We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Cabot Financial in behalf or Merlin Europe

Comments

-

Looked again through all paperwork including credit file.

Facts:

1. they're claiming the original debt as with Barclays Finance for £1,111.68 for £30.88/month taken in January 2008.

2. they're claiming the outstanding balance is £706.22

3. that would mean the total amount paid before defaulting was £405.46, divided by £30.88/month = 13 months paid.

4. 13 months from January 2008 would mean February 2009 is the month when the last payment was made.

5. let's assume no payment after that, 3 months later a default should have been recorded on the credit file, so that's May/June 2009.

What happened from June 2009 to October 2011? Shouldn't the default be registered sometime in 2009 rather than 2011, therefore shouldn't this be statute barred / removed from the credit file?

Am I wrong?

Not necessarily, as you don't seem to have included interest.

Using an online loan calculator, and trying some guesses at numbers, I found £30.88 per month fits a 48 month loan at 14.9%.

This won't be the only solution of course, but if it were those numbers then it takes 22 months to get the balance down to £704.78, and the interest is then about £8 a month.

So maybe payments were made for a big longer that that, down to a lower balance, then stopped, and they kept adding interest for a while.

Whatever it is, it sounds a bit like you still don't recognise it. Can there be mistaken identity somewhere?0 -

Over the phone I've been told the following:

Original amount £789 over 36 months starting 11 January 2008.

APR @ 19.9%

Total balance £1111.68

Outstanding balance £929.29 although the letter I had from then said £706.22!

That means £182.39 was paid, that's 6 months from January 2008!?0 -

OK, I misunderstood what you meant by the 1111.68, sounds like total repayments not the amount borrowed.0

-

No problem, so what I need next is a copy of the Default notice issued by Barclays Finance and Notice of Arrears so I can see how long they took to report the Default?0

-

Some further news, just called Barclays Partner Finance, they were closing at 8:00pm, so just in time.

I have confirmation that the last payment was made on November 2009 and it would have taken a maximum 6 months for them to issue the Default.

They will investigate the exact date when the default was registered and asked me to call again on Tuesday next week so they can advise.

Going by that, it looks like the Default should have been registered latest by May 2010 and not October 2011, which means this has should have disappeared from the file by now!0 -

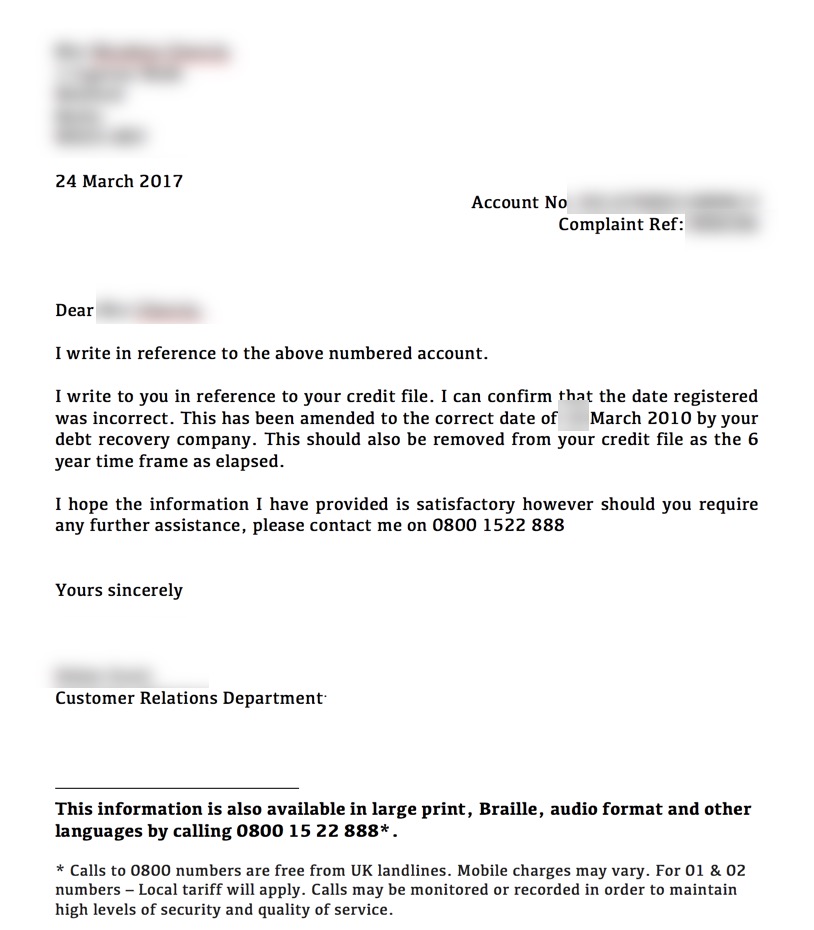

Update, Barclays Finance finally admitted they had the Default Notice wrong by 18 months!!!

Cabot is now updating the Credit File which means the default will be removed from the file.

Barclays is now asking me basically how much would I want to be paid not to file a complaint with FCA for not being able to get credit for all this time. They have asked for letters from the Mortgage Broker or Lenders to prove I was unable to get mortgage.

It took me one year to have this sorted, during which I was declined any mortgage offers from the high street lenders, causing me a lot of grief and stress...

Well, at least is done now! Thanks everyone for help and suggestions! :beer:0 -

Update, Barclays Finance finally admitted they had the Default Notice wrong by 18 months!!!

Cabot is now updating the Credit File which means the default will be removed from the file.

Barclays is now asking me basically how much would I want to be paid not to file a complaint with FCA for not being able to get credit for all this time. They have asked for letters from the Mortgage Broker or Lenders to prove I was unable to get mortgage.

It took me one year to have this sorted, during which I was declined any mortgage offers from the high street lenders, causing me a lot of grief and stress...

Well, at least is done now! Thanks everyone for help and suggestions! :beer:

Very well done.

I'd take them to the cleaners if it were me.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter0 -

Well, for now the thing is off your file, which in order of getting yourself a mortgage is the priority.Update, Barclays Finance finally admitted they had the Default Notice wrong by 18 months!!!

Cabot is now updating the Credit File which means the default will be removed from the file.

Barclays is now asking me basically how much would I want to be paid not to file a complaint with FCA for not being able to get credit for all this time. They have asked for letters from the Mortgage Broker or Lenders to prove I was unable to get mortgage.

It took me one year to have this sorted, during which I was declined any mortgage offers from the high street lenders, causing me a lot of grief and stress...

Well, at least is done now! Thanks everyone for help and suggestions! :beer:

Now, I'd be hammering them for this, and of course that you've had to go round the houses for a debt that isn't yours.

Good luck going forward and hopefully you can get your mortgage stuff sorted now!

P.S: As I provided financial advice (lol), my fee is 30% of any compensation received. If this isn't paid within 30 nanoseconds of receipt of said compensation I will register a default on your file and you still wont get a mortgage

In debt and looking for help? Look here for the MSE Debt Help Guide.

Also, If you need any free and impartial debt advice, the National Debtline, Stepchange, and the CAB can help.0 -

Thank you, all!

They've asked for a letter from either a lender or mortgage broker to explain the grief I had obtaining any mortgage deals. Even Barclays refused me with the default on!!!

What would you guys consider a fair/reasonable compensation?0 -

I'd work out:

a) The rent you paid while unable to get a mortgage

b) The equity you would have built up in the intervening time (e.g., if you were prevented from buying a house for a year, by what % did house prices rise in that year?)

c) Add up the time spent over that year applying for mortgages at 6.31/hour

d) Any lost opportunities during that time? Couldn't take advantage of a business opportunity, eg?

e) Any health/stress issues recorded?

Start there, anyway.MFW diary here. 1 Feb 2017 $229,371 - MFD Feb 2043 :eek: aiming for May 2028

14 August 2017 - Refinanced: $220,000

January 2019 $211,580 Current MFD 31 June 20360

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards