We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Sence Check My Numbers

scholesfan88

Posts: 265 Forumite

Hi

Need some help from those in the know, I've been to see a property today and would like to make an offer. However I'm now in meltdown over wether my numbers are correct and I'd be accepted for a mortgage.

House price £130k

Deposit £6.5k (95% LTV)

Income £37.5k

Debts (HP) £544 monthly

Debts (CC) £380 but just paid £150 so takes it to £160 and will be cleared next month

Debts (BNPL) Very account £480 not due until next year

No dependants

Outgoings around £100 in fuel and £60 in car tax and insurance

Living with parents so no rent or utilities to pay

Most of my spare income has been spent on clothes, gadgets, crap apart from the last month where I've been saving hard and spent virtually nothing apart from necessities. Previous bank statements will look poor apart from this months. Deposit has come from what I've saved since last payday (£1300) and what I've accumulated over time.

I have 1 missed payment (2 months in a row) on a phone contract, was told no further billing and so cancelled DD. Provider then tried charging for a final bill, hence the missed payment. This was paid off as soon as they sent a letter asking for it and was settled March 2016.

Affordability calculators seem to vary wildly. Some saying I can borrow up to £160k, others saying as little as £44k.

Help!

SF

Need some help from those in the know, I've been to see a property today and would like to make an offer. However I'm now in meltdown over wether my numbers are correct and I'd be accepted for a mortgage.

House price £130k

Deposit £6.5k (95% LTV)

Income £37.5k

Debts (HP) £544 monthly

Debts (CC) £380 but just paid £150 so takes it to £160 and will be cleared next month

Debts (BNPL) Very account £480 not due until next year

No dependants

Outgoings around £100 in fuel and £60 in car tax and insurance

Living with parents so no rent or utilities to pay

Most of my spare income has been spent on clothes, gadgets, crap apart from the last month where I've been saving hard and spent virtually nothing apart from necessities. Previous bank statements will look poor apart from this months. Deposit has come from what I've saved since last payday (£1300) and what I've accumulated over time.

I have 1 missed payment (2 months in a row) on a phone contract, was told no further billing and so cancelled DD. Provider then tried charging for a final bill, hence the missed payment. This was paid off as soon as they sent a letter asking for it and was settled March 2016.

Affordability calculators seem to vary wildly. Some saying I can borrow up to £160k, others saying as little as £44k.

Help!

SF

0

Comments

-

That seems a bit tight, generally you can lend x4.5 your income without debt, I hope you have some extra money for solicitors fees, moving costs e.t.c

Get a broker to see what they can do for you"It is prudent when shopping for something important, not to limit yourself to Pound land/Estate Agents"

G_M/ Bowlhead99 RIP0 -

Thanks for coming back to me.

Total debt stands at £22k which is car finance mainly.

I get paid in 2 weeks which will cover the legal fees and moving fees are minimal as this is my first house.

Officially down as living with parents however I'm in a serviced apartment paid for by my works Mon-Fri due to working away on secondment.0 -

Credit cards usually go off the balance and loans the repayments when assessing affordability.

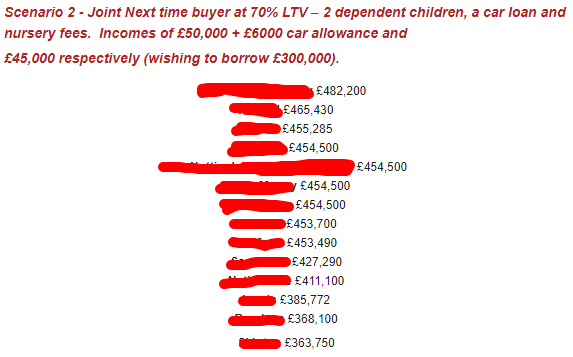

Affordability calculators can vary massively, here is an example of how the loan amounts can vary for the same person, £120k difference for the same case.

It sounds feasible. You may find some lenders will decline you outright because of the amount of debt but I would expect you to get a mortgage through at normal rates.I am a Mortgage AdviserYou should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.0 -

I’m similar in terms of mortgage required vs earnings/debts, except monthly outgoings. I had enough for 10% deposit but broker advised paying off debts with it to free up affordability.

The least outgoings you can go into it with will help as far as I understand.

Good luck.0 -

Thank you ACG, that's reassuring.

I've just booked an appointment with a local broker to sort it out. I'm usually reluctant to pay fee's for things like this however the broker states he's only charged a fee twice this year and if one applies then it's £295. In the grand scheme of things, I can live with that.0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards