We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Second Property Investments

Comments

-

I am hoping to retire in about 9 years time and BTL is one option I am looking at to help fund this.

You need to do your research and I am not professing to be an expert, so I am willing to listen to other people's experiences and learn from them.

But I know by looking around, knowing the property and rental markets, you can significantly increase your returns.

For example, it's possible to buy a tidy terraced house about 15 miles from where I live for around £40k - by tidy I mean it wouldn't need "doing up" before a tenant could move in. Rents for that type of property are currently around the £400 a month mark, so a gross return of 12%

You can probably beat that by looking at flats, or in other parts of the country.

Compare that to an annuity, I can get at best 3%.

Obviously the annuity is guaranteed but property isn't exactly a huge risk - if you can spread the risk over multiple properties you mitigate against bad tenants etc.

Another option is peer to peer lending, I heard a radio programme recently where a chap was getting 9% returns net so that's worth a look, unfortunately I didn't catch which website he was using but it was lending to businesses.

edit -it's Funding Circle - https://www.fundingcircle.com/uk/

My step-father owns about 20 properties that he rents out and manages himself, renting to DSS etc and he doesn't have a huge amount of problems but does generate enough income to support quite a nice lifestyle. But yes, he does have the odd bad tenant.

Anyway, good luck!Make £2018 in 2018 Challenge - Total to date £2,1080 -

scaredofdebt wrote: »For example, it's possible to buy a tidy terraced house about 15 miles from where I live for around £40k - by tidy I mean it wouldn't need "doing up" before a tenant could move in. Rents for that type of property are currently around the £400 a month mark, so a gross return of 12%

That kind of property is appealing because if bought mortgage free - it would be hard to lose any money over 30+ years via rent and/or selling. The rent without increase would be nearly £150k, if you had no gaps, but even with gaps and some increases over 3 decades, the amount is likely to be useful.

I did look into peer-to-peer lending a while back - seems like a fairly good one although it seems quite new (or maybe I just had not heard of it until recent years).To err is human, but it is against company policy.0 -

greenglide wrote: »Will the current lunacy in London property prices continue - it cannot go on for ever!

People have been saying that for decades - and it still continues. I am not sure how and I am amazed that the situation has been sustainable this long.0 -

People have been saying that for decades - and it still continues. I am not sure how and I am amazed that the situation has been sustainable this long.

Property is a financial asset that produces an income which (adjusted for inflation and acknowledging some growth) is generally quite stable.

Like any other financial asset, the price of the asset, divided by the income, is equal to the yield.

The yields on all financial assets get compared to each other, and ultimately the interest rate managed by the central bank.

If the income is stable, and the yield goes down, the price goes up.

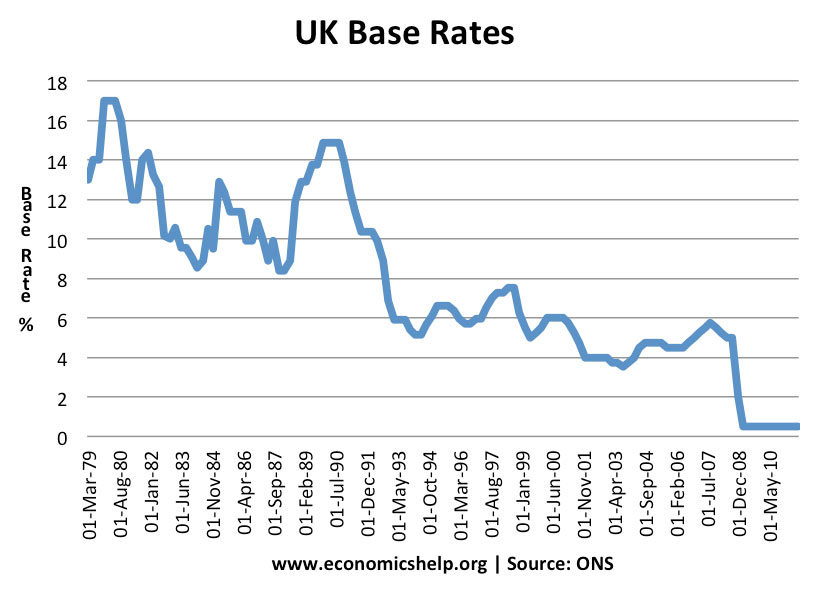

Take a look at what has happened to interest rates in this country over the very same decades you talk about.

That is how, and why the situation has persisted for so long.

Worth noting that the one slump in house prices we did have, in the early 90s, coincides with the only serious rise in interest rates. 0

0 -

princeofpounds wrote: »Property is a financial asset that produces an income which (adjusted for inflation and acknowledging some growth) is generally quite stable.

Like any other financial asset, the price of the asset, divided by the income, is equal to the yield.

The yields on all financial assets get compared to each other, and ultimately the interest rate managed by the central bank.

If the income is stable, and the yield goes down, the price goes up.

Take a look at what has happened to interest rates in this country over the very same decades you talk about.

That is how, and why the situation has persisted for so long.

Worth noting that the one slump in house prices we did have, in the early 90s, coincides with the only serious rise in interest rates.

That would suggest that the majority of London properties are purchased as investments and not as a personal abode. Also that the rental market can stand the increase costs that the Landlords would need if the cost of investment in the asset is increasing.

It still amazes me that the property costs (and rents) can still increase in the way that they have. Surely there must be a ceiling. Even the cost of renting must reach the point where is it not affordable and this will put the brakes on the situation.

But everything still marches upward. As I stated in an earlier thread this is one of the primary reasons why my place is being rented. In my circumstances the yield is not great but if I sold it we would never be able to return to the area in future as other savings would not keep pace with property prices at the rate they are currently increasing.0 -

Samsonite1 wrote: »Hello,

Does anyone think that aiming to buy a second property (and rent out) will become a bad idea for future finances? It would be great if they did not persecute a 2nd home as an investment, but only further homes...

S

I'm not sure why you think 2nd homes should be exempt?

Where does that stop? 3rd, 4th?

I understand your point but 2nd homes have to be an investment or a luxury for some!

In terms of risk, I do think people are being swayed by this. Daily Mail headlines such as property prices up 10% have people rushing to rightmove. If only it was that easy.

I rented out a 2nd house for a few years having moved. While I did not have any tenant problems, there is always the potential for bad payers, major maintenance etc. It does not take much to eat into a whole years rent.

When I decided to sell it was on the market for two years before I finally got rid. While I did not lose on the overall thing, I ended up selling the house at a bit of a knock down price to be finished with it.

It did not whet my appetite to go into it as a means of long term investment. That said, there are many who are doing very well with btl.0 -

I'm not sure why you think 2nd homes should be exempt?

Where does that stop? 3rd, 4th?

I understand your point but 2nd homes have to be an investment or a luxury for some!

In terms of risk, I do think people are being swayed by this. Daily Mail headlines such as property prices up 10% have people rushing to rightmove. If only it was that easy.

I rented out a 2nd house for a few years having moved. While I did not have any tenant problems, there is always the potential for bad payers, major maintenance etc. It does not take much to eat into a whole years rent.

When I decided to sell it was on the market for two years before I finally got rid. While I did not lose on the overall thing, I ended up selling the house at a bit of a knock down price to be finished with it.

It did not whet my appetite to go into it as a means of long term investment. That said, there are many who are doing very well with btl.

My logic (which is probably massively flawed) is that if you own two houses and live in one, you are not really setting up for a property business. As soon as you rent out 2 or more properties, you are creating a business.

What does the government want people to do with surplus income? I guess the only option which avoids being berated is to throw it at a pension, but then you can avoid paying loads of tax so the country is worse off as a whole. What is more selfish: property investment with lots of taxes paid or big pensions and little tax paid?To err is human, but it is against company policy.0 -

Samsonite1 wrote: »My logic (which is probably massively flawed) is that if you own two houses and live in one, you are not really setting up for a property business. As soon as you rent out 2 or more properties, you are creating a business.

I get your idea but its a little light on substance")

If you start a knitting operation selling wooly jumpers then you are creating a business and as such Mr Taxman is on your trail.Samsonite1 wrote: »What does the government want people to do with surplus income? I guess the only option which avoids being berated is to throw it at a pension, but then you can avoid paying loads of tax so the country is worse off as a whole. What is more selfish: property investment with lots of taxes paid or big pensions and little tax paid?

I would be less worried about what the government wants you to do with your surplus income - but they do want you save it for future prosperity, and to spend it, otherwise no economy. You need to work out whats best for you and not the government.

Putting it into pension will get be tax efficient. That versus btl is then a risk. Depending on your pension type, it may be at the risk of the markets. Equally your property is at risk of house price slump, which nobody thought could happen until the 1980's when many people heard of negative equity for the first time.0 -

Well exactly - I want to use both pensions and property. The property side of things - we are looking to be mortgage free as soon as possible and are overpaying as much as we can, we have increased our pensions and getting a second property with no mortgage (or a tiny one) would be the target. Once we are completely mortgage free, the plan would be to increase the pension contributions as much as possible.

One aspect is that - even if you are a high earner, your situation could change next year or in 5, 10 years etc. If you have some money in property, at least you can get at it potentially more easily before you retire if you lose your high income. If it was all in your pension, you might be in trouble?To err is human, but it is against company policy.0 -

I don't believe anyone here is telling do "definitely don't do it" you are being told that you are taking a risk as we do with all things.

If you are truly happy to take this risk on a single property and you are prepared to treat it as an investment and you become a landlord with all that entails, then fine.

If you have any doubts whatsever or you will be tying up a huge part of you wealth in this single property then tread very carefully.

You need to ensure you have enough of your wealth in other investments as well, pensions, s&s ISAs etc.

You will only be priced out of the London property market if London property prices for the properties you would want to buy in future continue to increase by more than inflation and other investments. They may do, they may not.0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards