We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Trying to understand my offset mortgage

pandaman888

Posts: 9 Forumite

Hi, I'm hoping to get a better understanding of offset mortgages, so any advice is appreciated...

My situation is I currently have an Coventry BS offset mortgage of £175k with 21 years remaining, my fixed term deal has lapsed and I'm on the variable rate of 4.49%. The rate hasnt bothered me as such as I've had £175k in savings that cover the mortgage amount so in essence the way I have understood is I have just been making interest free repayments. I have also selected my offset benefit as payment reduction as oppose to term reduction as I want to keep my monthly payments low.

The time has come for me to dip into the savings portion and I am looking to take out £30k. The way I understood offset mortgages is that the interest is charged on the portion which isnt covered by the savings account which will be £30k I'm planning to take out. Thus I thought it would be better to renew my fixed term deal with CBS with a fee free product and get a better rate (1.68% in this case) so my £30k attracts less interest.

So I have been speaking to the adviser at CBS and they have advised me that I'm actually worse off going to the new deal as my current offset interest benefit is calculated using 4.49% on the £145k savings pot thus providing a greater benefit that it would at 1.68%. They run some numbers and it works out to be £80 more on the 1.68% rate than on the 4.49% rate. The comparison they made was that I'm better being on the higher rate unless my savings dropped below £120k.

Is that actually right and my understanding of the offset benefit is incorrect? I've been trying to find some calculators to check but not being able to find one that fits my situation.

My situation is I currently have an Coventry BS offset mortgage of £175k with 21 years remaining, my fixed term deal has lapsed and I'm on the variable rate of 4.49%. The rate hasnt bothered me as such as I've had £175k in savings that cover the mortgage amount so in essence the way I have understood is I have just been making interest free repayments. I have also selected my offset benefit as payment reduction as oppose to term reduction as I want to keep my monthly payments low.

The time has come for me to dip into the savings portion and I am looking to take out £30k. The way I understood offset mortgages is that the interest is charged on the portion which isnt covered by the savings account which will be £30k I'm planning to take out. Thus I thought it would be better to renew my fixed term deal with CBS with a fee free product and get a better rate (1.68% in this case) so my £30k attracts less interest.

So I have been speaking to the adviser at CBS and they have advised me that I'm actually worse off going to the new deal as my current offset interest benefit is calculated using 4.49% on the £145k savings pot thus providing a greater benefit that it would at 1.68%. They run some numbers and it works out to be £80 more on the 1.68% rate than on the 4.49% rate. The comparison they made was that I'm better being on the higher rate unless my savings dropped below £120k.

Is that actually right and my understanding of the offset benefit is incorrect? I've been trying to find some calculators to check but not being able to find one that fits my situation.

0

Comments

-

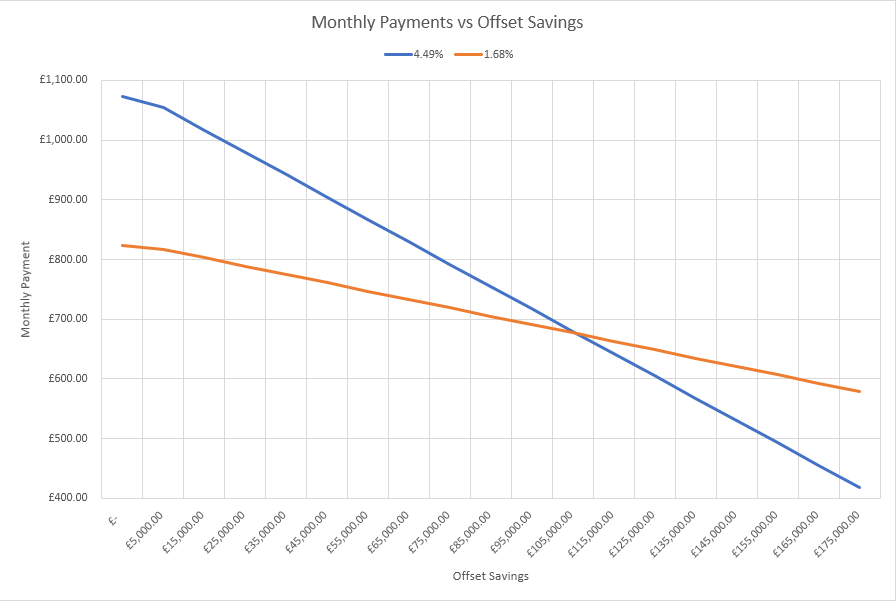

I don't have experience with offset mortgages, so I'm basing the following using simplified mathematical observations for the first month.

A higher rate of interest would result in a larger offset benefit, which means a larger reduction to your monthly payments. This could result in a monthly payment amount lower than what a lower rate of interest could achieve; however, more interest is still charged, so it's still more expensive overall.- Interest Rate: 4.49%

- Minimum Monthly Repayment: £1073

- Monthly Interest: £654.79

- Offset Benefit: £542.54

- Reduced Monthly Repayment: £530.46

- Interest Charged: £112.25

- Capital Repaid: £418.21

- Interest Rate: 1.68%

- Minimum Monthly Repayment: £824

- Monthly Interest: £245.00

- Offset Benefit: £203.00

- Reduced Monthly Repayment: £621.00

- Interest Charged: £42.00

- Capital Repaid: £579.00

1 -

Thanks that makes sense to me. I guess the adviser was just looking at keeping my monthly payments low whereas I’m just wanting to pay the lowest amount of interest.0

-

much apreciate the information given, i am thinking of joining my sons offset morgage , i already get a monthly sum off my investment and reluctant togive it up to him. i am 68 and having to look at, what to do with large amounts of money sat in funds. have a good relationship with my son, but still hard to lose control0

-

Offset mortgages with offset funds just means you are borrowing less.

If someone starts going on about savings rate is at the mortgage rate walk away.

Same rules apply to any borrowing lower rate lower interest

Unless you bee the benefits of offsetting nearly always cheaper to take regular mortgages at lower rates.

In the good old days when there were lifetime offset trackers at great rates the costs of offsetting were very low but these days there are few deals good enough.

0 -

Pandaman - you have been misled here.

Had you no funds offset you would current be paying 4.49% interest on your £175,000 mortgage.

With an offset account balance of £175,000, your mortgage is fully offset, you pay no interest, just repay capital.

If you take £30,000 out of your offset account you will be charged 4.49% interest on £30,000 of your mortgage balance, with just £145,000 offsetting. Clearly, if you put the mortgage on a 1.68% rate you will be paying less interest on the £30,000 (about £70 a month). To suggest anything else is nonsense.

I suspect what has happened here is that the staff member you spoke to made a poor attempt of using their offset calculator.

https://www.coventrybuildingsociety.co.uk/mortgages/calculators/intermediaries/OffsetCalculator.aspx

(Which incidentally, is so stone age, you need Adobe Flash loaded on your browser to use it)

I do not know your property value, or mortgage term, or tax rate. But making some assumptions in the calculator it told me you would save £30,000 on a 10 year period on the higher mortgage rate, and £20,000 on the lower mortgage rate. This is hardly surprising on closer consideration. The calculator could instead tell you that you would pay £30,000 more on the higher interest rate than on the lower interest rate - something we can all work out.

Points to note:

1) If you are offsetting at 100%, the mortgage rate makes no difference to your net costs.

2) The moment you are not offsetting 100% your mortgage rate makes a difference

3) You will always need to consider the loss of potential of having your funds elsewhere

4) If the event of the Bank crashing your funds are protected to £85,000 maximum, therefore offsetting above that is a risk, albeit a small one

5) Your tax rate is relevant to the loss of potential of having your funds elsewhere not your offsetting

Hope that helps

I am a Mortgage Broker

You should note that this site doesn't check my status as a Mortgage Broker, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.0 -

I thought so too initially and was perplexed, but upon closer inspection, the key point to consider from CBS is below:amnblog said:If you take £30,000 out of your offset account you will be charged 4.49% interest on £30,000 of your mortgage balance, with just £145,000 offsetting. Clearly, if you put the mortgage on a 1.68% rate you will be paying less interest on the £30,000 (about £70 a month). To suggest anything else is nonsense....current offset interest benefit is calculated using 4.49% on the £145k savings pot thus providing a greater benefit that it would at 1.68%. They run some numbers and it works out to be £80 more on the 1.68% rate than on the 4.49% rate. The comparison they made was that I'm better being on the higher rate unless my savings dropped below £120k.They weren't just calculating the interest charged. My calculations above demonstrate (at least conceptually) how much the offset benefit can reduce monthly payments, as well as the differences in interest charged (£112.25 - £42 = £70.25). Another point to note is the threshold of £120K they mentioned, below which the larger offset benefit (higher interest rate) was no longer cheaper, which strongly implies they were only comparing monthly payments in terms of affordability, as opposed to long term cost. I do agree it was extremely misleading of CBS to frame the comparison only in this manner, without highlighting the increased interest charges and overall cost of the mortgage, as it obviously contradicts conventional wisdom, perhaps an underhanded attempt at extracting further profit.0

I do agree it was extremely misleading of CBS to frame the comparison only in this manner, without highlighting the increased interest charges and overall cost of the mortgage, as it obviously contradicts conventional wisdom, perhaps an underhanded attempt at extracting further profit.0 -

Reminds me of the One account calculator that was very misleading.

If you did not put the numbers in right(for your current account) it double counted your mortgage payment and you paid your mortgage off with less money than you borrowed.

Many people missed that and went with the one account thinking it was somthing magic.

Offset mortgage work because you are overpaying(might be temp and you borrow it back) and that's it, there is nothing magic.

Borrow less even on a temp basis you pay less

Lower rate you pay less overall just don't have a line of credit(unless you have a borrow back overpayment facility).

................................................

4) If the event of the Bank crashing your funds are protected to £85,000 maximum, therefore offsetting above that is a risk, albeit a small one

You can have more saving than the financial compensation limits as "set off" would cover the excess up to the mortgage0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.6K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.7K Work, Benefits & Business

- 603.1K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards