We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

KRBS not updating the Interest rate on their tracker mortgages

Zypher20

Posts: 7 Forumite

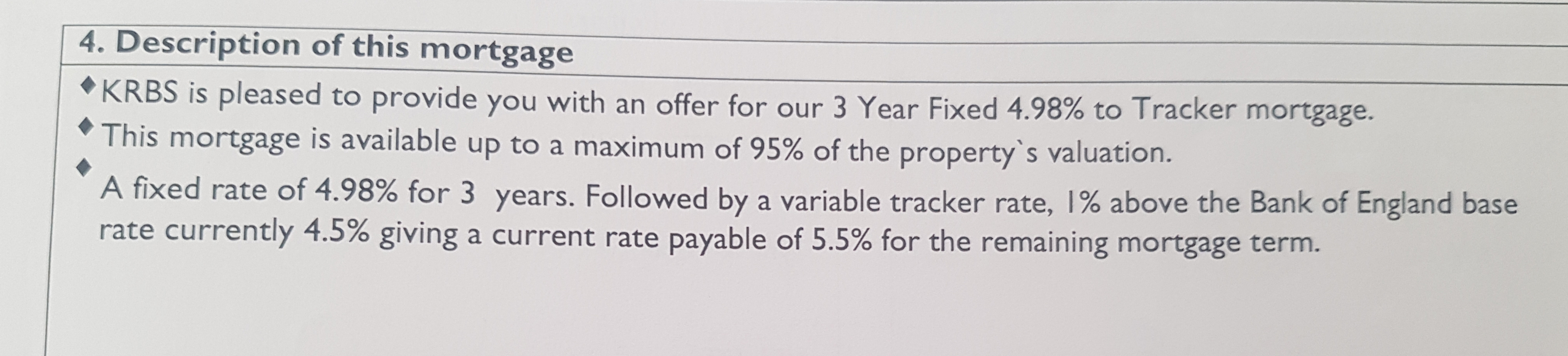

I currently have a tracker mortgage with Kent reliance building society which is 1% above the bank of england base rate.

However they have not updated my interest rate for the last 2 rate reductions. I phoned them today and was told they havent made a decision on the base rate reduction.

I informed them they dont need to make a decision the BoE makes the decision on the base rate. They just need to track it as per my mortgate terms. There is no minimum rate mentioned in my mortgage documents.

I am guessing this will be affecting anyone with a tracker mortgage with KRBS and their failure to adhere to the mortgage agreement is astounding.

However they have not updated my interest rate for the last 2 rate reductions. I phoned them today and was told they havent made a decision on the base rate reduction.

I informed them they dont need to make a decision the BoE makes the decision on the base rate. They just need to track it as per my mortgate terms. There is no minimum rate mentioned in my mortgage documents.

I am guessing this will be affecting anyone with a tracker mortgage with KRBS and their failure to adhere to the mortgage agreement is astounding.

0

Comments

-

There's obviously a clause within the product terms and conditions that gives them some discretion.0

-

There certainly isnt in my mortgage agreement. Problem is there isnt much I can do to make them adhere to the contract.

Raised a complaint with the financial ombudsman and sent a message to the fca but that's about all I can do. Other tha raise awareness on it on sites like this.0 -

FOS can only consider if you first make a formal complaint to Kent Reliance and your complaint is rejected. FCA doesn't take customer complaints.

In any case, I think you are being too impatient. The Kent Reliance website says:If you have a mortgage product that is linked to the Bank of England Base rate, then your monthly payments will change. We will confirm the changes in writing to you shortly.https://www.kentreliance.co.uk/support/base-rate-change-mortgage-faqs#4c015c13-2bd9-6312-8b0f-ff0000de2d98

0 -

Yes it has said that for the last month, and was not what was said when I called. For a baking system which is most likely mostly automated it should not take over a month for someone to input the new bank of England base rate onto the system.

How long is considered a reasonable time frame for changes in the base rate to be reflected on the mortgages? The first reduction in the base rate was the 10th March and colleages who hold tracker mortgages with other companies get their updated payments through before the lockdown even started.

I think such a long delay would not be the case if the rate had increased.0 -

Switch mortgage lender if you don't like the service given. KRBS have to consider the commercial impact on the business in making changes to their interest rates.0

-

I suspect it's more a case of the call centre operator giving a standard response that doesn't apply for rates linked to the base rate. Time will tell.

The Kent Reliance mortgage conditions state that changes to the interest rate will take effect on the day of the change to the base rate, and that they will give you notice of any change within a "reasonable time" after that change. I guess it has been over a month so I can sympathise with the OP, but you do have to make allowances for the current situation, with home-working, elevated sickness levels and increased customer contacts, it is probably taking them longer than usual to process the changes.0 -

I have just had a look at a Kent Reliance KFI - admittedly for a BTL rather than a residential mortgage and it actually follows the Kent Reliance Variable rate - not the Bank of England base rate. Does yours definitely follow the BoE base rate? If it does, you are right. If it does not then they can more or less do what they like.I am a Mortgage AdviserYou should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.0

-

Picture of mortgage offer back from 2006.

I would be crazy to change mortgage provider as who else will give 1% above BoE base rate and it's also a shared ownership mortgage which are hard to come by.

I understand covid 19 will lower staffing levels but I still managed to get though to their contact centre in under 5 minutes so they cannot be that stretched. ( can be waiting hours to get on b&q website)

When I spoke to them they went away twice to check about the rate both times saying they had not yet made a decision about the interest rates for their tracker mortgages. (He already had my account details so knew I was talking about an existing mortgage)

This suggests it's not a delay in updating their systems but a conscious decision to delay reducing their rates inline with mortgage agreement.

Personally the difference will be minimal however if I delayed increasing my payment when the rates went up I am sure they would be quick to react.

Others in the same situation may well have mortgages over 100/200k where a 0.65% difference in interest rates will make a noticable difference in their payments at a time when many may be on a reduce 80% wage or getting by on a redundancy payment.

1 -

Fair enough.

They could be seeing if there is anything in the contract about extreme circumstances or something to prevent it maybe? But on the face of it you seem to be right.

I am a Mortgage AdviserYou should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards