We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

How much of my portfolio should be in cash during retirement?

Comments

-

I have just over 2 years' cash in SIPPs, because that's how long our fixed rate mortgage has to run, and I want to be sure of meeting the repayments, if anything untoward happens. After that time, the likely withdrawal requirement will drop by 50%, so as time goes on, I will be reducing the cash level by half by adding to existing investments (if it hasn't been removed for other purposes).

2 -

I think it's important to understand where your cash buffer is being allocated from. So for example if you are holding 10% cash, and this would otherwise be allocated to equities, this may not give the outcome you desire.tacpot12 said:

My view is that you need 30 months of cash available; 24 months is how long the typical stock market crash takes to pass and for the stockmarket to get back to where it should have been, and a further six months because you don't want to be running on fumes.

https://finalytiq.co.uk/cash-reserve-buffers-withdrawal-rates-old-wives-fables-retirement-portfolio/

3 -

I am not yet in DD but see it differently. Whilst shares are high (as evidenced by low yields) I would be drawing from shares funds and retaining the cash and would draw against the cash when stocks were low (shown by higher yields).Joey_Soap said:I recommend 2 to 3 years income. So, like now if your income from stocks drops by 40% or so, you can ride through maybe 6 years at a pinch without selling family silver to live. Just draw down on the cash. Hopefully replenish it when times get better.

Is there any data historically on how much cash has cost - ie how much the best savings accounts (probably instant access or up to 12m fix) have fallen behind inflation by?

I think....1 -

Because Its his only holding which is guaranteed not to go down by 50%. And the loss of value over 3 to 5 years is nothing if your cash is in an interest bearing account. And at times of real distress (deflation) cash appreciates in terms of real valueMoe_The_Bartender said:I hold a years income in cash. It’s the only holding that’s absolutely guaranteed to lose value so why hold more than you really need?2 -

In my opinion, the answer depends on the size of your portfolio, your age and other personal circumstances.For example, if your portfolio is large (lets say 5M GBP) then the cash buffer isn’t as important. You won’t starve even if the market crashes and stays down for a number of years.If you are older... Lets say 80 years or so then I would put a decent chunk of your portfolio into an annuity. There is larger behavioural risk when we try to manage stock and bond portfolios in old age. If you have an annuity then cash does not matter except for a few months buffer for ongoing expenses.

In other cases something like 3 years’ worth of expenses makes sense to me.1 -

This link shows building society rates over many years.michaels said:

I am not yet in DD but see it differently. Whilst shares are high (as evidenced by low yields) I would be drawing from shares funds and retaining the cash and would draw against the cash when stocks were low (shown by higher yields).Joey_Soap said:I recommend 2 to 3 years income. So, like now if your income from stocks drops by 40% or so, you can ride through maybe 6 years at a pinch without selling family silver to live. Just draw down on the cash. Hopefully replenish it when times get better.

Is there any data historically on how much cash has cost - ie how much the best savings accounts (probably instant access or up to 12m fix) have fallen behind inflation by?

http://www.swanlowpark.co.uk/savings-interest-annual

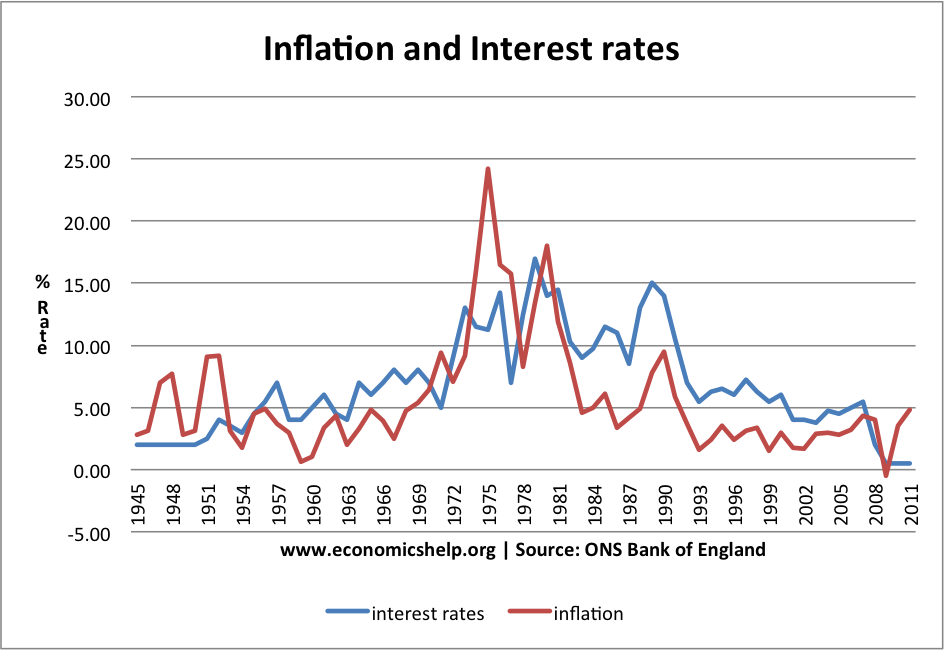

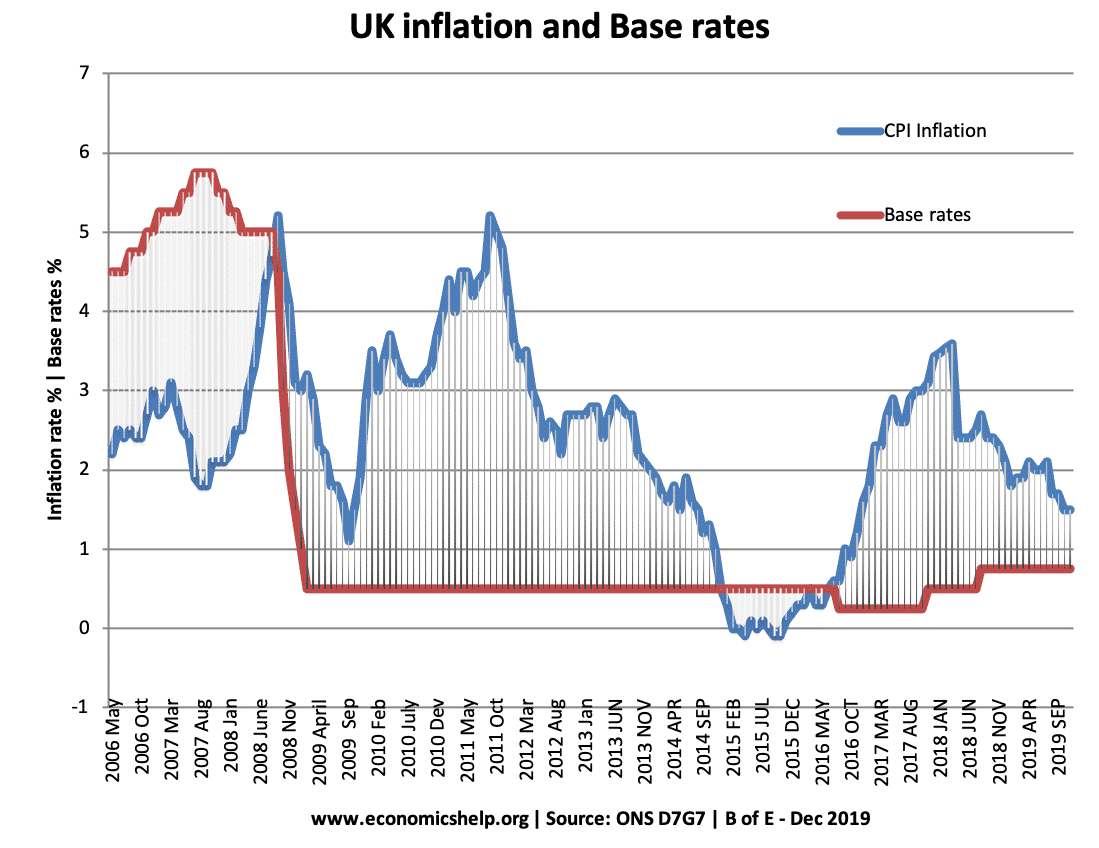

In general bank rates have held up versus inflation until the 2008 crash. Many building societies had savers rates above base rates.

https://www.economicshelp.org/wp-content/uploads/2012/01/inflation-interest-rates-1945-2011.png

https://www.economicshelp.org/wp-content/uploads/2017/10/inflation-interest-rates-06-19.png

I've always had a mix of cash in fixed rate bonds and shares. At the end of the day it's your savings and not some journalists or commentators telling you how much cash you should have in the background. If this latest crisis had turned a lot worse those with just 6 months cash could well have been worried.? Falling markets and little cash ?.I wouldn't want that at all.

Whoever inherits whats left of your savings is sure to blow a fair bit. That new car will be worth ten grand less as soon as its off the forecourt. Never mind the fitted kitchen and holidays.

3 -

So thinking at the portfolio level, holding cash does two things:

1) reduces volatility at the expense of growth

2) at the margin forms part of an active management strategy where investment is tilted towards equities when yields are high and away from equities when they are low

Number one sounds like it might be a rational trade off. Number two sounds like you just need a clear rebalancing strategy rather than tinkering at the edges with where you withdraw from.

Are there funds that pursue a 'value based strategy' that adjusts the weighting of equities vs money market based on some metric such as CAPE? Ideally something that just applies a set of rules with minimal charges rather than fund managers using their discretion (to get it wrong half the time) and charging through the nose for doing so?

I think....1 -

Thanks for the replies so far, and for the links - looking at those, it does seem that there is a case for some approaches that I hadn't considered. I guess I'm looking for a sensible middle ground that won't cause me any nightmares, and which I can manage with my relatively limited knowledge.

0 -

The current yield on the SP500 is just under 2%. A world tracker is similar.

https://www.multpl.com/s-p-500-dividend-yield

https://www.hl.co.uk/shares/shares-search-results/v/vanguard-funds-ftse-all-world-etf-usdgbp

I'm not saying this is the answer but an option. 5 years before retirement you could start holding the dividend payments as cash in your pot. That should give a base for an initial 3% withdrawal rate and see how it goes. If you have other savings in a bank account then even better.

There's always questions about inflation and dividends. Research shows it's not all that bad.

https://seekingalpha.com/article/439171-has-dividend-growth-kept-up-with-inflation

This is a decent website for past events.

https://www.yardeni.com/pub/buybackdiv.pdf

1 -

If you had accumulated £5 million, you could have a very comfortable retirement whether you left it all invested or kept a sizeable percentage in cash. It would be nice to have these options.Deleted_User said:In my opinion, the answer depends on the size of your portfolio, your age and other personal circumstances.For example, if your portfolio is large (lets say 5M GBP) then the cash buffer isn’t as important. You won’t starve even if the market crashes and stays down for a number of years.

1

{kind=link}

{kind=link}

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards