We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

How do you keep track of spending

Coco_Belle_2

Posts: 3 Newbie

Hi everyone,

I am looking for some advice on the best way to keep track of spending please.

My husband and I are guilty of burying our heads in the sand over financial worries and would spend first and worry later.

So I am looking for some easy to keep, and maintain, budget tracking ideas please.

I keep receipts but don't really know what to do with them, I don't know what to keep a record of, or how (online, spreadsheet, notebook) and I know that if it is too complicated or time-consuming then I won't manage to keep on top of it.

Thanks for your help in advance

x C x

I am looking for some advice on the best way to keep track of spending please.

My husband and I are guilty of burying our heads in the sand over financial worries and would spend first and worry later.

So I am looking for some easy to keep, and maintain, budget tracking ideas please.

I keep receipts but don't really know what to do with them, I don't know what to keep a record of, or how (online, spreadsheet, notebook) and I know that if it is too complicated or time-consuming then I won't manage to keep on top of it.

Thanks for your help in advance

x C x

0

Comments

-

I use a spreadsheet as it does the calculations for you as you make changes and i budget for the coming month so i can see what cash will be left in advance. start with all income for the month at the top (so the period starts from payday) then list all direct debits and standing orders due for the month. then put total figures in for groceries and for any other area you will be spending on for the coming month. this will be estimated figures but i record all actual spending daily to keep track.. then do a calc and take total expenditure from your income and hopefully there should be a surplus! if there is a minus you will need to reduce your estimated figures a bit (unless you have an overdraft which you can use).. then its just a case of marking off all figures as they are paid (i highlight paid amounts in bold) and recording all spending as you go along.. i like it because it ensures everything is accounted for and you can see where you are going to be at the end of the month rather than not knowing. when the next month comes round i just take the bold off and use the figures again. just takes a bit of time at first to set up the spreadsheet though but its worth it as it helps to keep good track of where your money is going!0

-

Thanks Zenthra,

I am trying to set up a spreadsheet so just wondered if it would be easier to do a written running total and then just do the entries into the spreadsheet weekly or something.

I don't really know what headings to use either, or even how to do the calculations. I've got a lot of work to do haven't I?0 -

Hi,

I have a small book with 3 columns in, date, amount spent and what it was for. I use this in conjunction with internet banking to keep tabs on my balance. I take out a set amount each week cash for food and petrol and set up standing orders and direct debits for everything else. It works for me,“We buy things we don't need with money we don't have to impress people we don't like.”0 -

When i was keeping a proper spending diary I used a simple note taking free app on my phone and just noted everything I spent. That lead to greater discipline about buying things like coffee, sandwiches, lunch at work, impulse buys of computer games and things which REALLY add up.

Nowadays, I just have to keep the budget on track. I take $50 our for the week (Living in Australia) and that's my fun money for swimming, coffee, incidental expenses, bus fares, etc. I sometimes don't need it all, so then it rolls into next weeks and I take less out.

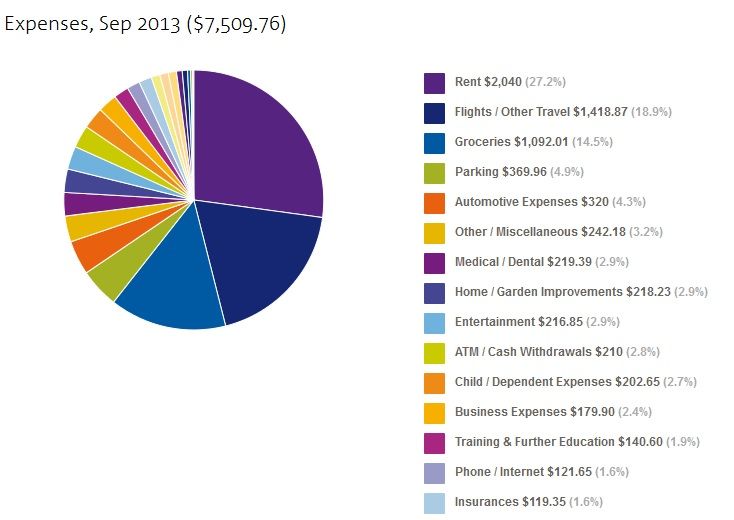

Online banking is very powerful. Our bank has excellent spending tracking tools. You go through your transactions and assign them to different budgets: groceries, healthcare, childcare, eating out, fuel, etc. Then, it automatically categorises similar transactions into types afterwards, and it gets it pretty much spot on.

We end up with something like this:

(I hasten to add this is not a normal month, with a number of car expenses and my wife working abroad for most of it).

I find that very useful to keep track of budgets and see where money is not being used effectively.0 -

I also use an app. It's on the iphone and free. It's very handy, everytime I make a purchase I just input the amount and choose a category - like rent, bills or entertainment. You can make your own categories.

I then at the end of the month put this on a spreadsheet - or if I upgrade the app for £1.99 I can send it as a spreadsheet and other things.0 -

I use a spreadsheet but I've set it out like a bank statement - date, item (e.g Tesco), amount in, amount out, balance. The preset things like direct debits are already in there - I just add a row if I take money out of the cashpoint etc, and then recalculate by copying the formula above through the new row into the row after my new entry. That's my basic current account sheet - got a lot of others in there that all self-reference (and in fact my current account sheet goes all the way to 2028!), so change one cell and it updates various sheets, but I don't think you need that."Save £12k in 2019" #120 - £100,699.57/£100,0000

-

I put as much as I can on cards and download data frequently onto ancient Microsoft money software. I know roughly when my credit card statement is due and enter a manual transaction into my current account for the payment date, updating the amount as my cc balance increases. I put all future payments into the relevant account including (interest free) loan repayments, mobile contract payments, direct debits, standing orders, interest on savings etc. I have 'piggy bank' accounts for Christmas, holidays, car expenses and child benefit which I can draw on if my current account doesn't have enough to cover my cc bill and I also have emergency savings which I prefer not to use at all but they are there for when the washing machine breaks down etc. I have a spreadsheet where I enter any 'borrowings' from emergency savings and try and pay them back within a reasonable time frame.

I know the general wisdom is to operate solely or mainly in cash but I know I wouldn't have the discipline to write down cash expenditure and my memory isn't great! At least with a card I know exactly where my money has gone. Cash withdrawal used to be a category in my budget but I never knew where the cash had gone so I now rarely carry cash though I have some locked away at home and £10 in the glove compartment of my car in case I can't pay by card or I only need a few pence for something. The only other cash I tend to withdraw is coins for school dinners and I now categorise this as a child related expense and comes out of child benefit. I sometimes draw on this for car parking if I know I'm going to a car park where I can't pay by card. Any change I get I put in jars for when I need cash for the vending machine at college.

The only time I carry substantial amounts of cash is when I'm on holiday just in case ...0 -

I have used Microsoft Money for years - since around 1998. It no longer exists as a product but the last version (2005) can be downloaded free.

It can take a while to set up and organise but will allow you track all bank accounts, credits cards, loans and payments and the key thing missing from current products which keeps me using MSmoney is 'cash flow' which allows me to look at my projected cash flow for the next 12 months (or even longer periods!)CHALLENGES MAR'14:

CHALLENGES 2014: £1-a-day#43 £84/£365; £3350k BY MAY £2700/£3350; £1500 BY JULY £0/£1000

EMERGENCY FUND £0/£2500; 2014 MFW #61 £0/£2500; CC £290/£2270

2014 SUMMARY (POAYD 2014 #120 £3074/£12485 24.6%

101 MONTHS... MORT: [STRIKE]£63,000[/STRIKE] £66850 | LOANS: [STRIKE]£26,000[/STRIKE] £0 | CARDS: [STRIKE]£33,000[/STRIKE] £1980

0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards