Emergency fund £8,500/£8,500

Mortgage overpayment £260

Debtfree!

£21,228.07 paid off in 22 months

We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

How do i finally face my debts?

Alicekimbo

Posts: 9 Forumite

I have approx £12k debt spread across various credit cardS and lenders. I was due to start a repayment plan with Stepchange at the end of March however i paused it because the rapid unknown of Corona Virus at the time.

i have buried my head and ignored my debts for the last few months, some have been passed to collection agencies, and the reality is i cant afford £400 a month purely on debts when i have mortgage and other bills to pay. I have just been offered and IVA plan by ‘Financial Support Systems’. Are they a con? Are they going to sting me with fees? I really don’t know what the best course of action is.

i have buried my head and ignored my debts for the last few months, some have been passed to collection agencies, and the reality is i cant afford £400 a month purely on debts when i have mortgage and other bills to pay. I have just been offered and IVA plan by ‘Financial Support Systems’. Are they a con? Are they going to sting me with fees? I really don’t know what the best course of action is.

2

Comments

-

It’s highly unlikely that Financial Support Systems are offering you a solution that is better than that by Stepchange (a debt charity, not a money making business - think about it). And an IVA may not be the best solution for your level of debt, more information is necessary.

Put your SOA on here (if you can’t find it on the site someone will link it) and by tomorrow afternoon you’ll have some really constructive advice. No one can give you any direction without the information in your SOA4 -

The link for a SOA

https://www.lemonfool.co.uk/financecalculators/soa.php

As above they are not a charity so will charge fees. Stepchange could be a better option. Post a bit more information and I am sure others can offer you some advice.

2 -

Only one way to face them I'm afraid, and that's head on. The good news is you have the knowledgable people on this forum who will help, and believe me, they give brilliant advice. Post the SOA as suggested and although it might feel as though you're being judged on past spending, please, please try to remember that all advice given is given with the intention of helping you get through this as painlessly as possible. Good luck!1

-

Alicekimbo said:I have approx £12k debt spread across various credit cardS and lenders. I have just been offered and IVA plan by ‘Financial Support Systems’. Are they a con? Are they going to sting me with fees? I really don’t know what the best course of action is.Hi,Ok, some clarity here for you, the debt industry is similar to any other industry, there are the right places to go for advice, and there are the wrong ones, most debt solutions are whats known as "regulated" that means the terms and fee`s on that arrangement are set by Government, this applies to Bankrupcy and DRO, an IVA however has no set fee structure, so an Insolvency Practitionaire can charge you what they like really, and it must be administered by an IP, as that is a legal requirement.Anyone can set up as a Debt management company, and to sell IVA`s, all you need is a solicitor, and an Insolvency practitionaire.Now because the fee structure is fluid, these companies can make a lot of money by selling IVA`s to all and sundrey, even through it may, or may not be the right solution for you.As a general rule, IVA`s are only suitable if -(a) You are a homeowner(b) You have debt in excess of 30k(c) You have sufficiant disposable income to make payments with.Also remember in year 5 of an IVA, you will be asked to try and re-mortgage (if your house has equity) if thats not possible, or you have no equity, then another year of payments is the norm, there is also a new recent clause where they offer you a loan to complete the IVA early, usually at stupid rates of interest, best avoided to be honest.From what you have written, an IVA is not suitable in your circumstances, as you have far too little debt, an informal debt management plan, set up by one of the free debt charities in my signiture will probebley suit your needs better.An IVA does have its place, and is suitable for some people, the debt charities will tell you the best solution for you, based on your circumstances, not on the size of your wallet, they are mis-sold on an alarmingly large scale, to people just like you, who are non the wiser when it comes to debt solutions, and accepts what the first place that comes up on Google tells them, and that is not a critisism of you, remember these people are out to sell you an IVA, thats all they do, they are not debt advisors, i am a debt advisor, as is Fatbelly, they are sales people, nothing more.Post up the SOA, and well have a look see.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter4

-

You can manage your debts yourself. You don't have to use a third party company. I did it myself, just telephoned them all and agreed on an affordable monthly amount. The good thing about doing it yourself is flexibility. I found it easier and quicker to just call them and up or reduce my payments rather than going via a third party which takes time. Once you have paid some off you can also offer to settle for a reduced sum. My only tip is be realistic. Don't offer all your spare money for debts. Unexpected things will happen and you need a little bit of spending money too. If you offer all you have and then 'break the agreement ' then creditors can become less inclined to want to work with you. Do a written budget so you truly know what your situation is and importantly to prevent getting back in debt.2

-

Thanks for the advice and yes i dont have a clue what is right and what is wrong for me. I’m looking for impartial advice. I did have a plan set up with StepChange but couldn’t realistically afford £400 a month repayments out of a £1300 salary. The IVA company told me even on a debt plan accounts will still default and creditors can still sell my debt on etc.

The only reason i’m unsure about phoning each of them is that a couple of accounts have already defaulted.... and my guess is they will not be willing to help?0 -

My personal debt is £12k

My personal debt is £12k

my partners personal debt is £2m

0 -

I chopped off incomes

my income- £1350 per month

partners income-£1650 per month0 -

I must also add that i refer to these debts as ‘old’ debts. Started opening credit cards in my early twenties at A time when my monthly salary was £900-£1000. I would pay my bills with my salary and go mad with credit cards. Now in my early thirties and current salary i no longer have the reliance and have learned alot about my relationship with money and how if effects me mentally. I grew up in an environment where if you wanted something you stuck in on the credit card. It was the norm. My mum took me to the bank at 18 to get my first credit card. Not blaming her in anyway but that was me then and this is me now and i want to fix and finally have freedom.0

-

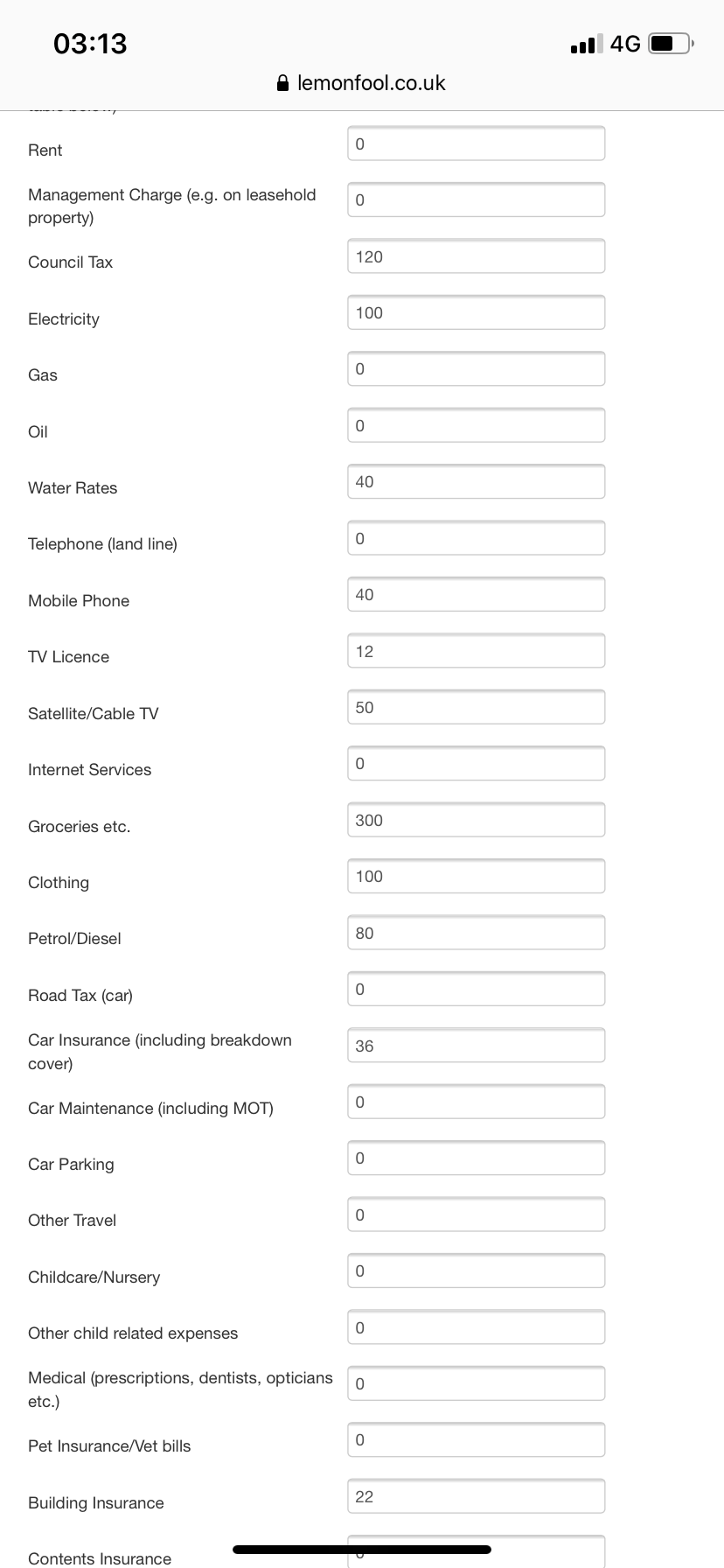

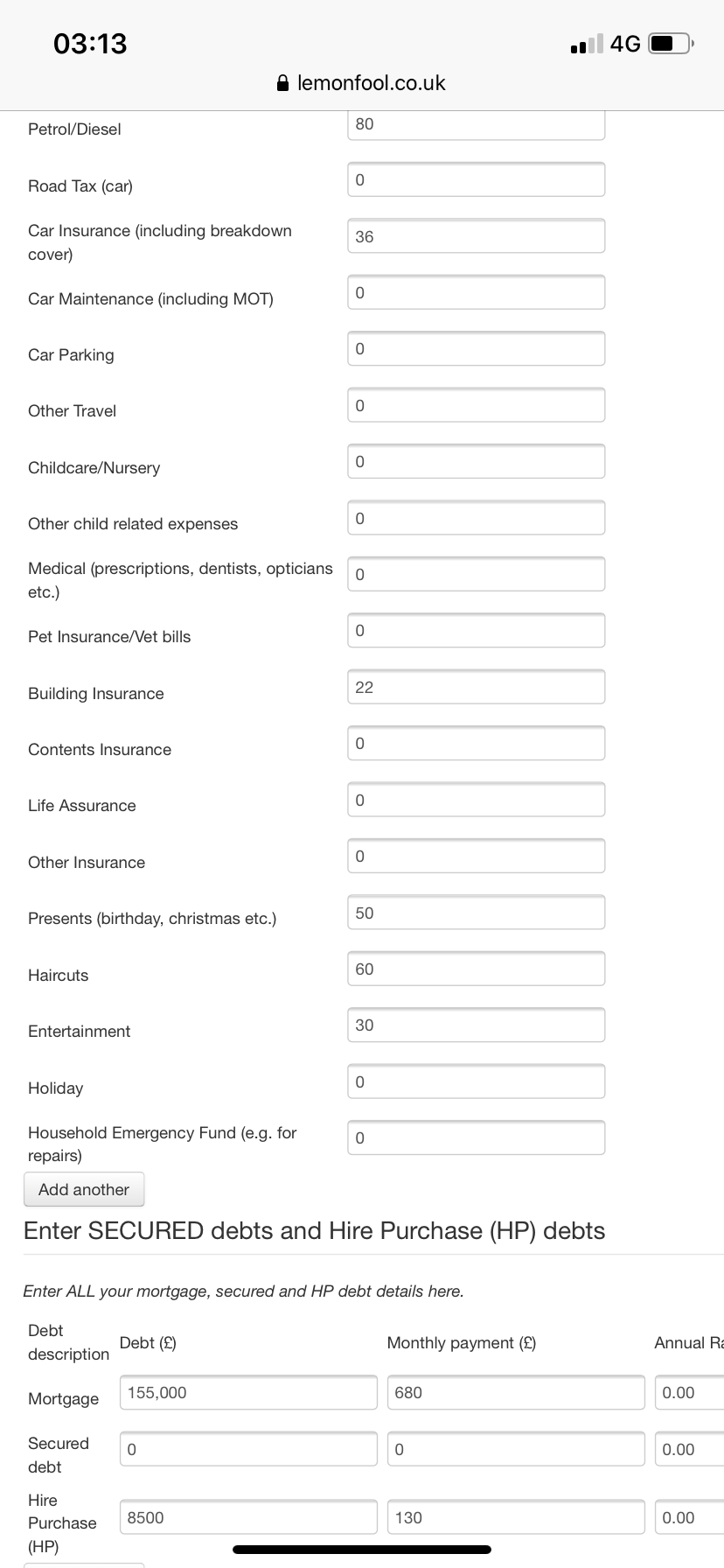

I think something has gone wrong with posting your soa, some parts are doubled up and some parts are missing, like the list of debts with interest rates, and totals of things. Can you have another go at posting it so we can get the whole picture?

At the moment your soa looks aspirational, which is fine as long as you know where your money has been going and you know how to make that stop. Your mobiles could be cheaper (sim only), you could lose £100 from your food budget (easy if there are only 2 of you) and you're missing contents insurance and a payment to an emergency fund, all very important. £60 for haircuts is too much, can you get a cheaper hairdresser? Or fewer cuts?

Does your employer pay for your car? You have petrol costs and insurance but no MOT costs or road tax. This needs fixed.

Your mortgage to income ratio is good. Once you've fixed your budget, it's likely your expenses won't come to much more than £1.5k p/m on a £3k p/m income. That's quite a healthy suplus. Can you think of anything else your'e missing out?

Without info about the debt it's hard to work out what's happened here. Have another go at your budget and let us know. With the info you've given so far, your position looks fine for you to start dealing with this.

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.6K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.7K Work, Benefits & Business

- 603.1K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards