We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

The rise of Annuities?

Comments

-

If you intend to outlive the average, if you want to avoid fees, if you value simplicity, and especially if your SP will not cover life's critical essentials - then consider annuities as part of your overall strategy.

If comparing annuities vs investment, don't forget to add in fees as they can be significant.0 -

Where are you going to invest to achieve a 4% drawdown rate. Little possibility of investing in secure bonds at the current time which offer a decent long term yield.ffacoffipawb said:

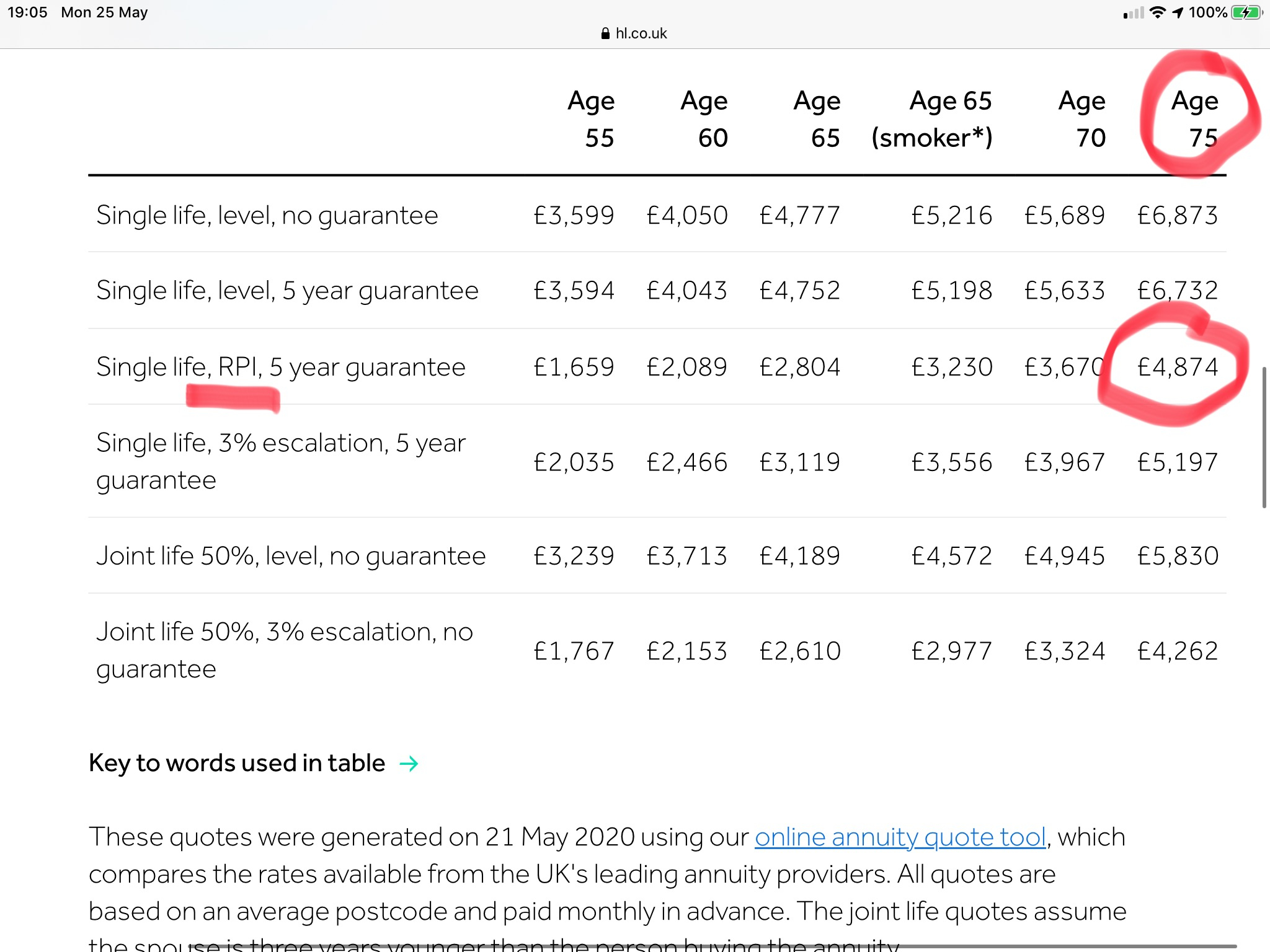

Current single life RPI annuity rates look acceptable at age 75 compared with 4% drawdown rate ...Deleted_User said:Annuities have been and still are a sensible option for at least part of ones portfolio.In addition to reliability and longevity insurance, annuities remove the risk of investors screwing up. After a certain age our decision making abilities become impeded which is why older people tend to make money related mistakes more often.My plan is to convert a significant portion of the overall portfolio to annuity when I am 75. And yes, I think they will become more popular. 1

1 -

Sure. Part of the plan. Also a good idea. Although the rules for SP are more prone to changesLinton said:If you want higher guaranteed inflation linked income as longevity insurance the cheapest way of doing it is by deferring your SP when younger. That gives you the effect of a 5.8% annuity rate.1 -

itwasntme001 said:An index linked annuity can be thought of as a proxy for the safe withdrawal rate under a 100% certainty.No it can't, as the safe withdrawal rate is the one where you run out of money the day of your death and your cheque to the undertaker bounces. (As undesirable and uncomfortable as that would be in reality.) If you buy an annuity you never run out of money even if you live to 200.Individual investors in decumulation can use higher-risk investments than insurance companies, even after allowing for reducing risk in decumulation compared to accumulation. They aren't forced to buy gilts as insurance companies are. Managing your own risks is completely different from managing risk in an annuity pool.The 4% safe withdrawal rate is pessimistic as it makes no allowance for even basic decumulation strategies like not increasing withdrawals if the fund size hasn't increased, or keeping a buffer in cash to avoid pound cost ravaging.My Dad took out a GAR 10% non-index linked annuity (over £10k pa in income) when he was 60 so inflation risk is there but the 10% rate seemed like a no brainer and it has mean that his capital does not need to be touched and thus passed down to me and my sibling.A 10% GAR at age 60 is a no-brainer. There's a reason they don't offer them any more. It has nothing to do with annuities on the current open market.3

-

I am not saying annuities and drawdowns are the same. They are both very different strategies with different methods, risks and costs so I agree with much of what you say Malthusian. What I am saying which you seem to be missing is that the expected return on bonds is the same as the expected return on equities and so whether you fund the retirement with 100% equities or 100% bonds, while with very different risk characteristics, should on an expected basis result in the same outcome. Using annuities requires certainty in payments hence the preference of fixed interest securities as opposed to equities. You could argue that drawdowns would require the same preference as how do you know equities will not enter into a 10 or even 20 year bear market? Would you stop all spending for 10 years just to wait for your portfolio value to climb back up?How do you know those heavily weighted towards equities are being cautious or even just ok with a 4% SWR? Because history says so? I do not think that is sensible even if history is all we have got. Clearly there is a market for annuities at 3% index linked as otherwise why even offer it? Index linking is a valuable feature that pretty much all drawdown strategies misses because most do not usually buy index linked bonds (or at least have a significant investment in). And more importantly now they offer negative yields making index linked annuities very attractive in comparison.1

-

The reason 10% GARs are not offered any more is exactly the same reason why annuity rates have fallen to records lows. It is because expected returns across all liquid asset classes have fallen to 0 or there about. 30-40 years ago real returns (including real interest rates) were comfortable in positive territory. People back then thought it would continue, reinvestment risk was pretty much nil and so insurance companies and pension funds offered what is now very attractive rates for annuities.The biggest risk by far that was underestimated by the pension companies offering 10% GAR was reinvestment risk.1

-

If you are saying that then you are wrong, the expected return on equities is higher than the expected return on bonds because of the higher risk of equtities. If the expected return on bonds was the same as the expected return on equities, why would anybody invest in equities?itwasntme001 said:What I am saying which you seem to be missing is that the expected return on bonds is the same as the expected return on equities and so whether you fund the retirement with 100% equities or 100% bonds, while with very different risk characteristics, should on an expected basis result in the same outcome.

3 -

coyrls said:

If you are saying that then you are wrong, the expected return on equities is higher than the expected return on bonds because of the higher risk of equtities. If the expected return on bonds was the same as the expected return on equities, why would anybody invest in equities?itwasntme001 said:What I am saying which you seem to be missing is that the expected return on bonds is the same as the expected return on equities and so whether you fund the retirement with 100% equities or 100% bonds, while with very different risk characteristics, should on an expected basis result in the same outcome.Market pricing theory suggests that tradable securities are priced such that risk neutrality exists in the market as a whole i.e. equities and bond prices have moved to levels that imply expected returns on both bonds and equities are the same. Because otherwise if equities had a higher expected return than bonds, the market would bid up equities to levels where both expected returns would match again.And yes people can still perfectly logically prefer stocks over bonds because whilst expected returns are the same, equities have more upside because their cashflows are a widely more uncertain than bonds (whilst government's are not perceived to default on their obligations at least).0 -

itwasntme001 said:coyrls said:

If you are saying that then you are wrong, the expected return on equities is higher than the expected return on bonds because of the higher risk of equtities. If the expected return on bonds was the same as the expected return on equities, why would anybody invest in equities?itwasntme001 said:What I am saying which you seem to be missing is that the expected return on bonds is the same as the expected return on equities and so whether you fund the retirement with 100% equities or 100% bonds, while with very different risk characteristics, should on an expected basis result in the same outcome.Market pricing theory suggests that tradable securities are priced such that risk neutrality exists in the market as a whole i.e. equities and bond prices have moved to levels that imply expected returns on both bonds and equities are the same. Because otherwise if equities had a higher expected return than bonds, the market would bid up equities to levels where both expected returns would match again.And yes people can still perfectly logically prefer stocks over bonds because whilst expected returns are the same, equities have more upside because their cashflows are a widely more uncertain than bonds (whilst government's are not perceived to default on their obligations at least).No, bonds and equity are not interchangeable. Bonds provide a guarantee of future repayment which is more valuable than the % return. This is important to major holders of cash such a insurance, life assurance, and pension companies which could not make their guaranteed payouts on the basis of equity investment as they would incur far too much short/medium term risk. You cant go down hardly go down to your high street bank with a £100M in cash. What would the banks do with it? Probably buy bonds after charging you for the privilege.Conversely bonds will almost always lose out to inflation in the long term. Somone putting all their pension contributions into bonds is destined for a retirement in poverty. Equity as a real asset based on people trading goods, should, all other things being equal, at least keep pace with inflation.Private holding of bonds is almost insignificant. Looking at https://fullfact.org/economy/guide-economy-debt/30% of all gilts are owned by insurance companies and pension funds7% is owned by the banks27% is owned by foreign institutions.25% is owned by the BoEwhich only leaves 10% or so to be shared amongst everyone else such as private investors, public and private companies etc etc

3 -

Linton said:itwasntme001 said:coyrls said:

If you are saying that then you are wrong, the expected return on equities is higher than the expected return on bonds because of the higher risk of equtities. If the expected return on bonds was the same as the expected return on equities, why would anybody invest in equities?itwasntme001 said:What I am saying which you seem to be missing is that the expected return on bonds is the same as the expected return on equities and so whether you fund the retirement with 100% equities or 100% bonds, while with very different risk characteristics, should on an expected basis result in the same outcome.Market pricing theory suggests that tradable securities are priced such that risk neutrality exists in the market as a whole i.e. equities and bond prices have moved to levels that imply expected returns on both bonds and equities are the same. Because otherwise if equities had a higher expected return than bonds, the market would bid up equities to levels where both expected returns would match again.And yes people can still perfectly logically prefer stocks over bonds because whilst expected returns are the same, equities have more upside because their cashflows are a widely more uncertain than bonds (whilst government's are not perceived to default on their obligations at least).No, bonds and equity are not interchangeable. Bonds provide a guarantee of future repayment which is more valuable than the % return. This is important to major holders of cash such a insurance, life assurance, and pension companies which could not make their guaranteed payouts on the basis of equity investment as they would incur far too much short/medium term risk. You cant go down hardly go down to your high street bank with a £100M in cash. What would the banks do with it? Probably buy bonds after charging you for the privilege.Conversely bonds will almost always lose out to inflation in the long term. Somone putting all their pension contributions into bonds is destined for a retirement in poverty. Equity as a real asset based on people trading goods, should, all other things being equal, at least keep pace with inflation.Private holding of bonds is almost insignificant. Looking at https://fullfact.org/economy/guide-economy-debt/30% of all gilts are owned by insurance companies and pension funds7% is owned by the banks27% is owned by foreign institutions.25% is owned by the BoEwhich only leaves 10% or so to be shared amongst everyone else such as private investors, public and private companies etc etcI never said they were interchangeable. Clearly both have different risk profiles. But that does not mean they can not be compared. How do you know that from today in 10 or 20 years time there is a 100% certainty that bonds will lose out to inflation? Same question with equities but instead of lose out, how do you know with 100% certainty that equities will keep pace with inflation at least?Out of the 30% of gilts owned by pension funds and insurance companies, how much do you think is held on behalf of private investors? What are the stats for equity ownership? why does private vs public ownership even matter? Prices are determined at the margin.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.3K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.9K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.4K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards