We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

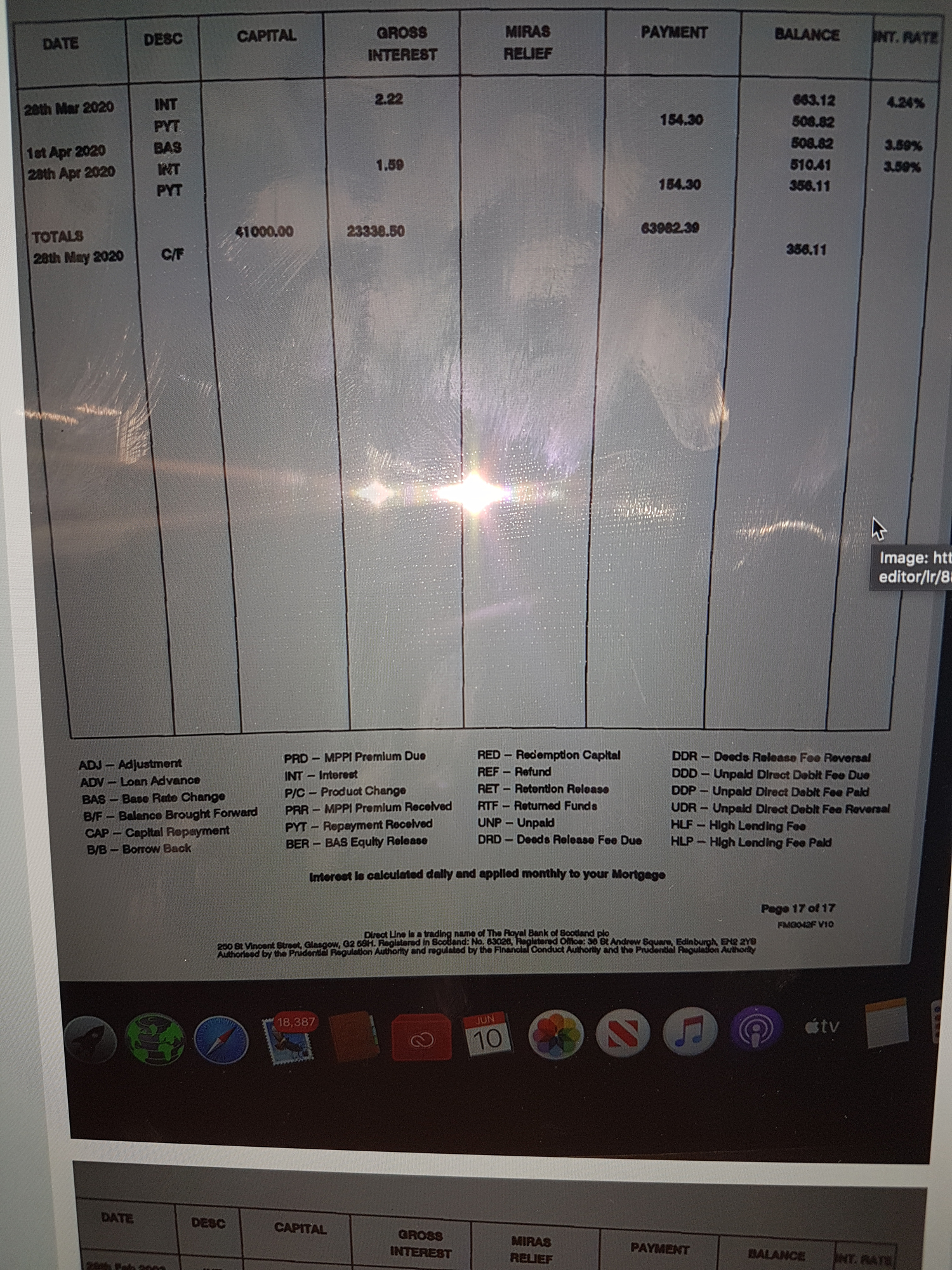

Direct line overpayment on mortgage does not seen right. We still owe despite overpaying 100 a month

Comments

-

Hope you get that last bit.

Now what stood out was• Phone call received from Mr P 18.10.2013 notes recorded as follows ‘incall fromThis was 2013 when base rates were 0.5%

Mr P I advised Mr P that he called to arrange overpayment to £100.00 above minimum on 14/07/2009 I advised term remaining 7 years and 3 months, I advised at 4.00% paying £518.55 term would reduce to approximately 7 years and 3 months Mr P. okay with this’

looking at a later number• Phone call received from Mr P 14.08.2017 notes recorded as follows ‘incoming call from Mr P advised balance £12,326.49, I advised if redeeming today £12,348.02, I advised term remaining 3 years 5 months and paying £100.00 over and above so paying £452.24 and at this rate could be repaid 2 years 5 months. Mr p will continue to pay £100.00 over and above, I advised no penalties for14.08.2017 balance £12,326.

paying £352.24 3y5m that's a rate of 9.4% (

paying £452.24 2y5m that's a rate 5%

then 08.10.19 balance £2,628

paying £371.26 8m

paying £287.06 10m

Both those would be rate of 10%+ but on very short terms with overpayments the rate varies a lot by a single extra month that does not need a full payment.

what rates have you been paying?

Your LTV must be good so rate should be Low <2%

0 -

Thanks in work i will get all statement posted do you want from statements from 2000 or just from 2009getmore4less said:Hope you get that last bit.

Now what stood out was• Phone call received from Mr P 18.10.2013 notes recorded as follows ‘incall fromThis was 2013 when base rates were 0.5%

Mr P I advised Mr P that he called to arrange overpayment to £100.00 above minimum on 14/07/2009 I advised term remaining 7 years and 3 months, I advised at 4.00% paying £518.55 term would reduce to approximately 7 years and 3 months Mr P. okay with this’

looking at a later number• Phone call received from Mr P 14.08.2017 notes recorded as follows ‘incoming call from Mr P advised balance £12,326.49, I advised if redeeming today £12,348.02, I advised term remaining 3 years 5 months and paying £100.00 over and above so paying £452.24 and at this rate could be repaid 2 years 5 months. Mr p will continue to pay £100.00 over and above, I advised no penalties for14.08.2017 balance £12,326.

paying £352.24 3y5m that's a rate of 9.4% (

paying £452.24 2y5m that's a rate 5%

then 08.10.19 balance £2,628

paying £371.26 8m

paying £287.06 10m

Both those would be rate of 10%+ but on very short terms with overpayments the rate varies a lot by a single extra month that does not need a full payment.

what rates have you been paying?

Your LTV must be good so rate should be Low <2%

0 -

Having gone through that long post I can see where you went wrong.

You let your payments drop and lost some of the benefits of overpaying early with smaller payments later.

I doubt there is anything wrong on the statements what will be interesting is the interest rate you have been paying because based on the numbers given that looked to be high.

Not familiar with direct line mortgages but understand they stopped in 2010 so surprised you did not move to a new lender with better rates?

0 -

0 -

rrrtt

rrrtt

0 -

Cccc

0

0 -

Sorry uploading from phone android apple will not play to well so uploader re organised some into size rather than order... phone hasnt got enough ram to re order statements cutting and pasting..0

-

How come you didn't remortgage away from them?

Statements seem fine though.2 -

Not seeing anything wrong on the numbers on a quick sweep over them.

There are a few time when rates went up but the payment was not recalculated would have to look for a pattern to see why maybe the overpayment meant it did not have to go up.

Page 1. 2000/2001 looks like it started out as a Base+1% tracker.

the rates seem to change with base rate timing but not by the same amount.

by the time we get to 2009 it is sitting at around base +3.5% for most of the next 10 years there are a couple of changes that do not fit with BOE rate changes you need to dig out the change of rate letters

The recalculation of payment every Sept explains why you ended up where you are not reducing the term.

You should be kicking yourself you have been on such a high rate for so long

Did you never think of reviewing your mortgage rate?

2 -

You should have remortgaged a decade ago.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards