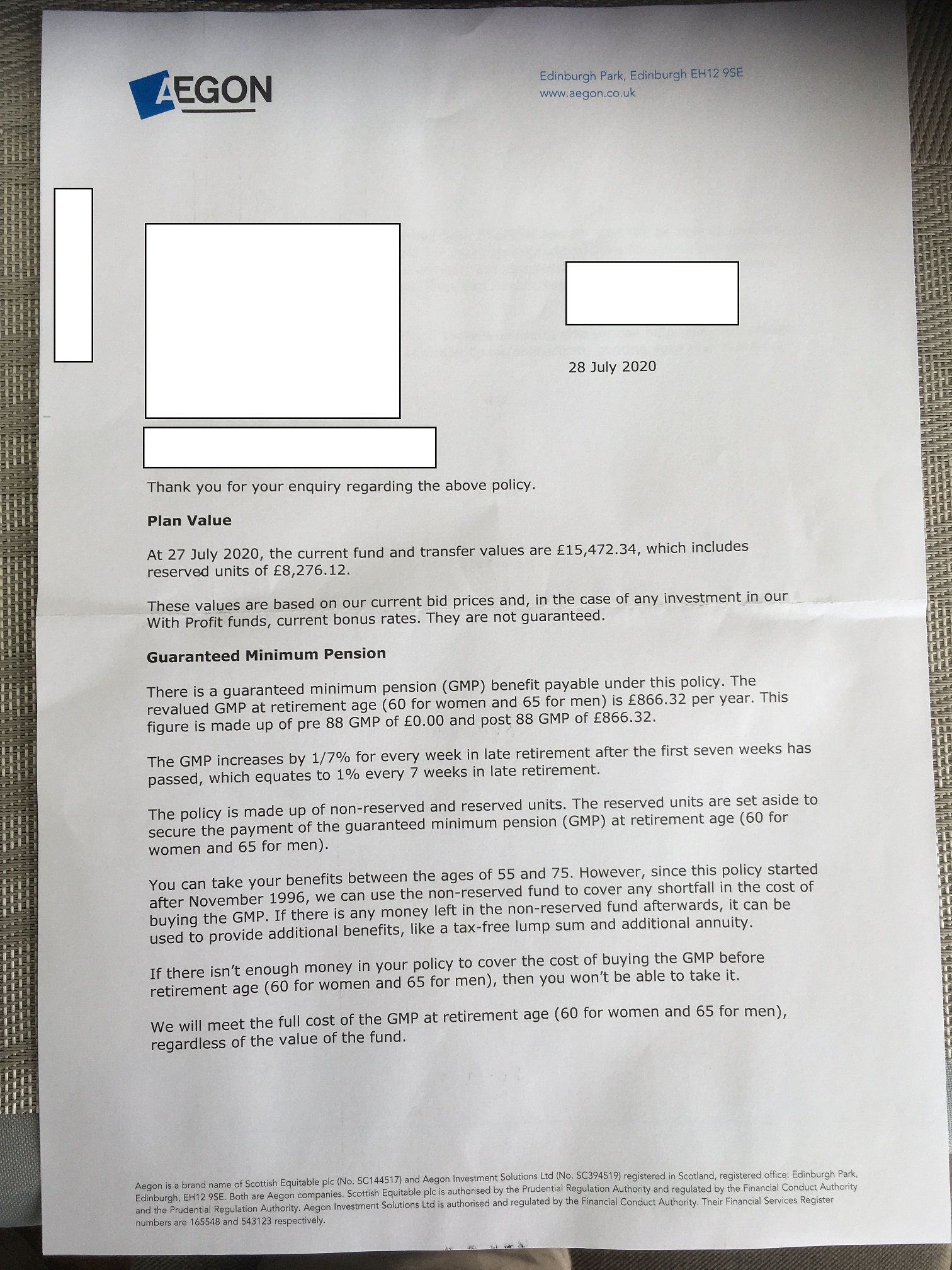

What options have we got with this fund?

I have edited details and attached the letter to this thread.

He is 76 years old, receives state pension and also £270 a month from a works pension. they have no other income.

They live in council property and the £270 a month from his works pension is taken away with rent and council tax payments. If he takes the yearly pension shown on the letter this will also be taken towards rent and council tax.

Could he take the full £15,472.34 as a lump sum? If he can i assume 25% would be taxed free and the remainder taxable.

We can not see the point of having a monthly income because he will not financially benefit from it himself. It also states on letter you can take benefits between the ages of 55 and 75. He is currently 76 years old does that limit his options?

Any advice would be a great help

Comments

-

He is 76 years old, receives state pension and also £270 a month from a works pension. they have no other income.

Does your mother not receive a state pension, even if only on your father's contributions? (Cat B - £80.45 a week). https://www.ageuk.org.uk/globalassets/age-uk/documents/factsheets/fs19_state_pension_fcs.pdf

If not, this needs to be checked.They live in council property and the £270 a month from his works pension is taken away with rent and council tax payments.I don't quite follow - do you mean that he receives his pension but it is swallowed up in rent and CT payments?

Are they in receipt of Pension Credit? If so, the availability of this pension should have been considered. https://www.ageuk.org.uk/globalassets/age-uk/documents/factsheets/fs48_pension_credit_fcs.pdf

With regard to the letter above, it seems that your father has a S32 policy which includes a post 88 GMP.

This pension would have become available to him at the age of 65 - Aegon would have been responsible for index linking the GMP once in payment by up to 3% per annum.

If a GMP is not brought into payment at GMP age, the statutory late retirement increase applies-the letter refers.

Is Aegon aware of your father's age?

There appears to be no indication of what options would be available to your father if he chose to bring the pension into payment - there will be the GMP but is there any excess over GMP? Any option of a lump sum?

A cash equivalent transfer value is given - this would be the value if the pension were transferred out to another arrangement. The GMP is a safeguarded benefit but as the CETV is under £30,000, your father would be able to transfer out to another arrangement without advice.

Aegon do not cover the possibility of Trivial Commutation - but see https://www.pensionsadvisoryservice.org.uk/content/publications-files/uploads/Taking_small_pensions_Detailed_SPOT008_V1.5.pdf

under "core eligibility".

If your parents are in receipt of means tested benefits, the value of this pension will be taken into account.

1 -

Thank you for the detailed response. Mother does receive the cat B pension £80.45 sorry i never mentioned it. They did qualify for pension credit at the start of there retirement but no longer do.

I will have to speak Aegon regarding whether they know my fathers age. We have only recently started receiving the letters. So they may not or it may be because he went over 75 in March that triggered the mail.

Regarding the works pension he receives. Yes it is swallowed up in rent and council tax payments. If the pension increases so do his payments against rent and council tax.1 -

Would it make sense to transfer the value out. Not draw on the pension. Then leave the money in a new arrangement to transfer to his wife or two son's on death?0

-

Would it make sense to transfer the value out. Not draw on the pension. Then leave the money in a new arrangement to transfer to his wife or two son's on death?

I think that the OP's parents are receiving housing benefit and council tax reduction on the grounds of their modest income.

According to https://www.gov.uk/government/publications/pension-freedoms-and-dwp-benefits/pension-freedoms-and-dwp-benefits

There are rules about how your pension, and any money you take from it, will be treated in the calculation of your entitlement to the following income-related benefits:

Housing Benefit

If you (or your partner) are over the qualifying age for Pension Credit

Once you (or your partner) reach the qualifying age for Pension Credit, you are expected to use your pension or pensions to help support yourself.

The particular pension to which the OP's question relates is a S32 with GMP - I suspect it should have been declared once the OP/s father reached age 65.

As far as I can see, if the OP's father does not access the pension, this could be relevant

"an amount of ‘notional’ income will be taken into account when your benefit is worked out. ‘Notional’ income (in this case) is an amount equivalent to the income you would have received if you had bought an annuity.

If you take an income from your pension pot, the amount which will be taken into account when assessing your benefit will be the higher of the actual income or notional income. If you take a cash lump sum, this will be taken into account as capital."

The OP might wish to check out the situation on his father's behalf?

1 -

This looks like a standard letter sent to policyholders up to age 75 and may not fully reflect the terms of his particular policy. Before doing anything else, I think you need to find out from Aegon what his options are given he is 76 - and then take a decision.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0

-

I think the tax free cash option is lost after age 75?0

-

My father did not even know about this pension until this year. OK well he probably did but may have been early in his working life and forgot about. I think the first letter from Aegon was after his 76th birthday in March. Obviously on his retirement at 65 his other works pension was drawn due to contact from the pension company telling him he had a pension to draw.0

-

That won't alter his options - as already pointed out, you need to check what these are.matthew68 said:My father did not even know about this pension until this year. OK well he probably did but may have been early in his working life and forgot about. I think the first letter from Aegon was after his 76th birthday in March. Obviously on his retirement at 65 his other works pension was drawn due to contact from the pension company telling him he had a pension to draw.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0 -

Thank you for the help. I will find his options and post back1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards