We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

MSE News: Payday loan cost cap confirmed by FCA

Former_MSE_Paloma

Posts: 531 Forumite

in Loans

People taking out payday loans will never have to pay back more than double what they originally borrowed, the FCA says...

Read the full story:

Payday loan cost cap confirmed by FCA

Click reply below to discuss. If you haven’t already, join the forum to reply. If you aren’t sure how it all works, read our New to Forum? Intro Guide.

Payday loan cost cap confirmed by FCA

Click reply below to discuss. If you haven’t already, join the forum to reply. If you aren’t sure how it all works, read our New to Forum? Intro Guide.

0

Comments

-

Press release: http://www.fca.org.uk/news/fca-confirms-price-cap-rules-for-payday-lendersPeople using payday lenders and other providers of high-cost short-term credit will see the cost of borrowing fall and will never have to pay back more than double what they originally borrowed, the Financial Conduct Authority (FCA) confirmed today.

Martin Wheatley, the FCA's chief executive officer, said:

'I am confident that the new rules strike the right balance for firms and consumers. If the price cap was any lower, then we risk not having a viable market, any higher and there would not be adequate protection for borrowers.

'For people who struggle to repay, we believe the new rules will put an end to spiralling payday debts. For most of the borrowers who do pay back their loans on time, the cap on fees and charges represents substantial protections.'

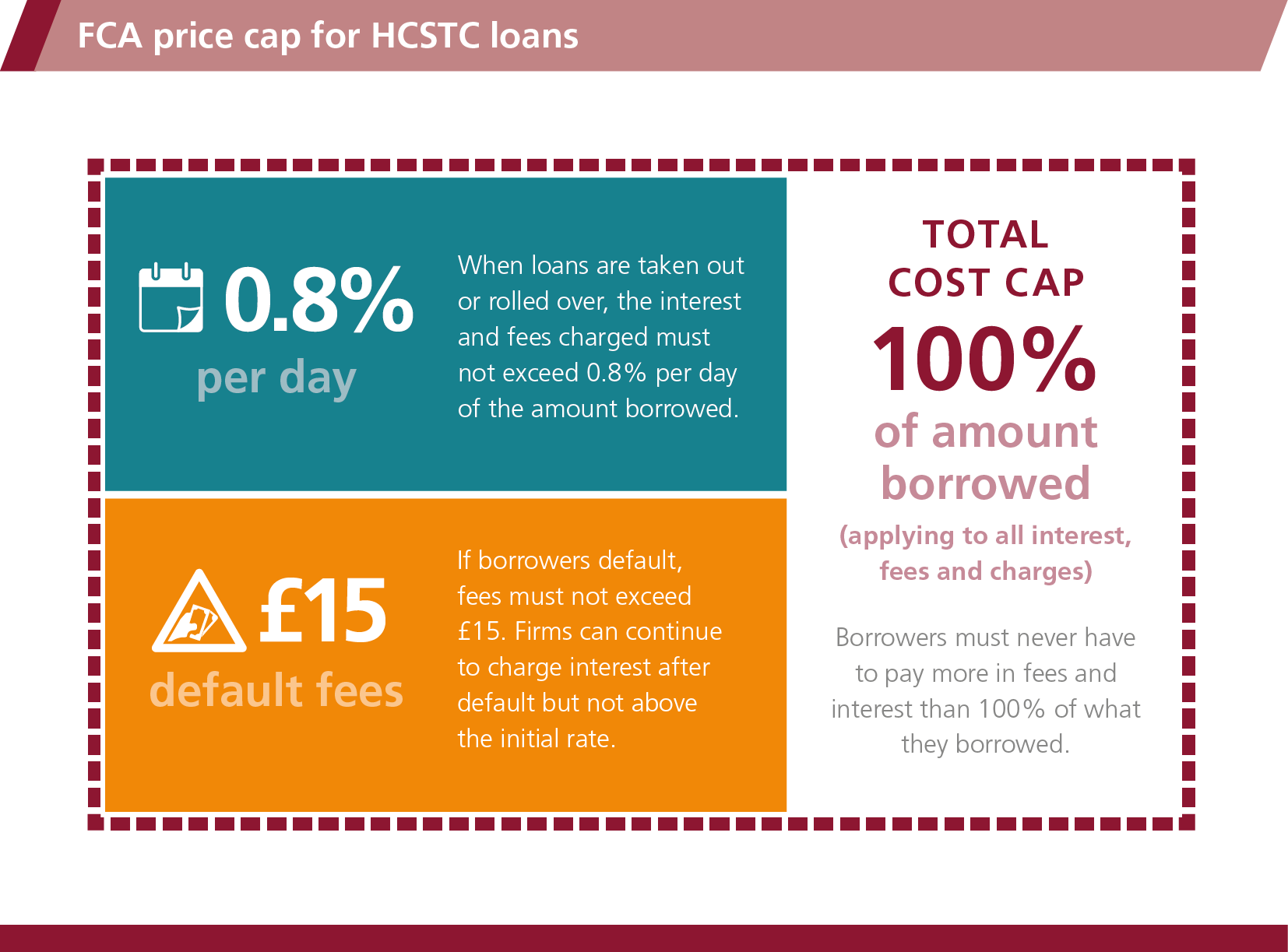

The FCA published its proposals for a payday loan price cap in July. The price cap structure and levels remain unchanged following the consultation. These are:- Initial cost cap of 0.8% per day - Lowers the cost for most borrowers. For all high-cost short-term credit loans, interest and fees must not exceed 0.8% per day of the amount borrowed.

- Fixed default fees capped at £15 - Protects borrowers struggling to repay.If borrowers do not repay their loans on time, default charges must not exceed £15. Interest on unpaid balances and default charges must not exceed the initial rate.

- Total cost cap of 100% - Protects borrowers from escalating debts.Borrowers must never have to pay back more in fees and interest than the amount borrowed.

Price cap consultation, further analysis

The FCA consulted widely on the proposed price cap with various stakeholders, including industry and consumer groups, professional bodies and academics.

In July, the FCA estimated that the effect of the price cap would be that 11% of current borrowers would no longer have access to payday loans after 2 January 2015.

In the first five months of FCA regulation of consumer credit, the number of loans and the amount borrowed has dropped by 35%. To take account of this, FCA has collected additional information from firms and revised its estimates of the impact on market exit and loss of access to credit. We now estimate 7 % of current borrowers may not have access to payday loans - some 70,000 people. These are people who are likely to have been in a worse situation if they had been granted a loan. So the price cap protects them.

In the July consultation paper the FCA said it expected to see more than 90% of firms participating in real-time data sharing. Recent progress means that participation in real-time data sharing is in line with our expectations. Therefore the FCA is not proposing to consult on rules about this at this time. The progress made will be kept under review.

The final policy statement and rules. The price cap will be reviewed in 2017.

Notes to editors- Price cap on high-cost short-term credit: Policy Statement 14/16

Proposals consulted on: position unchanged

The cap will have three components: an initial cost cap; a cap on default fees and interest; and a total cost cap.

- The initial cost cap will be set at 0.8% of the outstanding principal per day, on all interest and fees charged during the loan and when refinancing.

- Firms can structure their charges under this cap in any way they choose, for example, a portion could be upfront or rollover fees.

- Default cap

- The cap on default charges will be £15.

- Interest can continue to be charged but at no higher rate than the initial cost cap (calculated per day on the outstanding principal and fixed default charges).

- The total cost cap will be 100% of the total amount borrowed, applying to all interest, fees and charges.

- It will apply to high-cost short-term credit (HCSTC) as defined in our current CONC rules.

- The cap will cover debt collection, debt administration and other ancillary charges; and charges for credit broking for a firm in the same group or where the broker shares revenue with the lender.

-

- The price cap will apply to each loan agreement, and so to repeat borrowing in the same way as for a first loan.

- Firms engaging in this market should be participating in real-time data sharing, so that the vast majority of loans are reported in real-time.

- Recent progress is in line with our expectations. This will be kept under review.

- Our supervisory approach will follow our standard model.

- UK-based debt collectors will be prevented from collecting debts arising under HCSTC agreements entered into by incoming ECD lenders whose charges exceed the price cap.

- UK-based debt administrators will not be able to enforce or exercise rights on behalf of a lender under such HCSTC agreements.

- The Treasury has already announced its intention to lay before Parliament, ahead of the cap coming into effect on 2 January, an Order to confer a power on the FCA allowing us to take action if an incoming firm abuses the EU right of free movement by establishing in another member state directing all or most of its activities into the UK, with a view to avoiding rules that would apply if it had been established in another member state.

- There will be a review of the price cap in the first half of 2017.

Application of the cap to loans made before January 2015- We have adjusted the rules so that if an HCSTC agreement is modified after 2 January 2015, charges imposed before 2 January must be taken together with charges imposed after that date for the calculation of the cap.

- We have amended the rules to cover calculation of the cap when loans are refinanced.

- We have clarified that when an agreement is unenforceable, consumers still have a statutory duty to repay the principal, once a firm has repaid the interest or charges to the consumer, or indicated that there are no charges to repay. Customers must repay within a reasonable period. Lenders cannot make a demand in less than 30 days. We give guidance on what is reasonable in different circumstances.

- We will do further work to assess the impact of repeat borrowing and whether firms are adequately assessing affordability.

- The FCAs final rules for all credit firms including payday lenders were published in February 2014.

- The Money Advice Service is publishing new advice to help consumers who are considering taking out payday loans.

- Firms must be authorised by the FCA, or have interim permission, to carry out consumer credit activities. Firms with interim permission need to apply for authorisation in an allocated application period which last for three months and run from 1 October 2014 to 31 March 2016.

- The FCA took over responsibility for the regulation of 50,000 consumer credit firms from the Office of Fair Trading on 1 April 2014.

- The Financial Services and Markets Act 2000 gives the FCA powers to investigate and prosecute insider dealing, defined by The Criminal Justice Act 1993.

- On the 1 April 2013 the Financial Conduct Authority (FCA) became responsible for the conduct supervision of all regulated financial firms and the prudential supervision of those not supervised by the Prudential Regulation Authority (PRA).

- Find out more information about the FCA.

Free/impartial debt advice: National Debtline | StepChange Debt Charity | Find your local CAB

IVA & fee charging DMP companies: Profits from misery, motivated ONLY by greed0 -

Response from the CFA.

http://www.cfa-uk.co.uk/media-centre/press-releases/current-press-releases/cfa-responds-to-fca%E2%80%99s-cap-on-the-total-cost-of-credit.html11 November 2014

CFA responds to FCA’s cap on the total cost of credit

Speaking about the cap on the cost of credit, Russell Hamblin-Boone, Chief Executive of the Consumer Finance Association, which represents some of the best known short term lenders, said:

“Higher standards of conduct have gone hand in hand with a reduction in loans being approved. With the cap, fewer people will get loans from fewer lenders but the demand for credit will still be there and so there will be no significant impact on debt levels.

“The warning signs are already there. Only a quarter of people turned down for loans under tougher lending criteria said that they were better off not getting the money; the rest incurred charges for missed payments. The regulator will need to monitor this closely and act to prevent illegal lenders filling the credit gap.”

-Ends-Free/impartial debt advice: National Debtline | StepChange Debt Charity | Find your local CAB

IVA & fee charging DMP companies: Profits from misery, motivated ONLY by greed0 -

Well, it's a start... But while it's ok to say that it's capped at £24 interest and charges for a £100 loan in a month it still means that someone borrowing £1000 will be paying back £240 in interest...

Personally, I would have liked to have seen an upper limit brought into effect on how much could be borrowed too to acknowledge that it is intended as a short term/payday loan.

I know this will bring out the cries of 'Nanny state' and 'irresponsible lender' etc but introducing a cap isn't going to change peoples mindset overnight.

It will be interesting to see what changes lenders make to side step around the new rules, perhaps more PDL brokers *spit* cropping up in the mainstream or more payday lenders offering mid/long term loans similar to Provident?

MB0 -

If they ban loans from rolling over I can see firms swapping customer data to get round this. Payday UK sends Wonga customers adverts offering a "new loan" and Wonga does the same to Payday UK customers, both get round the rules.If you don't like what I say slap me around with a large trout and PM me to tell me why.

If you do like it please hit the thanks button.0 -

So, borrow £1,000 , the interest piles up so the amount owing is £2,000. What is the incentive for the borrower to pay a penny, as the effective interest rate is now zero?

So the lender now sells the debt for £1,100 to a debt "specialist".

Obviously the new firm can charge for collection expenses.

Then they send the bailiffs in.

Somebody somewhere seems to have the fantasy that the lender will be stuck with a £2,000 debt, which they just write off to offset corporation tax.0 -

This is all good, however whats the APR on provident loans?Don't put your trust into an Experian score - it is not a number any bank will ever use & it is generally a waste of money to purchase it. They are also selling you insurance you dont need.0

-

The other loophole seems to be the "revolving credit" or a longer term facility (6/12 months) at rates in the 100's APR...0

-

Gordon_the_Moron wrote: »If they ban loans from rolling over I can see firms swapping customer data to get round this. Payday UK sends Wonga customers adverts offering a "new loan" and Wonga does the same to Payday UK customers, both get round the rules.

That would be likely to fall foul of the new approach to affordability and the emphasis that PD lenders have to report all transactions to credit reference agencies.0 -

Hi all,

I have a friend who has a loan of £300 from last year, I believe from August, and have to pay £80 each month for 9 months. The new law has any influence or affect in any way loans as the previous example?

Thanks0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards