We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Endowment questions

dirk_

Posts: 58 Forumite

Afternoon All

I received my latest statement from Aviva yesterday and wonder if someone can offer advice on if it is worth keeping this policy running.

It is no longer linked to any mortgage

Annually we pay in £740.16

We did think of surrendering this policy and paying a lump sump in to our mortgage (bringing it down to round 30k)

Any suggestions ?:D

[IMG][/img]

I received my latest statement from Aviva yesterday and wonder if someone can offer advice on if it is worth keeping this policy running.

It is no longer linked to any mortgage

Annually we pay in £740.16

We did think of surrendering this policy and paying a lump sump in to our mortgage (bringing it down to round 30k)

Any suggestions ?:D

[IMG][/img]

0

Comments

-

Is there a maturity guarantee?

Take any guarantee into account when considering termination.I am a mortgage broker. You should note that this site doesn't check my status as a Mortgage Adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice. Please do not send PMs asking for one-to-one-advice, or representation.0 -

Is this something Aviva can tell me??

Thanks for the reply0 -

Yes. Old CU, NU and GA policies which were absorbed into Aviva can be subject to a mortgage endowment promise;-

http://www.aviva.com/media/news/item/uk-strong-growth-for-aviva-with-profits-customers-9619/Aviva launched its mortgage endowment promise in 2000 to assist policyholders who, at the time of the announcement, faced a projected shortfall on their mortgage endowment policy (the amount needed to pay off their mortgage when it matured). The mortgage promise was conditional on the company earning a sufficient investment return on its free reserves as well as the policy not being altered or sold. Aviva committed around £1 billion of capital for future endowment shortfall assistance – underlining the strength of its with-profits funds.I am a mortgage broker. You should note that this site doesn't check my status as a Mortgage Adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice. Please do not send PMs asking for one-to-one-advice, or representation.0 -

Thanks for the advice, I will contact Aviva and find out0

-

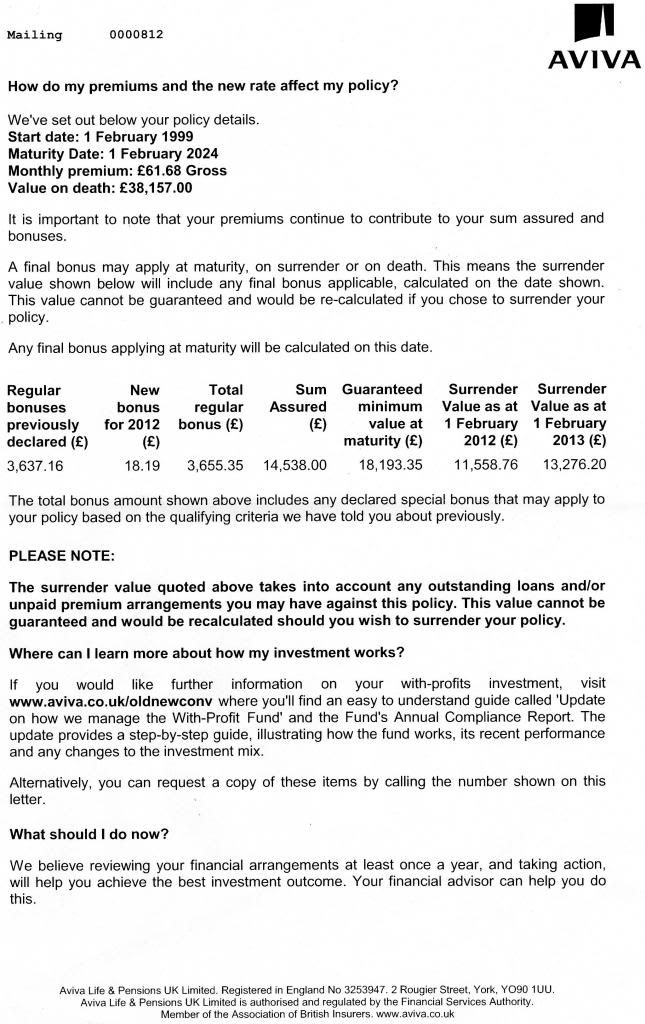

the maturity guarantee is £14538.00

Current surrender value is £ 13276.200 -

So, you have something to think about...I am a mortgage broker. You should note that this site doesn't check my status as a Mortgage Adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice. Please do not send PMs asking for one-to-one-advice, or representation.0

-

the maturity guarantee is £14538.00

Current surrender value is £ 13276.20

Aviva normally quote the MEP as a figure that is added maturity. So, if the MEP is £14,538 and you got a return that say matched the middle projection figure then they would add the MEP value to that (capped to target figure if it goes above it).I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

Thanks for the info guys

But can you explain that so a 5 year old can understand it:question:0 -

I am not a financial advisor, so don't blame me if this is wrong.the maturity guarantee is £14538.00

Current surrender value is £ 13276.20

As I see it, you are paying £740/year to have £14538 at the earlier of 2024 or your death. But you do also have the prospect of growth on that money beyond the £14538.

At the moment you are able to cheat death by taking £13276 now and not paying premiums for another 2 years to give you roughly your £14538. That money will earn the return of reducing your mortgage interest which is more certain than the returns on the policy. Given the surrender value is so high, there is little added value in the life insurance component.

I think I would take the surrender. Having said that, if for any reason the returns over the next few years are likely to outrun the premiums, I might hold onYou might as well ask the Wizard of Oz to give you a big number as pay a Credit Referencing Agency for a so-called 'credit-score'0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards