We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Extending borrowing power for FTBs

bobshi

Posts: 5 Forumite

I have an average salary.

I spend zero. No gyms, iPhones or avocado toast for me.

My mortgage potential across the lenders is £125k-130k.

I have a hefty £80k deposit saved.

Unfortunately only sheds are available in the area for that total sum, yet I know with my zero outgoings that I can afford, even with rate rises, a much higher mortgage.

Realistically, having used budget planners to cater for all spending, I could easily afford a mortgage of about £30k more than that whilst still having a great deal of left over dosh per month for unexpected spending, high inflation or rate rises etc.

What options are available for extending the mortgage borrowing power? For example family assistance.

I am aware of the Post Office's First Start product, but this seems geared toward high LTV ratios and so the interest rates begin a lot higher. Further more at the end of the fixed term, how would I go about remortgaging to a new cheaper fixed deal? The chances are my wage growth would not be sufficient to get a mortgage by myself to cover the remaining mortgage balance.

I spend zero. No gyms, iPhones or avocado toast for me.

My mortgage potential across the lenders is £125k-130k.

I have a hefty £80k deposit saved.

Unfortunately only sheds are available in the area for that total sum, yet I know with my zero outgoings that I can afford, even with rate rises, a much higher mortgage.

Realistically, having used budget planners to cater for all spending, I could easily afford a mortgage of about £30k more than that whilst still having a great deal of left over dosh per month for unexpected spending, high inflation or rate rises etc.

What options are available for extending the mortgage borrowing power? For example family assistance.

I am aware of the Post Office's First Start product, but this seems geared toward high LTV ratios and so the interest rates begin a lot higher. Further more at the end of the fixed term, how would I go about remortgaging to a new cheaper fixed deal? The chances are my wage growth would not be sufficient to get a mortgage by myself to cover the remaining mortgage balance.

0

Comments

-

Look further afield. The challenges you face are no different to previous generations.0

-

With respect, that is total nonsense.Thrugelmir wrote: »Look further afield. The challenges you face are no different to previous generations.

We know that the income-to-house-price ratio for first time buyers is higher than it has ever been. And much higher than decades ago. It is undeniably different to previous generations.

Anyway, in regards to 'look further afield', this is looking further afield. The sum I need, and can afford, tallies with what I require looking further afield.

If I look close by to either my parental home, or work, I would need a whole lot more.

So take your assumptions elsewhere and provide useful information or don't bother replying.0 -

With respect, that is total nonsense.

We know that the income-to-house-price ratio for first time buyers is higher than it has ever been. And much higher than decades ago. It is undeniably different to previous generations.

Anyway, in regards to 'look further afield', this is looking further afield. The sum I need, and can afford, tallies with what I require looking further afield.

If I look close by to either my parental home, or work, I would need a whole lot more.

So take your assumptions elsewhere and provide useful information or don't bother replying.

With all due respect it is you that that is making assumptions. Coming across as highly opinionated isn't the way to garner information on this forum.

For your information I had the same problem as you. As we could only borrow 2.75 times joint income at the time. Didn't go far in Surrey over 3 decades ago. So Imoved further afield. Resulting in a longer commute to work.

With that I'll leave you to your posturing.

PS. Maximum mortgage term was only 25 years. No 40 years terms back then. Or Help to Buy Schemes.0 -

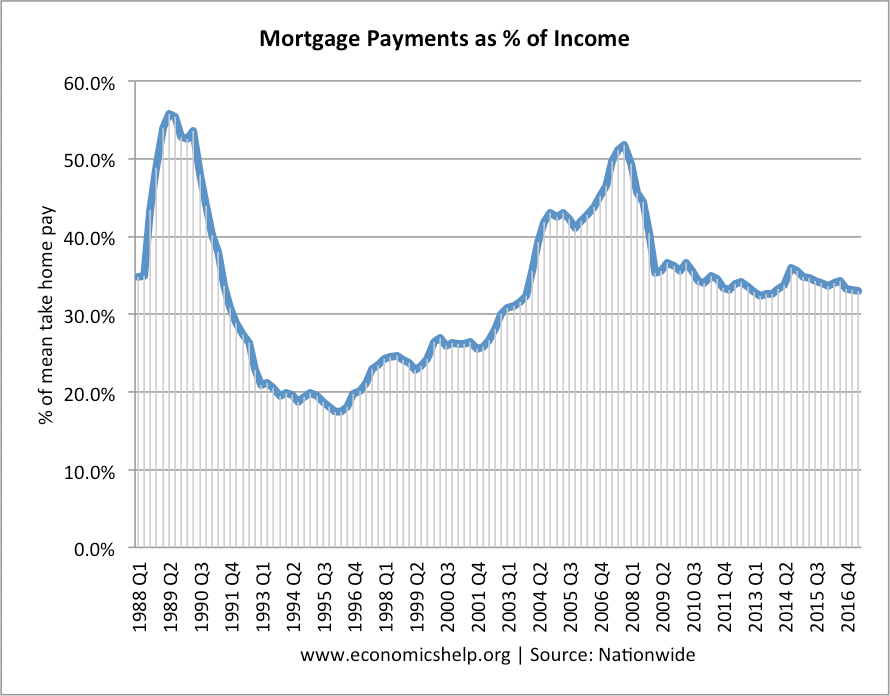

Mortgage payments to income seem about the average point over the last 30years.

https://www.economicshelp.org/wp-content/uploads/2015/09/mortgage-payments-as-percent.png

But yes since MMR we now have banks checking on ‘ affordability ‘ which is full of holes as per your case as you can ‘afford’ more due to lower trivial spending. Takes the decision process away from you to save those poor with financial acumen from themselves.

A lot more of FTB get help with deposits from parents these days than they did before.0 -

I have an average salary.

I spend zero. No gyms, iPhones or avocado toast for me.

My mortgage potential across the lenders is £125k-130k.

I have a hefty £80k deposit saved.

Unfortunately only sheds are available in the area for that total sum, yet I know with my zero outgoings that I can afford, even with rate rises, a much higher mortgage.

Realistically, having used budget planners to cater for all spending, I could easily afford a mortgage of about £30k more than that whilst still having a great deal of left over dosh per month for unexpected spending, high inflation or rate rises etc.

What options are available for extending the mortgage borrowing power? For example family assistance.

I am aware of the Post Office's First Start product, but this seems geared toward high LTV ratios and so the interest rates begin a lot higher. Further more at the end of the fixed term, how would I go about remortgaging to a new cheaper fixed deal? The chances are my wage growth would not be sufficient to get a mortgage by myself to cover the remaining mortgage balance.

You can ask someone to go on the mortgage with you to boost affordability (although may mean paying more stamp duty)

You could ask a family member to be a joint borrower whilst you remain the sole owner (should affect any stamp duty as they wouldnt an owner)

Beyond that, not a lot of options0 -

The best and likely easiest thing to do is to increase your salary. Take on a second job, gain new skills and progress at work, or just increase your hours.

Once you have the mortgage, and are in the new home, you can then decide whether to keep forging ahead at work or if you are able to take it easier.0 -

How much is your annual income?

How much are your commitments? (Loans/CC/HP etc)

How many kids do you have?

How old are you?

How much do you want?

You can potentially get maybe 5.5x or 6x income but it is unlikely to be at an interest rate of normal banks. There are lenders who assess affordability more closely which can work out better for someone in your situation.I am a Mortgage AdviserYou should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.0 -

With respect, that is total nonsense.

We know that the income-to-house-price ratio for first time buyers is higher than it has ever been. And much higher than decades ago. It is undeniably different to previous generations.

Anyway, in regards to 'look further afield', this is looking further afield. The sum I need, and can afford, tallies with what I require looking further afield.

If I look close by to either my parental home, or work, I would need a whole lot more.

So take your assumptions elsewhere and provide useful information or don't bother replying.

The world is very different from how it was when I was young. People (with special attention to liberals) who got free university education voted to take that away from those following them. People with generous final salary pensions said those were unaffordable for others.

Mortgages however are in many ways better than the old days. We used to get 2.5 times one salary plus 1 time the second. When I set out to get one the first building society I went to said I had to save with them for 2 years before being considered for a loan.

That fades into insignificance compared to a woman I spoke to who was probably about 15 years older than me. As a woman she couldn't get a mortgage. She had been to her bank 3 times asking for one and was told no. Then her bank manager asked to see her. He told her there was a customer who had bought a flat and been unable to pay the mortgage. As she wanted a mortgage she could have one if she took on the flat. She did and was delighted to get the chance.

Can you imagine someone pulling a stunt like that today?0 -

OP either wait to get a house, or buy further afield. I moved out of London because I couldn't afford to buy.

Your salary is what limits you and/or house prices. Which one can you control?"It is prudent when shopping for something important, not to limit yourself to Pound land/Estate Agents"

G_M/ Bowlhead99 RIP0 -

You may spend zero but won't be once you have bought.

What's your post purchase SOA look like?

If realistic you may find lenders that will look at it.0

{kind=link}

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.1K Reduce Debt & Boost Income

- 455K Spending & Discounts

- 246.5K Work, Benefits & Business

- 602.8K Mortgages, Homes & Bills

- 178K Life & Family

- 260.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards