We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Debate House Prices

In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non MoneySaving matters are no longer permitted. This includes wider debates about general house prices, the economy and politics. As a result, we have taken the decision to keep this board permanently closed, but it remains viewable for users who may find some useful information in it. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Baffling London BTL economics

Comments

-

chucknorris wrote: »So you are ignoring inflation, inflation plays its part, it isn't wise to rely upon it, but it should not be ignored either, it has actually literally made me quite a lot of money.

Inflation has nothing to do with house prices. House prices don't track inflation at all, they are even specifically excluded from the inflation figures. That is why I have a separate figure for HPI and one for general inflation (maintenance costs) and one for rent inflation. It's all there in the spreadsheet.

I really don't understand why you continue to have a go at me when it is the original poster, a known BTLer and generally housing bull who said the purchase makes no sense from an investment view because the buyer overpaid and prices are softening. Can you take it up with him rather? Tell him he is being stupid because "inflation" will mean he is wrong?Edit: How much did your spreadsheet make you in the last tax year, that is the ultimate test, everything else is just !!!!!!!!, I don't mean that nastily, it just happens to be true. My spreadsheets make me money, that is why I spend time on them, time is money.

*sigh*

I constructed the example to illustrate the point being made by the original poster. But as usual you guys can't resist.

Woof woof.0 -

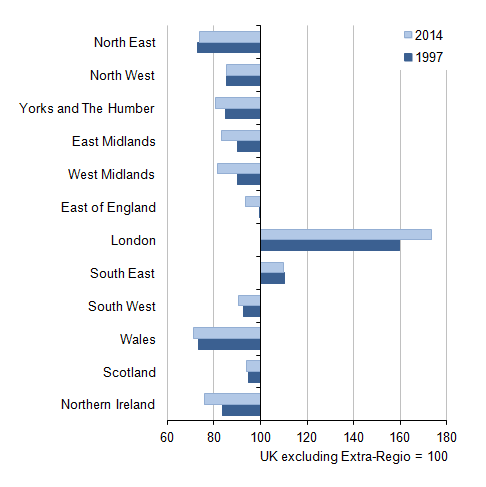

1: Profit is king, Cashflow is God, regional GVA is Zeus!

Over the last 20 years London has growth its GVA more than rUK which goes a LONG way to explain why London prices have gone up more than rUK and it also explains why some areas like stoke or Middlesbrough have gone nowhere for 10 years

So for example in 2014 London GVA grew by +5.3% whereas the UK excluding London was closer to +2.5%. That dear readers is a HUGE massive economy changing difference! If sustain over periods of 20-30 years it will completely change the fortunes of a region. That is pretty much what happened over the last 20 years with London growing faster than rUK London got rich and houses got expensive.

I dont see why the same wont happen again over the next 20-30 years. London is geared to benefit from future growth in a way stoke on trent isnt.0 -

If I were modelling house prices I would try to take this into account.

If over the next 20 years you expect inflation to be 2% a year,

UK nominal GVA growth to be 4% a year

Then you might take London nominal GVA growth to be 5% a year.

That might seem insignificant but if the uk is growing just a real 2% a year while London is growing at 3% then compounded over a 25 year period its going to have a large impact.

So I would expect London house prices to diverge another ~30% above rEngland prices over the next 25 years simply on the basis that GVA growth in London will be about 30% higher than rEngland.

Of course the exact numbers are up for debate I just used a round 1% higher growth. If someone takes 0.5% or 1.5% instead of 1% it makes quite a big difference. One could also make the case that all this is baked into current prices but I dont think so0 -

chucknorris wrote: »So you are ignoring inflation, inflation plays its part, it isn't wise to rely upon it, but it should not be ignored either, it has actually literally made me quite a lot of money.

Inflation should not be ignored it gives a good estimate of possible uplift. Of course house prices can overshoot inflation (London) or undershoot them (North)

Over a 30 year period with an assumption of inflation at 2.5% (the midpoint of the BOE target of 2-3%) prices of a basket of goods would be 2.1 x what they are now.

It is unlikely that house prices will stay flat while general prices double and possibly wages almost tripling0 -

mwpt

your sheets link misses a few things.

Your profits should either be paying down the debt or they should be accumulating interest themselves. (or if making a loss, the opposite)

that will also change your 'overall yield' which you should change to 'overall annual return'

Finally you should do a NPV of the cash invested, NPV compared to 30 year gilts, NPV of the total return on the property. All post tax0 -

Inflation has nothing to do with house prices. House prices don't track inflation at all, they are even specifically excluded from the inflation figures. That is why I have a separate figure for HPI and one for general inflation (maintenance costs) and one for rent inflation. It's all there in the spreadsheet.

I really don't understand why you continue to have a go at me when it is the original poster, a known BTLer and generally housing bull who said the purchase makes no sense from an investment view because the buyer overpaid and prices are softening. Can you take it up with him rather? Tell him he is being stupid because "inflation" will mean he is wrong?

*sigh*

I constructed the example to illustrate the point being made by the original poster. But as usual you guys can't resist.

Woof woof.

Where is all this 'having a go at me' and 'tell him he is stupid' coming from? You are being far too touchy, I'm not having a go at you at all.

I have made my thoughts quite clear on the subject of investment property several times since the tax changes were announced. I don't think buying an investment property (with a significant mortgage) is as good an investment choice as shares is, for a higher rate tax payer because:

1. It takes a quite a few years to reach decent profitability, that could change if rents rise significantly, but I wouldn't want to rely upon that. I'm not saying that it won't happen, I just wouldn't want to rely upon it.

2. The new £5k tax free allowance for dividend income (£10k for a couple) is a significant tax advantage when you compare it to the tax treatment of investment property. This is more significant to someone who is only going to buy one or two properties. Obviously if you are talking about investing £m's then that tax free allowance pales into insignificance.

3. Shares don't come with the same hassle that property can give you.

4. It is much easier to avoid CGT with shares than with property, due to the iliquidity of property.

5. You can't put residential property in an ISA or SIPP.

As for what you said about inflation having nothing to do with house prices, of course it does, but in a general rather than specific way. By that I mean you obviously can't point at RPI or CPI and apply it to house prices, but over time inflation will have an affect on house prices, as peoples earnings rise.

Just to emphasise the point I am not having a go at you, I just don't think property is a particularly good investment now, shares look a much better investment to me.Chuck Norris can kill two stones with one birdThe only time Chuck Norris was wrong was when he thought he had made a mistakeChuck Norris puts the "laughter" in "manslaughter".I've started running again, after several injuries had forced me to stop0 -

mwpt

your sheets link misses a few things.

Your profits should either be paying down the debt or they should be accumulating interest themselves. (or if making a loss, the opposite)

The latter doesn't reveal the yield on the BTL investment correctly because now we have another variable component completely unrelated to the BTL. But point taken about the former, I will adjust the sheet to pay down the debt.that will also change your 'overall yield' which you should change to 'overall annual return'

Well, it is named overall yield for a reason") See above.Finally you should do a NPV of the cash invested, NPV compared to 30 year gilts, NPV of the total return on the property. All post tax

See above.Finally you should do a NPV of the cash invested, NPV compared to 30 year gilts, NPV of the total return on the property. All post tax

I can add that but it isn't strictly necessary to make a judgement about the returns on the BTL investment. Useful though nonetheless.0 -

chucknorris wrote: »As for what you said about inflation having nothing to do with house prices, of course it does, but in a general rather than specific way. By that I mean you obviously can't point at RPI or CPI and apply it to house prices, but over time inflation will have an affect on house prices, as peoples earnings rise.

I have a separate variable, called HPI to account for this. The reason I did it like that is because HPI bears almost no relation to general inflation, hasn't for quite some time, so you have to have a separate variable.

You can adjust it as you see fit in the spreadsheet, perhaps a good value going forward for London averaged over 15 years would be say, 2 or 3%?

Btw, London HPI has exceeded wage growth and general inflation for decades, and this is mathematically unsustainable. Would it be a real surprise if certain areas flatlined or mildly declined over the next 5-10 years? I certainly would not be surprised. In fact, I'd say it is fairly likely but only in certain areas. So if I can put zero % HPI into a spreadsheet and the property still earns me a decent positive yield, that is a fairly good buy signal.Just to emphasise the point I am not having a go at you, I just don't think property is a particularly good investment now, shares look a much better investment to me.

I won't be investing in property but thanks for giving your thoughts. I'll pass this on to my brother. I suspect that BTL right now requires a bit more nuance and being close to the action, getting the good deals through connections with EAs. He lives abroad, he isn't going to be able to do that.0 -

I have a separate variable, called HPI to account for this. The reason I did it like that is because HPI bears almost no relation to general inflation, hasn't for quite some time, so you have to have a separate variable.

You can adjust it as you see fit in the spreadsheet, perhaps a good value going forward for London averaged over 15 years would be say, 2 or 3%?

Btw, London HPI has exceeded wage growth and general inflation for decades, and this is mathematically unsustainable. Would it be a real surprise if certain areas flatlined or mildly declined over the next 5-10 years? I certainly would not be surprised. In fact, I'd say it is fairly likely but only in certain areas. So if I can put zero % HPI into a spreadsheet and the property still earns me a decent positive yield, that is a fairly good buy signal.

I won't be investing in property but thanks for giving your thoughts. I'll pass this on to my brother. I suspect that BTL right now requires a bit more nuance and being close to the action, getting the good deals through connections with EAs. He lives abroad, he isn't going to be able to do that.

I'm very pleased where London property is right now, it has exceeded my hopes in the last few years, and I wasn't expecting to see the current values for years. I'd be very happy if it just stagnated for a few years until I sell, the reason that I am staying in for a few years (2-4?) is for the income, rather than for any hope of further capital growth.

I would add though that if I did end up on the Isle of Man, I might end up buying an investment property or two there, because;

-there is no GCT

-there is no stamp duty

-Corporation tax for property companies is only 10%

-dividends from IOM companies are tax free

That would depend on whet the market is like of course, but moving to the IOM is no more than a thought at the moment.Chuck Norris can kill two stones with one birdThe only time Chuck Norris was wrong was when he thought he had made a mistakeChuck Norris puts the "laughter" in "manslaughter".I've started running again, after several injuries had forced me to stop0 -

All of that is taken account for in the spreadsheet. The final column, which shows the yield, calculates it off only your initial investment which is the 30% deposit sum plus all fees. And if you copy or duplicate a sheet and play around with HPI, setting it at even say a moderate 1-2% instead of zero, you'll see if makes an enormous difference, as you'd expect when using leverage.

I am somewhat offended that you think I'm stupid

EDIT: And I'm not ignoring inflation. I set the HPI at zero for a reason, to see what happens if nominal prices don't rise for a significant amount of time. And once again, the sheet is editable if you copy the tab and create your own scenario to show your estimates for HPI, etc.

EDIT2: And I wanted to see what happens with nominal prices not rising for a good reason, because the OP said the buyer overpaid and that prices were softening in that area.

I've run a reasonably similar retirement spreadsheet where, 20 years ago, I made assumptions about what 40 years from there would look like. As you can imagine life doesn't work in a straight line like a spreadsheet and all of the assumptions were wrong to a greater or lesser degree.

The advantage I have is 20 of those 40 years have passed and the spreadsheet has been updated accordingly and I now only need to make assumptions for 20 years hence. The same will happen with your spreadsheet - at the end of year one it can be updated with real numbers and future assumptions finessed.

I'm more interested in how you'd use the model to decide whether to buy a BTL. I see my retirement spreadsheet as a pension tracker as much as a forecasting tool.

Take the Bristol example for your brother - what is it that's going to make the difference between a yes and a no? I know if it was me I'd want to take a view on the long term but would be far more interested in the performance over the first 5 years or so.

So is Bristol a buy or not? Does it have to work over 30 years with inflation at 1.5% and HPI at 0%?0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 352.7K Banking & Borrowing

- 253.8K Reduce Debt & Boost Income

- 454.6K Spending & Discounts

- 245.8K Work, Benefits & Business

- 601.8K Mortgages, Homes & Bills

- 177.7K Life & Family

- 259.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 15.9K Discuss & Feedback

- 37.7K Read-Only Boards