We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

State Pension forecast & NI contributions

Squirall

Posts: 27 Forumite

Hello, I am a little bewildered that after paying NI contributions for 42 years & serving 22 years in the RAF, that I have been asked to 'top up my contributions' to receive a FULL State Pension. I believe you only need 30 years NI contributions. But they are asking for over £2,000 to make it so I receive the full pension .

0

Comments

-

Did you contract out of the state pension at all?

1 -

Did you contract out of the state pension at all?

The OP says

serving 22 years in the RAF,All armed forces schemes were contracted out.

The OP may also have been a member of other contracted out schemes.

2 -

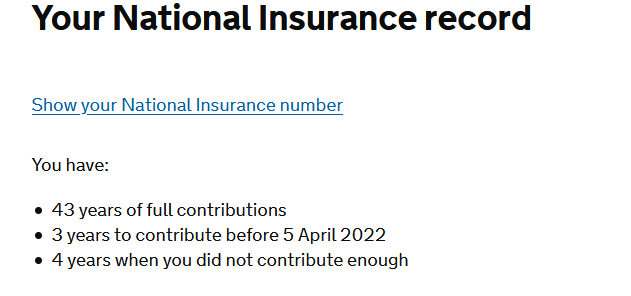

Thank you for replying - yes I contracted out for about 10 years but it says I have 43 years full contributions

0 -

Squirall it does not matter how many years if you contracted out. I have a full 49 years will start my SP next month but the most I can get is £152.37 a week and I am only getting that because of the 2016 new rules, so I won't "retire" until 65 & 9 months. Not that I am going to retire now, I shall become a burden on my workplace since they cannot retire me :-0) and enjoy not paying NI that will take care of the extra Tax.Paddle No 21:wave:2

-

OP

https://www.moneyforce.org.uk/News/2017/September/The-State-Pension-and-you

At 6/4/16, two calculations were done for you.

Old Rules

NI years [up to 30] /30 x £119.30 + (Additional State Pension - Deduction for Contracting Out).

New Rules

(NI years [up to 35]/£155.65) - Contracted Out Pension Equivalent.

Your "starting amount" was the higher of the two.

In your case the starting amount was under a full NSP - you have the opportunity to increase up to the full amount by post 2016 contributions.

See https://www.royallondon.com/siteassets/site-docs/media-centre/good-with-your-money-guides/gwymg-8-new-state-pension-april-2019-edition-interactive.pdf

https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/210299/single-tier-valuation-contracting-out.pdf

2 -

It depends what you call "the full pension". You have still got what you earned under the old scheme, if you want to get the full "new" pension you will need to contribute more in accordance with the rules. You are lucky that you get a second bite at the cherry. When I stopped working I was resigned to getting around £128 under the old scheme then along came the new scheme and I could top it up.Squirall said:Hello, I am a little bewildered that after paying NI contributions for 42 years & serving 22 years in the RAF, that I have been asked to 'top up my contributions' to receive a FULL State Pension. I believe you only need 30 years NI contributions. But they are asking for over £2,000 to make it so I receive the full pension .

2 -

Squirall said:Hello, I am a little bewildered that after paying NI contributions for 42 years & serving 22 years in the RAF, that I have been asked to 'top up my contributions' to receive a FULL State Pension. I believe you only need 30 years NI contributions. But they are asking for over £2,000 to make it so I receive the full pension .Ditto. You and I are in good places pensionwise - we paid reduced NI during our contracted out service, have been getting our RAF pensions since our 40s, and still have the opportunity of topping up our State pensions to the full single tier rate.Assuming you will be a basic rate tax payer in retirement, you'll get your £2K back after just 4 years. After that, you'll be quids in.ADD: When DWP say that you have "43 years of full contributions" they actually mean "full financial years" and not "full rate of NI, non-contracted out, years".

2 -

Thank you, I didn’t know services members were automatically contracted out.xylophone said:Did you contract out of the state pension at all?The OP says

serving 22 years in the RAF,All armed forces schemes were contracted out.

The OP may also have been a member of other contracted out schemes.

1 -

The full, meaning maximum, state pension is currently over £300 a week and it's impossible for someone with your work record to receive that much because it requires maximum earnings-related NI contributions and instead of paying them your armed forces pension scheme chose not to pay those but instead to take responsibility for those payments itself, contracting you out of the earnings-related part of the state pension accrual. That's good news for you because it allows you to get doubly paid.Squirall said:Hello, I am a little bewildered that after paying NI contributions for 42 years & serving 22 years in the RAF, that I have been asked to 'top up my contributions' to receive a FULL State Pension. I believe you only need 30 years NI contributions. But they are asking for over £2,000 to make it so I receive the full pension .

Since 2016 there's been a cap on new state pension accrual at the single tier state pension level, currently £168.60 a week. Those at that level get to pay full NI and get no more state pension. But your work pension is ignored so while someone not contracted out would be over that threshold you aren't. Which is excellent news because if your life expectancy is normal extra years are a bargain.

Most people with lots of contracted out years will have a combination of old rules calculation before 2016 and new from then, because this produces a higher payment than the alternative of new rules throughout. This calculation has three parts:

1. Basic state pension. 1/ 30th of the basic state pension per full year paying in or getting credits. The "43 years of full contributions" part of your forecast mostly refers to this (includes post-2016 also) and means that you have accrued the maximum possible basic state pension, currently £129.20 a week. Contracting out doesn't affect this.

2. Earnings-related state pension. Extra accrual based on earnings, almost all of it not accrued while in a contracted out pension. You have some of this, mostly from the after RAF years.There is no contracted out deduction under these rules, the money was never accrued in the first place.

3. Single tier pension years starting from 2016. 1 / 35th of the single tier pension accrued peer year until you reach the single tier cap, currently £168.60 a week.

What your forecast is doing is telling you that there's still room for you to get up to the cap by earning, getting credited with or buying some more years from 2016 onward. Don't buy any years before 2016, those won't get you any increase.

We can't yet give an explicit answer about years to buy. To do that we need to know:

a. the amount based on your current contribution record

b. what years are available for you to buy.

You could also phone the Future Pension Centre and they will be able to tell you which years are beneficial.0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.8K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.9K Work, Benefits & Business

- 603.4K Mortgages, Homes & Bills

- 178.2K Life & Family

- 260.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards