We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Debate House Prices

In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non MoneySaving matters are no longer permitted. This includes wider debates about general house prices, the economy and politics. As a result, we have taken the decision to keep this board permanently closed, but it remains viewable for users who may find some useful information in it. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Inter generational fairness

chiefie

Posts: 406 Forumite

Is it me, but.....,

I think the young of today do have a tough deal which was different to when I was 20 over 30 years ago. Defined benefit pensions are as rare now as honest politicians, tuition fees are ridiculously high, and the cost of housing (the price) is high.

But I got a degree but couldn't afford my first car till I was 23. I could only afford my first house with my wife at age 27 which was a stretch at 3 times my salary and 1 times hers. I paid mortgage rates around 11%. I got gazumped 3 times and ended up paying 50% more for my first house than I could have two years before. I sold nine years later and made zero profit.

All this stuff about us oldies leaving the young a pRoblem is nonsense to a degree. We did though allow governments to let big business get away with paying low taxes, stopping pensions and the like to ensure shareholders benefitted.

Rant over - just can see all this being used as an argument to means test the state pension (already called a benefit), to charge pensioners NI, to further devalue the remaining DB pensions in the name of fairness to others. It all seems a race to the bottom

I think the young of today do have a tough deal which was different to when I was 20 over 30 years ago. Defined benefit pensions are as rare now as honest politicians, tuition fees are ridiculously high, and the cost of housing (the price) is high.

But I got a degree but couldn't afford my first car till I was 23. I could only afford my first house with my wife at age 27 which was a stretch at 3 times my salary and 1 times hers. I paid mortgage rates around 11%. I got gazumped 3 times and ended up paying 50% more for my first house than I could have two years before. I sold nine years later and made zero profit.

All this stuff about us oldies leaving the young a pRoblem is nonsense to a degree. We did though allow governments to let big business get away with paying low taxes, stopping pensions and the like to ensure shareholders benefitted.

Rant over - just can see all this being used as an argument to means test the state pension (already called a benefit), to charge pensioners NI, to further devalue the remaining DB pensions in the name of fairness to others. It all seems a race to the bottom

0

Comments

-

What race to the bottom everyone has access to much more of everything at all points in life, the big change has been that life itself has shifted by about 10 years as kids stay 'kids' for longer.

We are also in a period of low-ish productivity growth as the last 10 years has brought us a lot of technology but not so much in big productive technology leaps. For instance broadband is a lot faster smartphones exist now etc but they have not improved productivity a huge amount.

I think the period 2020-2040 is going to be a golden time as technology kicks in with huge productive leaps as software becomes human level or better capable at specific tasks. Possibly the first big one will be software driven vehicles. The government will tax these productivity leaps very heavily and distribute to the masses via tax cuts, more benefits and higher state spending.0 -

Currently, the average age of a first time buyer in the UK is 30, or 32 in London. Source. People simply can't afford to buy earlier than that because they need to have hefty deposits and find it tough to save big deposits while paying high rents.I could only afford my first house with my wife at age 27

This actually sounds quite low to me. Most first time buyers take out a mortgage at 4x salary (which is about the maximum lenders will allow these days. It used to be 6x before the financial crash).which was a stretch at 3 times my salary and 1 times hers.

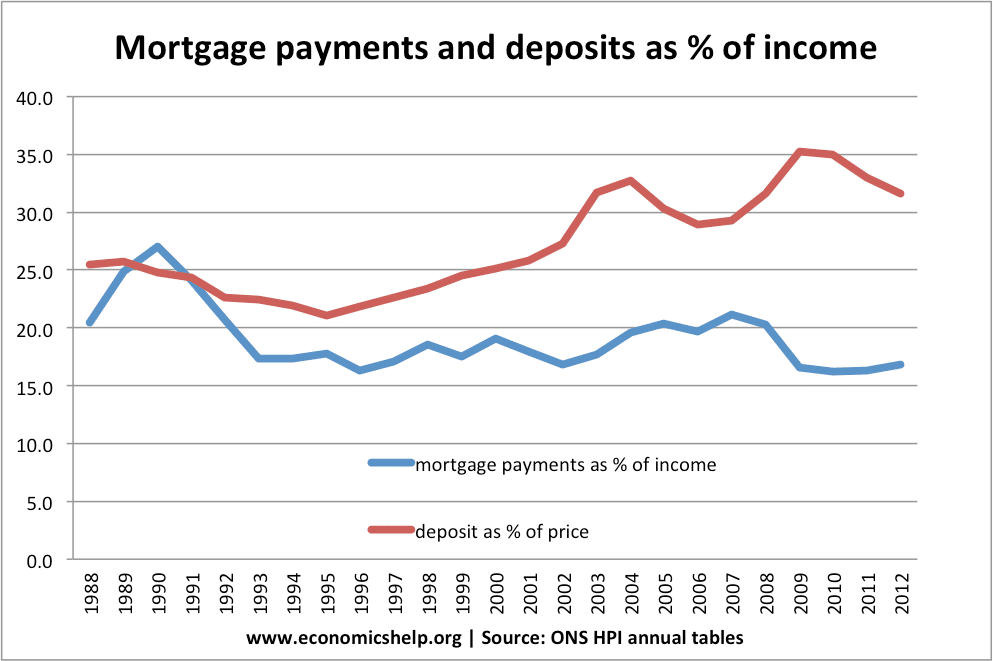

This is a fair point. Average mortgage payments as a % of income today are broadly consistent with what you paid. Much higher house prices but much lower interest rates. Here's a graph.I paid mortgage rates around 11%.

What do you think a pension is? By far the largest group of shareholders is pension funds.All this stuff about us oldies leaving the young a pRoblem is nonsense to a degree. We did though allow governments to let big business get away with paying low taxes, stopping pensions and the like to ensure shareholders benefitted.0 -

steampowered wrote: »Currently, the average age of a first time buyer in the UK is 30, or 32 in London. Source. People simply can't afford to buy earlier than that because they need to have hefty deposits and find it tough to save big deposits while paying high rents.

But they spend more time at University, often take gap years.

There is also a tendency not to save as quickly. There are many temptations to spend discretionary income. For example, I know an 23 year old who has just replaced a 2 year old iPhone with the latest model. Even though I can afford it I do not buy iphones and my Samsung is now 5 years old but does me fine. The old expression: you cannot have your cake and eat it.

3 times salary was the norm in 1980 also in those days.This actually sounds quite low to me. Most first time buyers take out a mortgage at 4x salary (which is about the maximum lenders will allow these days. It used to be 6x before the financial crash).What do you think a pension is? By far the largest group of shareholders is pension funds.

What he meant is that the decisions on the affordability of DB pensions and their phasing out were made for business reasons, effectively to reduce worker pay at the expense of more profits for shareholders. Some blame Gordon Brown for removing tax relief on dividends in the 1990s which was a factor or at least a good excuse for businesses. But the Government in the 1980s allowed firms to take holidays from paying their contributions into the company pension fund because of them being in surplus, 10 years later they said the pensions were unaffordable. In reality, pensions went because firms were unwilling to contribute and nobody thought it was worth protesting.

So what do you think a pension fund is? It is future pensioners deferred salary invested on their behalf by their representatives in the stock market, bonds or property.Few people are capable of expressing with equanimity opinions which differ from the prejudices of their social environment. Most people are incapable of forming such opinions.0 -

What race to the bottom everyone has access to much more of everything at all points in life, the big change has been that life itself has shifted by about 10 years as kids stay 'kids' for longer.

We are also in a period of low-ish productivity growth as the last 10 years has brought us a lot of technology but not so much in big productive technology leaps. For instance broadband is a lot faster smartphones exist now etc but they have not improved productivity a huge amount.

I think the period 2020-2040 is going to be a golden time as technology kicks in with huge productive leaps as software becomes human level or better capable at specific tasks. Possibly the first big one will be software driven vehicles. The government will tax these productivity leaps very heavily and distribute to the masses via tax cuts, more benefits and higher state spending.

Or the government will not deal with the tax loop holes for the international companies, unemployment goes up and tax goes up ? I don't have faith at the moment that the people who govern will think about society impact of change, only business. Thanks for the comments-interesting.0 -

I know a lot of people that have never had any sort of company pension and most Boomers didn't go to university either. House prices are the big difference, but where I live which is 20 mins from Chester and Liverpool, 30 form Manchester and 15 from Warrington, you can get a nice terrace for 75-80k, which niftily is about three times average salary. South East is a whole different ball game!0

-

Or the government will not deal with the tax loop holes for the international companies, unemployment goes up and tax goes up ?

UK unemployment falls to 11-year low

http://www.bbc.co.uk/news/business-37997713

What tax increases are you worried about?... I don't have faith at the moment that the people who govern will think about society impact of change, only business. Thanks for the comments-interesting.

What do you mean by "society impact of change"; what are you concerned about?0 -

blah blah "We lived on cardboard boxes in our first house"... "didn't have any iphones ect" ... "the youth of today spend all their money on rubbish"

Because people born post-war were so much more special than those born in the last 30 years? They were so much better at saving, and circumstances were exactly the same?

Honestly, people project such rubbish. We live in different economic times. Credit is far more available. Consumer/home inflation has continued whilst salaries have not inflated. There is a MASSIVE house price difference between the North and South of the country. There has been the death of the manufacturing industries.

I see that you've conveniently forgotten that your university education was free, but would now cost at least £27,000

Pensions are obviously a big problem. There is going to be a decreasingly poor ratio of pension receivers Vs pension pot payers. It's a pyramid scheme and it's going to topple unless people take less state pension. Pension *should* be means tested.

We're on a generational slide. The boomers had it better than their parents, but the children of boomers (and their children) are most likely not going to have it as good. It's the inevitable process of automation and globalisation. Sure we'll have cooler gadgets, but we'll loose out paying more for education, housing and pensions.0 -

I am sure this is a factor for some first time buyers, but university and gap years lasting until people are 30?But they spend more time at University, often take gap years.

The ONS figures available here are very interesting on this. You will see that home ownership is much lower than it was at 1981 at every age group until age 45. Youc an't explain that on the basis of university and gap years.

After age 45, home ownership is substantively higher than it was in 1981.

I don't think anyone in particular is to blame with this. I also don't think we could flick a magic switch by protesting. Pension schemes have changed because of changing demographics. In particular the fact that people are living so much longer than they used to.What he meant is that the decisions on the affordability of DB pensions and their phasing out were made for business reasons, effectively to reduce worker pay at the expense of more profits for shareholders. Some blame Gordon Brown for removing tax relief on dividends in the 1990s which was a factor or at least a good excuse for businesses. But the Government in the 1980s allowed firms to take holidays from paying their contributions into the company pension fund because of them being in surplus, 10 years later they said the pensions were unaffordable. In reality, pensions went because firms were unwilling to contribute and nobody thought it was worth protesting.

This isn't a bad thing and its not anyone's fault. It is just a fact of life that the country has to deal with when it structures pension schemes.

In defined benefit pension schemes, the employer/sponsor promises a specified payment determined by a formula depending on the employee's earning history and length of employment. The payment has nothing to do with investment returns.

This type of arrangement has become unsustainable because people are living longer. In order to keep a DB scheme running, you have a situation where you have the same number of employees paying into the scheme but an ever increasing number pensioners paid by the pension fund.

Here is the Worldbank's graph of the age dependency ratio in the UK. This is the ratio of retired people to working age people. You will see it has increased from 18% in 1960 to 27% today. That's a 50% increase. On that basis alone, DB scheme contributions would need to be 50% higher to fund the same level of retirement benefits.

That is how a modern defined contribution scheme works. That is not how a defined benefit scheme works.So what do you think a pension fund is? It is future pensioners deferred salary invested on their behalf by their representatives in the stock market, bonds or property.

The payments made to pensioners in a DB scheme is not linked to investment returns. That is why DB schemes end up with deficits - because their investment returns are not sufficient to maintain payments to pensioners.

The point I was making is that pension funds are by far the largest groups of shareholders of UK companies. So if something benefits company shareholders it in effect benefits pension funds.0 -

Is it me, but.....,

I think the young of today do have a tough deal which was different to when I was 20 over 30 years ago. Defined benefit pensions are as rare now as honest politicians, tuition fees are ridiculously high, and the cost of housing (the price) is high.

But I got a degree but couldn't afford my first car till I was 23. I could only afford my first house with my wife at age 27 which was a stretch at 3 times my salary and 1 times hers. I paid mortgage rates around 11%. I got gazumped 3 times and ended up paying 50% more for my first house than I could have two years before. I sold nine years later and made zero profit.

All this stuff about us oldies leaving the young a pRoblem is nonsense to a degree. We did though allow governments to let big business get away with paying low taxes, stopping pensions and the like to ensure shareholders benefitted.

Rant over - just can see all this being used as an argument to means test the state pension (already called a benefit), to charge pensioners NI, to further devalue the remaining DB pensions in the name of fairness to others. It all seems a race to the bottom

Its a good discussion. You seem concerned about pensions and probably rightly so.

I dont think there is trully an issue with different age groups in terms of outlooks its just the world isnt what it was 30 years ago. People always defend what they hold dear, youve bee n told all your life you will be looked after in retirment (like me) and its becoming less and less likely every day. Youre rightly annoyed. However your annoyance, i believe, is misguided. The discussion is generally played out among the young v old. You had this we had that. Ultimately though we have and we are all still being lied to. It baffles me that we have some of the worlds greatest number people yet cant work out what basically comes down to a simple budget. A country of bankers are unable to deliver anything vaguely like an accurate cash flow forecast.

Ultimately it is a race to the bottom as we bicker among ourselves trying to hold on to any shred of benefit we're entitled to.Toute nation a le gouvernement qu'elle m!rite.

The plebs are arguing for their cut whilst overlooking the fundamental issue in that we are terribly managed and the complete lack of responsibility that slopes off the shoulders of parliament.0 -

ringo_24601 wrote: »We're on a generational slide. The boomers had it better than their parents, but the children of boomers (and their children) are most likely not going to have it as good. It's the inevitable process of automation and globalisation. Sure we'll have cooler gadgets, but we'll loose out paying more for education, housing and pensions.

House prices have risen faster than wages in certain areas. Lower interest rates mean the monthly payments may still appear affordable, but wanting to pay off your mortgage early is much harder and getting the deposit is much harder. "Luckily" there are still enough rich buyers around to keep the prices high but those on lower salaries struggle.

However, boomers are going to be dying out soon while there is a good chance that those still alive in the next 10-50 years will benefit from some truly mind blowing technology and potentially even significant anti-aging or age-reverseal. People are also becoming more liberal and tolerant so the world is (with some ups and downs) becoming a nicer place to live.

Put simply, offered a choice between being a boomer and being a 20 something year old looking to start out their adult life now, I'd choose the latter every time.0

{kind=link}

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.1K Reduce Debt & Boost Income

- 455K Spending & Discounts

- 246.5K Work, Benefits & Business

- 602.8K Mortgages, Homes & Bills

- 178K Life & Family

- 260.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards