We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Want to become a Forum Ambassador? Visit the Community Noticeboard for details on how to apply

IVA or loan

nobbyclarke123

Posts: 21 Forumite

Okay guys & Girls,

would like to get your opinion on a situtation that I'm in.

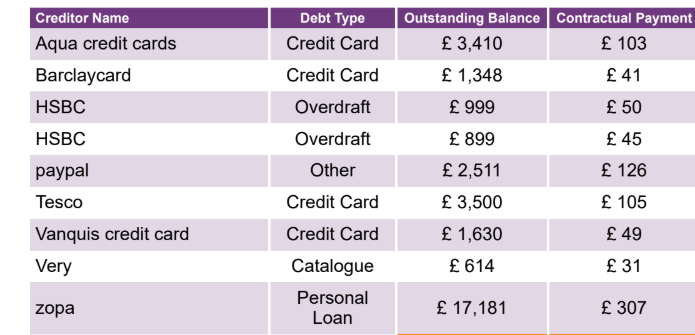

I have gotten myself into a mess with credit cards and decided to tackle this head on. I contacted stepchange and followed their debt remedy advice, they have given me a number of option for my situation, but recomend that an IVA would be the best solution.

My income is circa £2100 after tax, NI, Student Loan & pension.

my outgoing are approximately £1992

I spoke to my boss, to ensure that entering an IVA wouldnt cause and adverse issues at work. He asked me to give him a copy of my debt advice and he would get back to me.

He then made me an offer, to loan me £15k to clear my cards, and leave me with only my fixed sum loan to repay. he would take all repayments for the £15k from, 50% of my overtime and 100% of my bonuses (excluding christmas) he would however expect me to increase my weekly overtime to 10hours each week. but believes that within 3 years i will have cleared the loan and be in a better situation than an IVA would leave me in...

do you think that this is the best solution ?

would like to get your opinion on a situtation that I'm in.

I have gotten myself into a mess with credit cards and decided to tackle this head on. I contacted stepchange and followed their debt remedy advice, they have given me a number of option for my situation, but recomend that an IVA would be the best solution.

My income is circa £2100 after tax, NI, Student Loan & pension.

my outgoing are approximately £1992

I spoke to my boss, to ensure that entering an IVA wouldnt cause and adverse issues at work. He asked me to give him a copy of my debt advice and he would get back to me.

He then made me an offer, to loan me £15k to clear my cards, and leave me with only my fixed sum loan to repay. he would take all repayments for the £15k from, 50% of my overtime and 100% of my bonuses (excluding christmas) he would however expect me to increase my weekly overtime to 10hours each week. but believes that within 3 years i will have cleared the loan and be in a better situation than an IVA would leave me in...

do you think that this is the best solution ?

0

Comments

-

If it avoids insolvency, then yes, it might be a good idea, but to make it work, you must close down the card accounts, and not re-use them, you must also learn to budget better, and start living within your means, otherwise you will just make the situation worse.

If you can do all of that, and the boss is willing, then fair enough, but a lot of people who consolidate their debts, do so without changing their spending habits, and it can backfire spectacularly badly, so be warned.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter2 -

Its not a personal loan is it but 1 from the company ?Id get it in writing, sounds a good idea as long as you don't end up creating more debt and you rigorously stick to a budget, reduce what you pay for utilities, phone contract.0

-

No this wouldnt be a personal loan, but one from the company to myself as an employee.DCFC79 said:Its not a personal loan is it but 1 from the company ?Id get it in writing, sounds a good idea as long as you don't end up creating more debt and you rigorously stick to a budget, reduce what you pay for utilities, phone contract.

Thank you for this advice, the plan is to repay all cards, close the accounts and never use them again as I just do not have the self discipline required to use them safely.sourcrates said:If it avoids insolvency, then yes, it might be a good idea, but to make it work, you must close down the card accounts, and not re-use them, you must also learn to budget better, and start living within your means, otherwise you will just make the situation worse.

If you can do all of that, and the boss is willing, then fair enough, but a lot of people who consolidate their debts, do so without changing their spending habits, and it can backfire spectacularly badly, so be warned.0 -

Is this an interest free loan?

I'd be very wary of mixing work with my personal finances.

However, I'm not sure who has who over what barrel here?

They're going to want you to jump through hoops, at their discretion...but they won't want you to leave as you might default if you're out of work!!How's it going, AKA, Nutwatch? - 12 month spends to date = 3.24% of current retirement "pot" (as at end December 2025)0 -

Regarding interest - the plan was for this to be interest free, but the goverment rules say a loan over £10k that is interest free is classed as a benifit in kind.Sea_Shell said:Is this an interest free loan?

I'd be very wary of mixing work with my personal finances.

However, I'm not sure who has who over what barrel here?

They're going to want you to jump through hoops, at their discretion...but they won't want you to leave as you might default if you're out of work!!

Therefore the interest will be 2.5% reducing until the balance falls below the £10k threshold, after which the interest will reduce to zero ?

I think that if anything, the company will have me over the barrel, but the company is also one of the most down to earth & best i have ever worked for !0 -

Nobby - why did stepchange recommend an IVA? Are you a homeowner? You've got around 32k debt, and around £100 per month available. An IVA is going to cost you £6k if they can get one through at that level. Bankruptcy would cost less as long as yu don't have an asset to protect.0

-

Nobby - why did stepchange recommend an IVA?Rhetorical question. Why did you think they recommended it?

To the OP. Has your boss investigated the implications of a company loan to an employee from the tax and NI point of view? HMRC are all over these at the moment with IR35 so may attract more notice than he might want. This could put you in a difficult position later.

Can't post the link yet but search the Gov UK site for loans to employees.

- All land is owned. If you are not on yours, you are on someone else's

- When on someone else's be it a road, a pavement, a right of way or a property there are rules. Don't assume there are none.

- "Free parking" doesn't mean free of rules. Check the rules and if you don't like them, go elsewhere

- All land is owned. If you are not on yours, you are on someone else's and their rules apply.

0 -

Not sure why they recommend an IVA over bankruptcy... tbh and insolvency solution isnt really what I wanted to do.fatbelly said:Nobby - why did stepchange recommend an IVA? Are you a homeowner? You've got around 32k debt, and around £100 per month available. An IVA is going to cost you £6k if they can get one through at that level. Bankruptcy would cost less as long as yu don't have an asset to protect.

My boss has looked into the tax implications, and hence the interest being charged whilst the balance is over the 10k interest free the the gov set.

0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.9K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.9K Work, Benefits & Business

- 603.5K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards