We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

do i add the fee or pay it, what is cheaper

Comments

-

do you have to pay to get out of either?

If you plan to change in a year .. and it costs you to get out - you have to add that in too...

ALSO - in 2 years you might not be able to get the 'liftetime tracker rate' .. it may well be higher - as i'm sure if rates increast the tracker rates will too..0 -

hi, there are no penalties on either mortgage which is why i thought it may be better to take this route rather than fixing straight away. bu as you say the rates start rising then the deals get pulled and new deals offered at higher rates.Listen to what people say, but watch what people what people do!!0

-

What's the rate, payment and follow on rate of your current deal?

add the fees make the payment the same and check after 2 years.

working over 20years

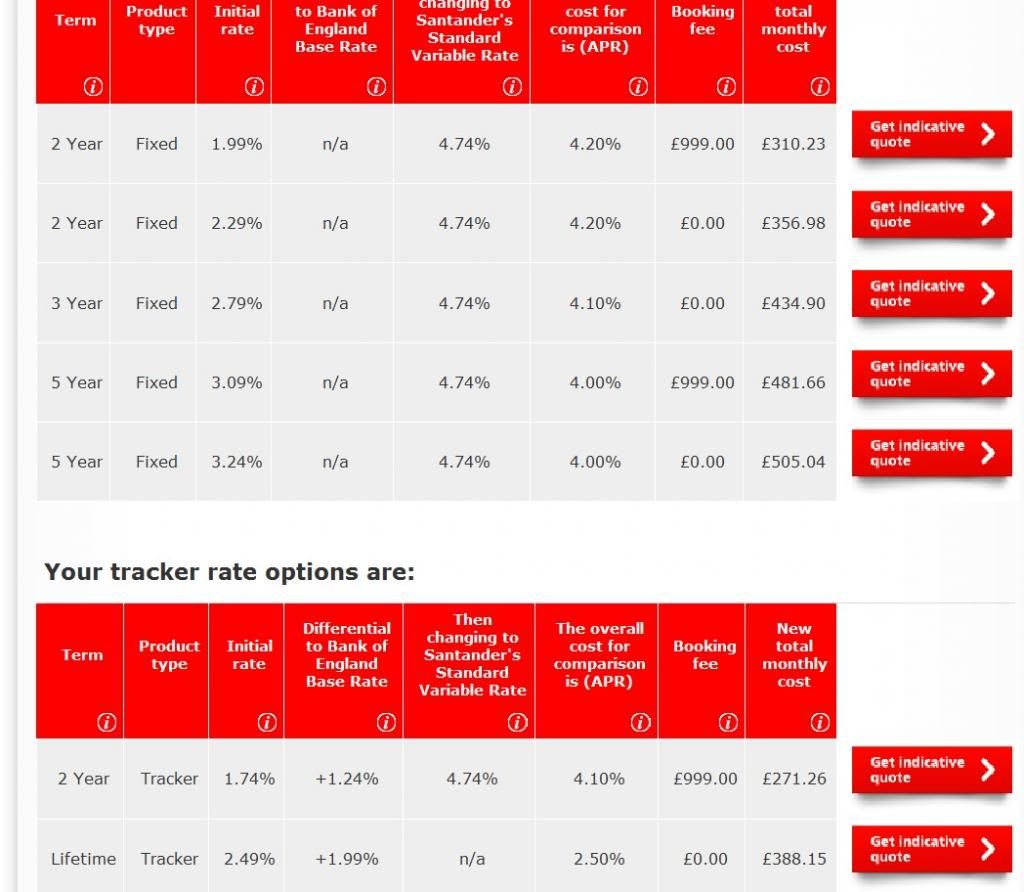

1. £187k @ 2.49% £987pm

2. £188k @ 1.74% £928pm

lets call that £1k in 2 years you will owe.

1. £171,957

2. £170,248 (£1610 saving towards the next set of fees)

add £600pm overpayment (can you do this on the fix? )

1. £157,208

2. £155,606 ( now 1600 )

Now you have to consider the follow on rate of the fix the costs to re mortgage and the deals that will be available and if your circumstances don't change to make a new deal harder.

When rates rise will the tracker rate premiums over base go up or down or stay the same, base + 2% seems to be where they are stabilizing.

How much will your LTV change with the overpayments will it improve your deal choices.

With a £1600pm payment on 2.49% yo pay off the mortgage in 11years 2months.

(unless rates rise)0 -

thanks for replying to my questions.... ive thin ki have mental drain working all the possibilities out.

our LTV is really good its about 40%

i jsut spoek tot he bank and they have a online transfer service which lists all the deals out and i may try to speak to someone as they offer advice aswell.

these costs are based on interest only for now....

as i say this next year im really going to overpay and the lifetime tracker looks intresting because i can really overpay on it but theres only £117 difference on monthly payments between the lifttime tracker and the five year year whihc has no fees on it.

I know with fixed you can only overpay by so much each year but i suspect we can managed £1500 a month overpayment so it will nearly be 20k over the year. Listen to what people say, but watch what people what people do!!0

Listen to what people say, but watch what people what people do!!0 -

Are you saying you can put a total payment of £2kpm towards this mortgage?

working with the 5y fix at £505pm + £1500pm overpayment £2005pm on £187k

after 5 years

£89,436 Fix

£83,798 Tracker if rates stay low this is the lowest amount.

The longer they stay below the fix the higher they can go above the fix to still breakeven.

eg if they stayed low they can go up to

1y 3.52%

2y 4.00%0 -

yeah that was a bit ambitious, my current payments are £621 a month on 3.99% fixed which is coming to a end in june. so the difference between the highest fixed rate and what we are currently paying is £146.00 i can add a month.

plus i finished my car loan last month so i have another £273.00 a month to put into the mortgage.

also wife has just started back at work and we are going to live as we did before on my wage and nearly everything after tax will go into the mortgage so i reckon we should have £1000 to put down so reckon about £1400 a month extra down.

As i say we plan to do this for at least a year but that was based on the fleixable rate and trying to take advantage of the lower rate, thats what tempts me because we can overpay and then jump when the rates rise as there are penalties.Listen to what people say, but watch what people what people do!!0 -

One key here is you don't NEED to fix you have plenty of headroom,

Long term the tracker may be the best option and not bother changing unless you find a better tracker, give up the idea of jumping on a fix.

The hassle and fees can eat into savings, follow on rates can catch you out if circumstances change.

Base+2% is not a bad rate to be looking at long term and anyone with that has had that as a follow on rate have been advised to keep it.

I would also do a forward review of what money you need to keep back saving for things, short term emergencies are covered by just not overpaying one month.0 -

getmore4less wrote: »One key here is you don't NEED to fix you have plenty of headroom,

Long term the tracker may be the best option and not bother changing unless you find a better tracker, give up the idea of jumping on a fix.

The hassle and fees can eat into savings, follow on rates can catch you out if circumstances change.

Base+2% is not a bad rate to be looking at long term and anyone with that has had that as a follow on rate have been advised to keep it.

I would also do a forward review of what money you need to keep back saving for things, short term emergencies are covered by just not overpaying one month.

Just want to say a big thanks for the time you have taken to reply to my questions and the patience, really appreciated. thankyou ever so much. makes a bit more sense to me now and thats the way i was leaning but just wasnt sure.Listen to what people say, but watch what people what people do!!0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards