We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Could the Govt allow DC pot holders to buy public sector pensions to reduce the deficit?

Comments

-

Why assuming a 5% employer contribution? I left public sector to private sector with a DB scheme, as did many others..michaels said:Well your public sector pension was worth another 60% or more on top of your salary so you would have had to leave your 40k govt job and get more than 60k in the private sector (assuming 5% employer pension contribution) to actually be getting the same remuneration.......Gettin' There, Wherever There is......

I have a dodgy "i" key, so ignore spelling errors due to "i" issues, ...I blame Apple 1

1 -

michaels said:Well your public sector pension was worth another 60% or more on top of your salary so you would have had to leave your 40k govt job and get more than 60k in the private sector (assuming 5% employer pension contribution) to actually be getting the same remuneration.

Thats not difficult to achieve in my experience. In my line of work private sector easily earns twice or more what an equivalent public sector worker would earn.1 -

Only reason for choice is 5% is minimumGunJack said:

Why assuming a 5% employer contribution? I left public sector to private sector with a DB scheme, as did many others..michaels said:Well your public sector pension was worth another 60% or more on top of your salary so you would have had to leave your 40k govt job and get more than 60k in the private sector (assuming 5% employer pension contribution) to actually be getting the same remuneration.

I think....0 -

You are missing the employer contribution, which is considerable ( 30% sort of ballpark but depends on age in some way I don't know).michaels said:So suppose a govt employee on 50k pays 12.5% for 1/80th final salary pension available at 67. Now assume they could buy as much pension as they want so 2% of salary would buy then 2/80ths etc - then 50k would buy then 8/80ths or 5k pa of pension (wow this is a good deal!)

But a banker, engaged at enormous expense,Had the whole of their cash in his care.

Lewis Carroll1 -

Thanks - so do we know what actual rate the govt puts on these contributions - even with 50k buying 2k per annum pension it would be worth it for most DC pension pot holders.theoretica said:

You are missing the employer contribution, which is considerable ( 30% sort of ballpark but depends on age in some way I don't know).michaels said:So suppose a govt employee on 50k pays 12.5% for 1/80th final salary pension available at 67. Now assume they could buy as much pension as they want so 2% of salary would buy then 2/80ths etc - then 50k would buy then 8/80ths or 5k pa of pension (wow this is a good deal!)

It has been suggested that you can buy into a gov pension when you join the civil service although no idea what the rate is - does anyone know?

I think....0 -

there will be actuarial calculations specific to which scheme you're joining (there are many variations in public sector schemes), you'd probably have to ask the individual scheme for a quote. Which is how it works in reality, after you take the job.........Gettin' There, Wherever There is......

I have a dodgy "i" key, so ignore spelling errors due to "i" issues, ...I blame Apple1 -

michaels said:There is also another way people can effectively purchase more state pension - by deferral. Perhaps if public sector pension terms are too generous then the offer could be made at the same 'cost' as deferral which I think works out at a return of about 5.8% (is this based on average longevity?) DC pension holders could be given the option to either 'defer forward' and/or purchase extra state pension on the same terms as deferral.State Pension is increased by about 5.8 percentage points for each year deferred (not compounded). However, that is not really the rate of return, as the initial capital from the period of deferral is lost.For rates of return, the more obvious rate is the SCAPE discount rate used to value public service pension schemes, currently set at CPI+2.4%. Alternatively gilt yields could be used, although as gilt yields would produce very similar figures to commercial annuity rates that may not make much sense.michaels said:Well your public sector pension was worth another 60% or more on top of your salary so you would have had to leave your 40k govt job and get more than 60k in the private sector (assuming 5% employer pension contribution) to actually be getting the same remuneration.I think 60% is rather over the top. For example, new pension accrual in the Civil Service scheme is calculated to cost 24.9% of pensionable pay by the Scheme Actuary using the SCAPE discount rate (CPI+2.4%), or 47.4% using a standard IAS19 rate (using the yield on high-quality (AA) rated corporate bonds). Of these costs, members pay 5.6 percentage points.Thanks - so do we know what actual rate the govt puts on these contributions - even with 50k buying 2k per annum pension it would be worth it for most DC pension pot holders.

It has been suggested that you can buy into a gov pension when you join the civil service although no idea what the rate is - does anyone know?The rate is heavily dependent on age - have a play with the Civil Service alpha Added Pension calculator to get an idea of the cost of Added Pension.£50,000 would purchase £2,760 of CPI linked pension for a male aged 65, with dependent receiving 37.5% of the pension upon death, payable from age 66. Without survivor cover it would purchase a pension of £2,9402 -

I doubt it would - I shoved some numbers into an online annuity calculator and it said 50k would probably give an annuity of 2.3k if bought at 65.michaels said:Thanks - so do we know what actual rate the govt puts on these contributions - even with 50k buying 2k per annum pension it would be worth it for most DC pension pot holders.

But a banker, engaged at enormous expense,Had the whole of their cash in his care.

Lewis Carroll0 -

That would be a level annuity. An index linked annuity would be half that.theoretica said:

I doubt it would - I shoved some numbers into an online annuity calculator and it said 50k would probably give an annuity of 2.3k if bought at 65.michaels said:Thanks - so do we know what actual rate the govt puts on these contributions - even with 50k buying 2k per annum pension it would be worth it for most DC pension pot holders.

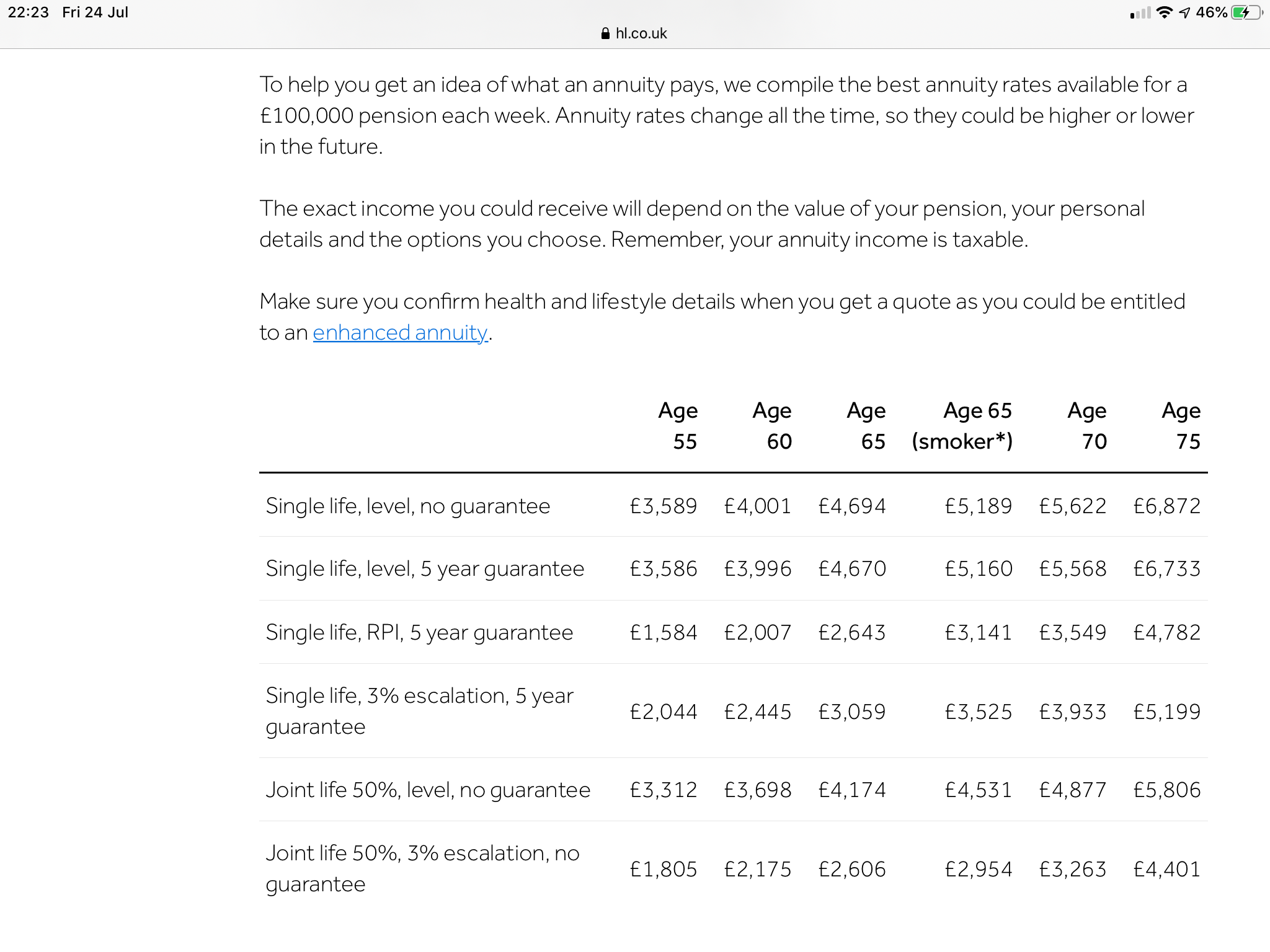

Sample rates for £100,000 purchase money courtesy of Hargreaves Lansdown

https://www.hl.co.uk/retirement/annuities/best-buy-rates 2

2 -

So I went on an annuity calculator and said if someone aged 66 lived of 9k savings for a year and deferred their state pension for that year they would increase their state pension thereafter by 5.8% or about 500 quid whereas if they spent the 9k savings on an annuity (LPI indexed) they would only get about £230pa - ie the return on deferring is more than twice the cost of the lost year's pension.hugheskevi said:michaels said:There is also another way people can effectively purchase more state pension - by deferral. Perhaps if public sector pension terms are too generous then the offer could be made at the same 'cost' as deferral which I think works out at a return of about 5.8% (is this based on average longevity?) DC pension holders could be given the option to either 'defer forward' and/or purchase extra state pension on the same terms as deferral.State Pension is increased by about 5.8 percentage points for each year deferred (not compounded). However, that is not really the rate of return, as the initial capital from the period of deferral is lost.For rates of return, the more obvious rate is the SCAPE discount rate used to value public service pension schemes, currently set at CPI+2.4%. Alternatively gilt yields could be used, although as gilt yields would produce very similar figures to commercial annuity rates that may not make much sense.michaels said:Well your public sector pension was worth another 60% or more on top of your salary so you would have had to leave your 40k govt job and get more than 60k in the private sector (assuming 5% employer pension contribution) to actually be getting the same remuneration.I think 60% is rather over the top. For example, new pension accrual in the Civil Service scheme is calculated to cost 24.9% of pensionable pay by the Scheme Actuary using the SCAPE discount rate (CPI+2.4%), or 47.4% using a standard IAS19 rate (using the yield on high-quality (AA) rated corporate bonds). Of these costs, members pay 5.6 percentage points.Thanks - so do we know what actual rate the govt puts on these contributions - even with 50k buying 2k per annum pension it would be worth it for most DC pension pot holders.

It has been suggested that you can buy into a gov pension when you join the civil service although no idea what the rate is - does anyone know?The rate is heavily dependent on age - have a play with the Civil Service alpha Added Pension calculator to get an idea of the cost of Added Pension.£50,000 would purchase £2,760 of CPI linked pension for a male aged 65, with dependent receiving 37.5% of the pension upon death, payable from age 66. Without survivor cover it would purchase a pension of £2,940

Same point applies to your next point re bond yields, we are not talking an expected return we are talking a guaranteed return so the correct comparator is the cost of an annuity.

And if I could get an index lined Annity paying 5.4% at 66 I would have enough money to retire now")

I think....0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards