We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Should I scrap MA & go direct?

jamesm5094

Posts: 45 Forumite

I applied in May through mortgage broker to HSBC and beginning of June the mortgage product got pulled and they declined us because there was confusion over if my partner self employed had ceased trading so they was only going by my employed salary. My MA has said we got to wait for a product to become available and then he will submit it and appeal the declined decision to get it overturned.

I have spoken with HSBC direct and they have a 10% deposit deal at 1.89% which they have said I can get.

So should I go direct and put in a 2nd application with HSBC? Or will it just flag up that I have a application already submitted and have been declined??

0

Comments

-

What's changed with regards to your partner?jamesm5094 said:I have spoken with HSBC direct and they have a 10% deposit deal at 1.89% which they have said I can get.0 -

@jamesm5094 If you are aiming for the 90% HSBC option, then you are likely to have better luck going direct than through a broker as HSBC is severely throttling broker applications so they struggle to place applications on behalf of their client. They have to get in an online queue at 8 in the morning until a quota is filled, etc. At least that's what my broker told me a couple of weeks ago.However, more importantly you need to be clear on the reason for the initial decline and make sure that there isn't a fundamental issue that makes you ineligible for the HSBC product.Assuming you provided all the information asked, it doesn't reflect well on your broker that the app got declined and that he/she is now telling you that the 90% product is "pulled" while leaving you hanging. Also, there's now an extra hard check on your recent credit history.If you do choose to go direct, do make sure you let them know about the recent decline at the outset.0

-

I supplied all documents required for myself as well as for my self employed partner. My MA then sent me some questions HSBC was asking and one was had my partners business ceased trading due to coronavirus. I was thinking in the context of has the business stopped because of coronavirus but will start up again when possible so I said yes. He then told HSBC that and they think my partners business has shut down for good so they only went on my pay and I can’t lend enough on my own so they declined it. So it was a miss communication error.I have told my mortgage broker that I have spoken with HSBC and they have said what product I can get and they have done a DIP saying I can borrow enough. My mortgage broker has said to me that HSBC have told me I can borrow enough but when it gets further into the application they will decline it as I have already been declined by them once.My selling and purchasing chain are all completely ready to exchange now and I’m the only one holding them up because I haven’t got my mortgage offer. I don’t know what to do.1

-

@jamesm5094 I

I'll be honest, it's a tricky one. If the underwriters looked at what you've said and provided, and then decided that (in their opinion) the business isn't operational, a second direct application is going to give the same result. A DIP would not show that.

Their judgement as to the viability of the business is necessarily going to be more conservative than your partner's. I highly doubt it's a simple miscommunication error.

But if HSBC is literally the only 90% lender you are eligible for, then I guess there's no harm in going direct. Worst case scenario they decline again and you are no worse off than now (unless there's an application fee).

0 -

My mortgage broker has told me he has wrote emails and letters to appeal it but has got to wait for a mortgage product to become available for him to re-submit it. As I’m only putting 10% deposit down then who knows when a product will become available through him.This is why I’m debating going straight direct to HSBC as I know the product is there and if it all went through ok then it could be done a lot quicker.Plus if I stick with broker then if it did take weeks till a product become available I don’t know if the other people in the chain will wait that long.....0

-

That's ridiculous. Why did your broker pass on the information that your partner's business had closed for good, without asking you for clarification first?? The broker should have known that this would have resulted in a declined application and should have at least consulted you on this. I can't fathom why he/she just passed the message along without discussing the implications or double-checking what you meant. Bizarre."If you cannot do great things, do small things in a great way" - Napolean Hill0

-

Not all mortgage brokers are created equal. Ultimately we ended up binning our broker when she made some critical mistakes in our application and then advised us to go with a more expensive product because she 'didn't like the fees' on the cheaper deal (despite the overall cost over the fix being lower).

It was quite stressful doing the application on our own, and Nationwide were painful to deal with (computer fault on first application, mistake made in subsequent application, then repeated failure to contact us when they needed more information; they just left us waiting to contact them to find out what they were waiting for so we had to phone every day to make sure it actually went through). However, we were able to get the best product for our situation on our own.0 -

@jamesm5094

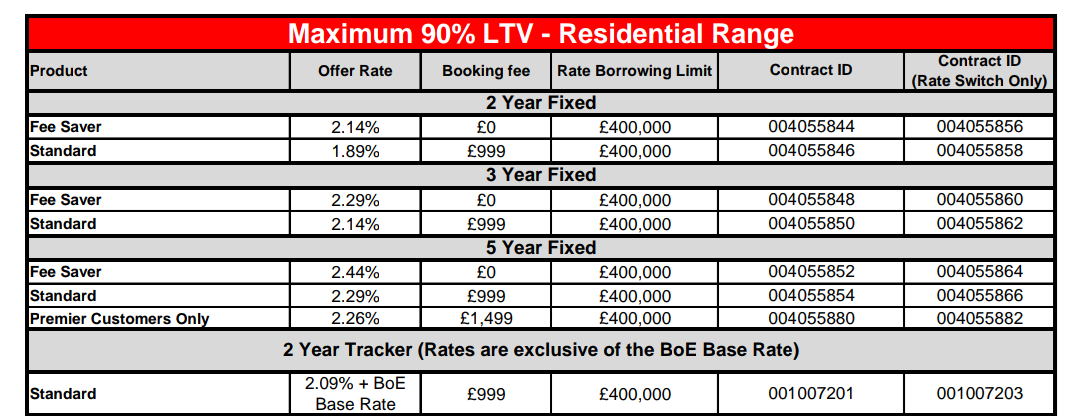

Your broker is not being straight with you. There ARE 90% HSBC products available for brokers, it's just that (currently) it's much harder for brokers to make a submission as compared to applying direct. That's not his fault, but he should be upfront about it.

Here is the latest list of 90% intermediary products as on the HSBC intermediary website.

0 -

God knows why he has done that, stupid of him really if he knew it would just get declined. It’s just a complete balls up of the whole thing and we’re left stuck in a situation.DaMoon said:That's ridiculous. Why did your broker pass on the information that your partner's business had closed for good, without asking you for clarification first?? The broker should have known that this would have resulted in a declined application and should have at least consulted you on this. I can't fathom why he/she just passed the message along without discussing the implications or double-checking what you meant. Bizarre.0 -

See I didn’t think he was being straight with us. He has also told us that we need to wait until HSBC will take into account my overtime as we can’t borrow enough but when I did a DIP directly with HSBC they have said we can borrow enough without my overtime.jamielutz1987 said:@jamesm5094

Your broker is not being straight with you. There ARE 90% HSBC products available for brokers, it's just that (currently) it's much harder for brokers to make a submission as compared to applying direct. That's not his fault, but he should be upfront about it.

Here is the latest list of 90% intermediary products as on the HSBC intermediary website.It’s all just confusing, the original application my broker had made a valuation and everything had been done so if I now go directly to HSBC they are going to have to carry out another one.I just don’t want to go direct if it’s going to make the situation worse and it’s just going to put more bad marks against my name.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.7K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.7K Work, Benefits & Business

- 603.2K Mortgages, Homes & Bills

- 178.2K Life & Family

- 260.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards