We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

A few tax relief questions

Comments

-

https://www.pensionsadvisoryservice.org.uk/about-pensions/saving-into-a-pension/pensions-and-tax/the-annual-allowance

Employer contributions do count in terms of the annual allowance.

https://www.which.co.uk/money/pensions-and-retirement/personal-pensions/contributing-to-a-private-pension-explained/how-the-pensions-annual-allowance-works-ac8d33u9v9ch

1 -

Employer contributions do count in terms of the annual allowance.I'm not saying they don't.But (at least in this instance) the annual allowance (for the total of employer+employee) is £40,000.And the mother is limited for her own contributions, within that, to her gross wage (£10,000)What seems to be at issue is do the employer contributions count against that £10,000, or just the £40,000.The link the OP found seems to indicate that it's set against both (reducing the amount the mother may contribute) - mine says just the £40,000 (so she's still left with £10,000 minus anything she herself has already contributed.)Conjugating the verb 'to be":

-o I am humble -o You are attention seeking -o She is Nadine Dorries1 -

I don't know why this always causes such confusion even amongst the regulars here. It's discussed every week. See https://forums.moneysavingexpert.com/discussion/comment/76833367#Comment_76833367 and the Pru link which is a good explaination

1 -

But the website for the LGPS she is in says this:xylophone said:Your mother has "relevant earnings" and she is contributing to a scheme offering "relief at source".

Will I receive tax relief on my contributions to the LGPS?

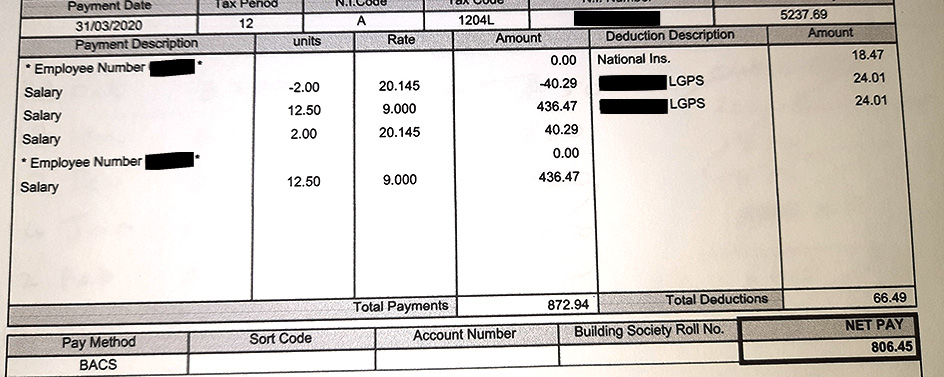

Yes. As a member of the LGPS, your contributions receive tax relief by deducting your contributions from your pensionable pay before any tax is calculated. For most people this is a saving of 20% but higher rate tax payers will receive a higher rate of relief.This is a copy of her latest payslip. She's supposed to pay 5.5% of pensionable pay, which this shows.

Whether the tax relief is relief at source or on net pay, when working out her remaining contributions, should she still be allowing for the tax relief or will not paying any tax make a difference?

Her end of year deductions show that she's contributed £617.99 and LGPS have contributed £2078.72. Should she account for the additional tax relief?

Again, apologies for all the questions. I'm trying to get my head around it.

0 -

LGPSAh. That's different - we were all (well I was, certainly) assuming a defined contribution pension - that looks like a defined benefit one.And not something I can helpfully comment on.

Conjugating the verb 'to be":

-o I am humble -o You are attention seeking -o She is Nadine Dorries1 -

sparky0138 said:

But the website for the LGPS she is in says this:xylophone said:Your mother has "relevant earnings" and she is contributing to a scheme offering "relief at source".

Will I receive tax relief on my contributions to the LGPS?

Yes. As a member of the LGPS, your contributions receive tax relief by deducting your contributions from your pensionable pay before any tax is calculated. For most people this is a saving of 20% but higher rate tax payers will receive a higher rate of relief.This is a copy of her latest payslip. She's supposed to pay 5.5% of pensionable pay, which this shows.

Whether the tax relief is relief at source or on net pay, when working out her remaining contributions, should she still be allowing for the tax relief or will not paying any tax make a difference?

Her end of year deductions show that she's contributed £617.99 and LGPS have contributed £2078.72. Should she account for the additional tax relief?

Again, apologies for all the questions. I'm trying to get my head around it.

What they say above ie "As a member of the LGPS, your contributions receive tax relief by deducting your contributions from your pensionable pay before any tax is calculated" is wrong in her case. Because she earns below the personal allowance, she doesn't get any tax relief on her LGPS contribution, as it uses "net pay" (which is a confusing HMRC term - it means, as it says above, that conts are deducted before tax is applied - this means if she doesn't earn enough to pay tax, there is no tax relief).Look at the "total taxable to date", is that on the payslip, because you haven't shown it. This will be gross pay minus her LGPS contributions. The amount she can pay into a SIPP/personal pension this tax year is 80% of the "total taxable to date", the SIPP provider will claim the additional 20% from HMRC. This is because a SIPP is a RAS (relief at source) scheme, in which you can get tax relief below the personal allowance, unlike a "net pay" scheme like LGPS.

0 -

But the website for the LGPS she is in says this:

Aargh! You made no mention of the fact that she was in LGPS - your only mention was of a pension with Fidelity.

Let's be clear - your mother is in LGPS and has a pension with Fidelity?

In terms of her LGPS defined benefit pension, if she is only earning £10,000 a year then she is not receiving any tax relief - this is because the scheme (unlike a personal pension with Fidelity), operates Net Pay rather than Relief at Source.

0 -

Sorry for the confusion. She has a SIPP with Fidelity which is invested in Vanguard 60. She's made some regular contributions to that this year. She's also in a LGPS. Here's the taxable pay and total deductions part on her final payslip of the tax year:

Here are some figures:

Gross salary: £10,474.68

Net contributions to SIPP: £1220

Contributions to LGPS: £617.99

Employer contributions to SIPP (assuming that's what the ERS line means): £2078.72

The thing is, the contributions her payslip says she's made to the LGPS don't add up to her ACTUAL contributions. She only paid in £576.12. Does anyone know why those figures might differ?0 -

sparky0138 said:Sorry for the confusion. She has a SIPP with Fidelity which is invested in Vanguard 60. She's made some regular contributions to that this year. She's also in a LGPS. Here's the taxable pay and total deductions part on her final payslip of the tax year:

Here are some figures:

Gross salary: £10,474.68

Net contributions to SIPP: £1220

Contributions to LGPS: £617.99

Employer contributions to SIPP (assuming that's what the ERS line means): £2078.72

The thing is, the contributions her payslip says she's made to the LGPS don't add up to her ACTUAL contributions. She only paid in £576.12. Does anyone know why those figures might differ?

Make no sense. The salary only adds to about £6500, clearly wrong. Employer wouldn't be paying into the SIPP surely? Those would be payment to LGPS presumably? Didn't your mother pay direct to the SIPP?

0 -

Her wage slips changed to online a few months ago. On her old paper wage slips it used to say taxable pay, pension paid and NI paid. The taxable pay and pension paid added up to her gross pay. Now it does not. You're right, this makes no sense.Make no sense. The salary only adds to about £6500, clearly wrong. Employer wouldn't be paying into the SIPP surely? Those would be payment to LGPS presumably? Didn't your mother pay direct to the SIPP?

Her employers are only contributing to the workplace pension, which she is paying 5.5% of her wages into. The SIPP is separate and she's been making some monthly contributions to that.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards