We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Overpaying mortgage now or later

Comments

-

1) He only has a 3 year fixed, especially in this time, I'd do all I could to pay as much as possible off of the principle sum. You have no idea what the interest is going to look like in 3 years, but it's on its way up.

2) Even if you're relatively lazy, you can get 1.25% interest right now. That's almost his mortgage interest, but he won't be able to push it beyond his mortgage interest on the total sum through savings accounts. On his £14K that's an additional £175. If it was me, I'd get more out of it.

3) When he reaches the end of that 3 years, with the 14K overpayment and let's say he adds another 5K overpayment over the remaining 2 years. Assuming he's on 90% LTV, with the overpayments, he'll be at 81% LTV when he has to remortgage.

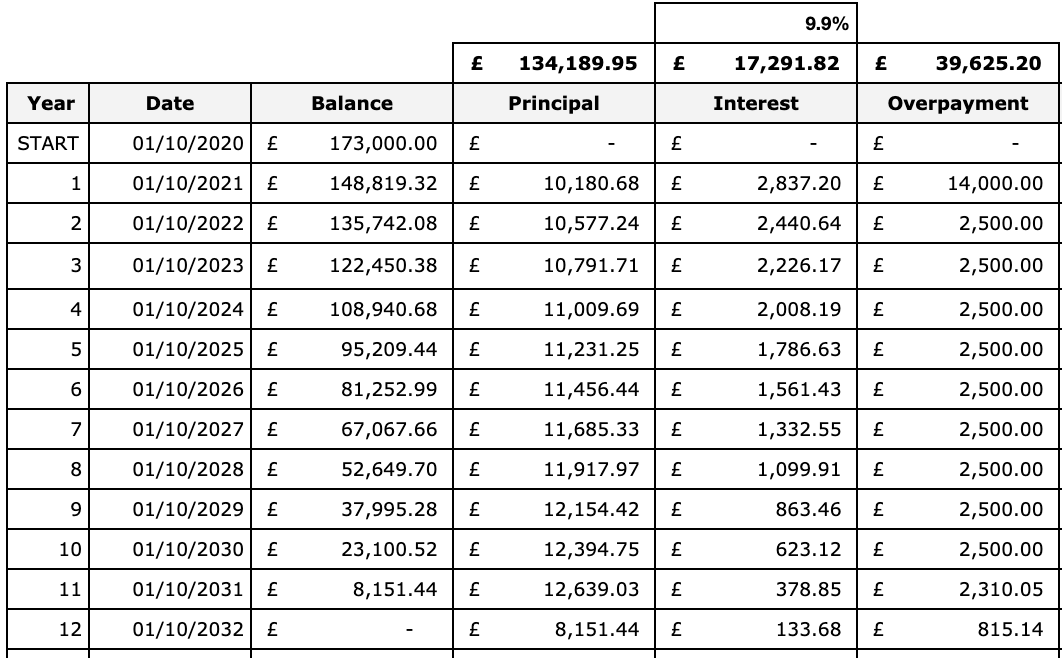

4) For simplicity I'll assume you can get 1.64% for the rest of his mortgage term, let's also assume you pay that 14K toward principle amount and every year overpay by 2.5K or max 10%, you'll save £6,449.37 in interest and finish your mortgage in 12 years.

If you think it's worth it, do it, if not don't. Personally I'd overpay to the max of my ability (assuming I have a buffer/safety net/security). One thing that doesn't make 'financial sense' though, is wasting it on things you don't need.") 0

0 -

1) If by "in this time" you mean potential wave of job losses thats a reason not to overpay surely?

2) with a combination of regular savers and easy access you can actually get very close to 1.64

3) Irrelevant to argument as to whether to overpay now or later

4) You seem to have assumed here money earmarked for overpayment is sitting in 0% account.0 -

1) Risk and mortgage interest are on their way up, not down. It won't matter if BoE even sets negative rates. w.r.t losing jobs, that's why I said assuming you have a buffer/etc. Obvious if you don't have anything to fall back on, keep it and don't overpay.grumiofoundation said:1) If by "in this time" you mean potential wave of job losses thats a reason not to overpay surely?

2) with a combination of regular savers and easy access you can actually get very close to 1.64

3) Irrelevant to argument as to whether to overpay now or later

4) You seem to have assumed here money earmarked for overpayment is sitting in 0% account.

2) Fair enough

3) Not really, because by overpaying he'll get a better LTV when he remortgages. His question was whether it makes sense to overpay and there are multiple aspects to that, including your remortgage later down the line. Furthermore, the assumption is that we're headed for a drop in value. In 3 years it's well within the realm of possibilities that he ends up with a house he can no longer afford.

4) I don't. That's why I said save your money until the end of the mortgage year, read my initial post. He can save it longer, but that has risks of its own (see point 3).0 -

Never overpay, with the present climate due to Covid, put £7,000 into savings so you could pay the mortgage. You get no benefit ever for overpaying should you need a break!

The other £7,000 put into your pension. The Government will give £1,400 for doing so. Over 15 years this could grow, at a low rate of 2% to about £11,300, more than beating the extra £3,666 interest you pay and you still have that other £7,000!0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards