We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Early-retirement wannabe

Comments

-

I assumed it was the OP renamed as the old name hasn't been used post migration.atush said:No last post unless you are the OP.

Otherwise quite rude

i may be wrong though.1 -

why the need to assume anything - if you read the signature line which says it all ;-)ffacoffipawb said:

I assumed it was the OP renamed as the old name hasn't been used post migration.atush said:No last post unless you are the OP.

Otherwise quite rude

i may be wrong though.

The questions that get the best answers are the questions that give most detail....0 -

The signature wasnt there earlier.Hmgdavid said:

why the need to assume anything - if you read the signature line which says it all ;-)ffacoffipawb said:

I assumed it was the OP renamed as the old name hasn't been used post migration.atush said:No last post unless you are the OP.

Otherwise quite rude

i may be wrong though.0 -

Early_Retire_Free said:Last post

It feels like the "wannabe" tag has run its course.

As many of you who've followed this thread will have experienced, actually getting to retirement has been a very difficult (mental) journey. For most, the financial decision and working towards the financial goal itself becomes all-consuming. But for us (and this isn't bragging), our finances have been sorted for some time and the real challenge was always the mental side of retirement, finding things to do and finding a purpose.

But I now wonder whether "purpose" is just a media creation. Do we actually need a purpose to feel valued and valuable? Maybe it helps in the overall scheme of things but its possibly overrated.

I've increasingly been describing myself as "retired" and more comfortable with the term. I haven't done anything that could be regarded as gainful employment for the last six months and I think I've underestimated my capacity for being happy doing very little indeed.

That's not to say I've become a couch potato because time has been filled with exercise and holidays (indeed I'm writing this from over 11,000 miles away). But I am now able to reflect logically and rationally and face to the fact that the world of work is gone .....but I love my new life.

I've aligned my MSE username with my web presence but the key message from this post is that the "wannabe" is no more. I am early retired.

Yes me too! I have been "not employed and living off my company pension well before normal retirement age" for nearly a year now. It took me a good 8 months to get comfortable with the idea! I am doing plenty of things and nothing at the same time! My label is "retired for now", which seems to fit the bill! Roll on spring!

"For every complicated problem, there is always a simple, wrong answer"0 -

Congrats - I was beginning to think you weren't going to do it - enjoy!Early_Retire_Free said:Last post

I am early retired.

0 -

Not the way i read it.0

-

Another April rolls round, and plenty to update about this year, although the TLDR version is that everything is still on course for early retirement sometime in the period between June 2022 to September 2023, as has been the plan for a few years now.As pictures can now easily be included I've added some charts from my spreadsheets for greater detail, although unfortunately that makes the post quite long but hopefully more interesting. I think the post gives good insight into how I have prepared and planned for retirement, how I hope things will turn out in the future and how I have tried to mitigate risks which can be anticipated, both in terms of investment risk but also pension policy change risk.BackgroundMyself and my wife are both aged 42, no children and no plans for any. We live in London, and plan to retire in a few years to go traveling for 1-3 years before returning to live in mid/north Wales. I expect the cost of our house in Wales to be about the same as the value of our London house so that change should be neutral in terms of savings. We want to be financially independent by the time we leave to travel and not have to work again, although we may well do voluntary work.Non pension assets

- House value - £504K

- Cash - £67K

- ISA - £206K

Non pension liabilities- Mortgage - £39K

- Credit card debt - £74K

Expenditure levelsI log our annual expenditure as a residual, using the equation:- Consumption=Total income - pension saving - ISA saving - income tax - National Insurance - mortgage payments - change in minor debt levels

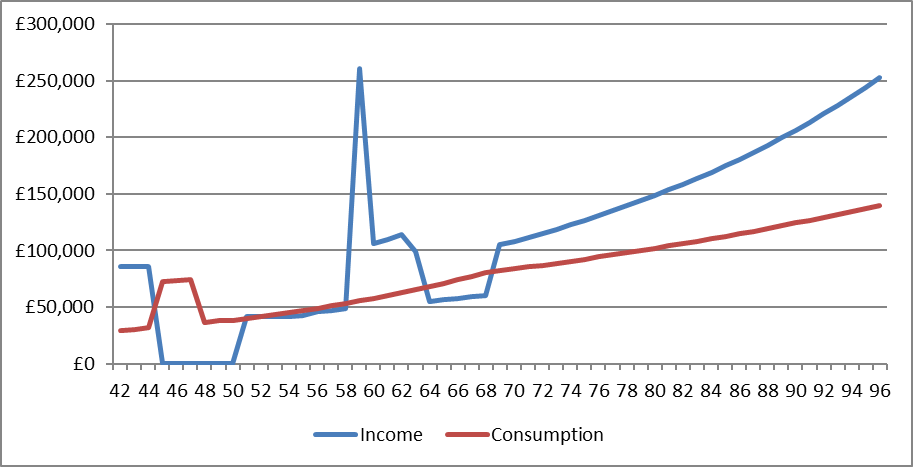

I then revalue past years by average earnings change, and take the mean value of the adjusted amounts. This ensures all expenditure is captured, and having a 7 year period means even occasional expenditure such as house maintenance and car purchase is captured in the calculation. Using figures from the last 7 years gives revalued average annual consumption of £29,471 p/a for the household (ie me and my wife), and this has been consistently around £30,000 each year.The chart below shows our household expenditure allocation over the last 7 years. It shows a shift in saving away from DC pensions after 2015/16 (with a consequent increase in amount of income tax paid), and towards ISA saving from 2017/18. The consumption figures for 2017/18 and 2018/19 need to be viewed together, as some significant expenditure for holidays in 2018/19 was paid for in 2017/18. Income after retirementBetween leaving employment at around age 45, all income will come from ISA saving until age 50.Both myself and my wife are in Defined Benefit pensions which have a protected minimum pension age of 50, and we plan to commence them at age 50. Based on current accrued pension, this will give a combined annual income of slightly under £35,000 p/a before tax from age 50 which should meet almost all of our expenditure needs, with any additional income requirements being met from ISA savings.We also have some Defined Contribution savings, which are slightly over £200,000 (falling from about £230,000 a few months ago) and these will be used between minimum pension age (which I assume to be 58) and State Pension age to provide an equivalent income to State Pension.We will also both have full State Pensions from age 68, although some voluntary contributions after we stop work will be needed to get full accrual.COVID19 impact and asset / debt allocationOur income is unaffected by COVID19.We had about £230,000 in Defined Contribution and just over £200,000 in ISAs prior to the recent market volatility. The ISAs are invested very defensively as most of the funds will be needed within the next 8 years, and these experienced only a very small fall, something like 2%. The Defined Contribution funds were invested with more risk, reflecting that they won't be used for another 16 years, will be subject to income tax, and can replenished with the benefit of tax relief if required. The fund value of our DC investments is down a bit under £30,000.Fortunately, we had more in DC than we needed due to the strong investment growth in recent years, so the loss is of little consequence to our plans. I model alternative scenarios as a sensitivity check, and the highest amount of DC pension we would want from these scenarios is only an additional £20,000 in the DC funds so I will wait until just before leaving employment in 2-3 years before making any decisions about extra contributions. If minimum pension age doesn't increase to 58 then we would want quite a lot more in DC pensions, unfortunately, I doubt there will be any clarity about that anytime soon so I am assuming the worst plausible case for my planning, and that funding for when we are aged 55 to 58 (in excess of our Defined Benefit pensions) will come from ISAs rather than DC pension.When COVID19 hit, I renewed a lot of 0%, nil fee balance transfers, so currently we have about £75K of credit card debt, most not payable until 2021. This will be used to pay off our mortgage when our fixed-rate term expires at the end of this month and to make half of our 2020/21 ISA contributions earlier than we would usually make them. I expect to be able to repay all credit card debt (from income) as 0% offers expire from now on, whilst maintaining full ISA contributions for both of us. I also paid my consultancy's Corporation Tax bill earlier than necessary just to ensure there was no high-priority debt outstanding going into what might be turbulent times.Future income and consumptionThe chart below shows future net income and consumption (in cash terms) by age, assuming my wife and I leave employment in April 2023. I assume consumption needs escalate in line with average earnings growth (4.2% p/a in the long-run) to age 68, and by CPI (2% in long-run) thereafter.

Income after retirementBetween leaving employment at around age 45, all income will come from ISA saving until age 50.Both myself and my wife are in Defined Benefit pensions which have a protected minimum pension age of 50, and we plan to commence them at age 50. Based on current accrued pension, this will give a combined annual income of slightly under £35,000 p/a before tax from age 50 which should meet almost all of our expenditure needs, with any additional income requirements being met from ISA savings.We also have some Defined Contribution savings, which are slightly over £200,000 (falling from about £230,000 a few months ago) and these will be used between minimum pension age (which I assume to be 58) and State Pension age to provide an equivalent income to State Pension.We will also both have full State Pensions from age 68, although some voluntary contributions after we stop work will be needed to get full accrual.COVID19 impact and asset / debt allocationOur income is unaffected by COVID19.We had about £230,000 in Defined Contribution and just over £200,000 in ISAs prior to the recent market volatility. The ISAs are invested very defensively as most of the funds will be needed within the next 8 years, and these experienced only a very small fall, something like 2%. The Defined Contribution funds were invested with more risk, reflecting that they won't be used for another 16 years, will be subject to income tax, and can replenished with the benefit of tax relief if required. The fund value of our DC investments is down a bit under £30,000.Fortunately, we had more in DC than we needed due to the strong investment growth in recent years, so the loss is of little consequence to our plans. I model alternative scenarios as a sensitivity check, and the highest amount of DC pension we would want from these scenarios is only an additional £20,000 in the DC funds so I will wait until just before leaving employment in 2-3 years before making any decisions about extra contributions. If minimum pension age doesn't increase to 58 then we would want quite a lot more in DC pensions, unfortunately, I doubt there will be any clarity about that anytime soon so I am assuming the worst plausible case for my planning, and that funding for when we are aged 55 to 58 (in excess of our Defined Benefit pensions) will come from ISAs rather than DC pension.When COVID19 hit, I renewed a lot of 0%, nil fee balance transfers, so currently we have about £75K of credit card debt, most not payable until 2021. This will be used to pay off our mortgage when our fixed-rate term expires at the end of this month and to make half of our 2020/21 ISA contributions earlier than we would usually make them. I expect to be able to repay all credit card debt (from income) as 0% offers expire from now on, whilst maintaining full ISA contributions for both of us. I also paid my consultancy's Corporation Tax bill earlier than necessary just to ensure there was no high-priority debt outstanding going into what might be turbulent times.Future income and consumptionThe chart below shows future net income and consumption (in cash terms) by age, assuming my wife and I leave employment in April 2023. I assume consumption needs escalate in line with average earnings growth (4.2% p/a in the long-run) to age 68, and by CPI (2% in long-run) thereafter. The initial spike in consumption is an allowance of an additional £40,000 p/a to fund travel (this is in addition to the standard consumption of c£30K p/a).The spike in income around age 58 is Defined Contribution pension commencement lump sums and then drawdown each year set to avoid higher rate tax (thresholds assumed to increase in line with average earnings) until the pots are exhausted. If all turns out as modeled, I would have £40,000 of savings in reserve at all times. That isn't much, but I think we should have plenty of income for our needs so am relaxed about having relatively small reserves.Sources of incomeThe chart below breaks down the source of pension. Note that as our birthdays are not aligned with tax years I model income as starting from our first birthday after the start of a tax year for convenience, which slightly understates the amount of pension income we will receive.Note that people often comment about the high value of State Pension shown in the chart, especially in later years. This is a consequence of the Triple-Lock policy escalating the value relative to prices significantly as the increase compounds over time, and in particular earnings growth being assumed to be 4.2% p/a compared to CPI growth of 2% p/a. As the chart above shows, we are not particularly dependent on State Pension to meet consumption needs, so if the Triple Lock is removed it wouldn't affect our plans.

The initial spike in consumption is an allowance of an additional £40,000 p/a to fund travel (this is in addition to the standard consumption of c£30K p/a).The spike in income around age 58 is Defined Contribution pension commencement lump sums and then drawdown each year set to avoid higher rate tax (thresholds assumed to increase in line with average earnings) until the pots are exhausted. If all turns out as modeled, I would have £40,000 of savings in reserve at all times. That isn't much, but I think we should have plenty of income for our needs so am relaxed about having relatively small reserves.Sources of incomeThe chart below breaks down the source of pension. Note that as our birthdays are not aligned with tax years I model income as starting from our first birthday after the start of a tax year for convenience, which slightly understates the amount of pension income we will receive.Note that people often comment about the high value of State Pension shown in the chart, especially in later years. This is a consequence of the Triple-Lock policy escalating the value relative to prices significantly as the increase compounds over time, and in particular earnings growth being assumed to be 4.2% p/a compared to CPI growth of 2% p/a. As the chart above shows, we are not particularly dependent on State Pension to meet consumption needs, so if the Triple Lock is removed it wouldn't affect our plans. Retirement flexibilityLeaving employment in April 2022 would be just about viable, but would require a few cut-backs and leave very little margin.In practice, I think we will end up having a leaving window between June 2022 and September 2023 - this is because June would ensure we exploit our income tax Personal Allowances and qualify for another year of State Pension, whilst September would mean we benefit from summer, bank holidays, and use our income tax personal and basic rate allowances. If I carried on working past September then I wouldn't leave until at least January (to benefit from Christmas period) so I think September is a natural end-point to assume.

Retirement flexibilityLeaving employment in April 2022 would be just about viable, but would require a few cut-backs and leave very little margin.In practice, I think we will end up having a leaving window between June 2022 and September 2023 - this is because June would ensure we exploit our income tax Personal Allowances and qualify for another year of State Pension, whilst September would mean we benefit from summer, bank holidays, and use our income tax personal and basic rate allowances. If I carried on working past September then I wouldn't leave until at least January (to benefit from Christmas period) so I think September is a natural end-point to assume.

8 -

hugheshevi, thanks for such a detailed post - very helpful for a straightforward view on the spending side of the equation.

Give or take I guess you'll have a net worth of around £1M at retirement to (buy a home and) get you to the point where you'll take your DB pension and on to collecting SP. Assuming DB/SP are both 'guaranteed' and 'inflation proof', then you have most of the retirement risks covered (sequence of returns, crashes, out-living assets, declining mental capacity to manage investments, asset management fees).

So, what next? Definitely relax and spend no more time on expenditure data analysis") you have that nailed.

you have that nailed.

My only thought would be that you are planning an extra-ordinarily long retirement period, which means that even tiny risks can take on more importance, so check that you are happy with the long term viability of your DBs and also that they are balanced adequately between the 2 of you if one dies 'early' and the spouses half is enough either way around.1 -

Fascinating post, hugheskevi. There is one aspect I am confused about in your second chart. If the numbers are showing as in real term then how come your and your wife's state pensions are showing increase still unless you are assuming the triple lock system will always be in place, and your predicted CPI is lower than the minimum 2.5% increase?

EDIT: I just realised that hugheskevi did cover this later in the post. Just ignore my question, please! 1

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards