We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Can anyone advise me on default notice?

BigCraigJohn

Posts: 1,082 Forumite

Hi

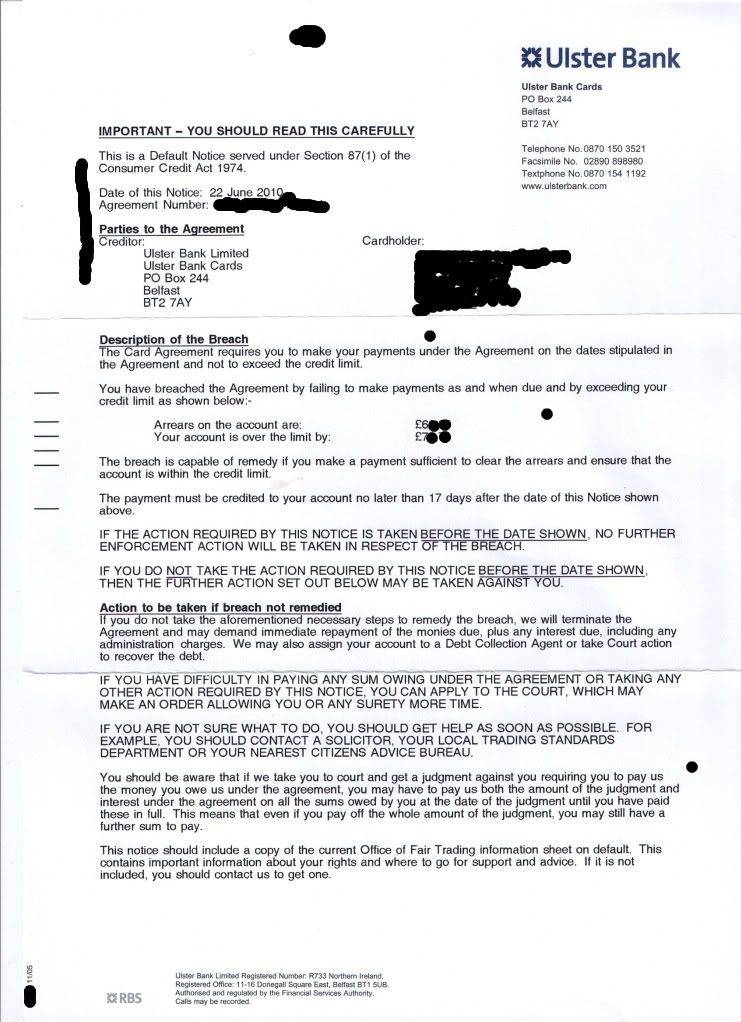

This morning I received what I consider a surprise default from ulster.

Its a surprise because although I was 2 months late I have paid 1 and had just agreed to catch up my arrears by paying extra on my monthly payments over 6 months.

Well anyway the notice was dated 22nd but only gave me 17 days to rememdy from the day after the notice which is next friday. It shows as post mark S which is apparently a business wholesale service where the business diy and royal mail deliver next day after receiving.

It is however clear to me that the notice was not forwarded to royal mail till 25th as it was only delivered today.

Ps here is a scan of the dn and a scan of the envelope

http://i1017.photobucket.com/albums/af299/badgercraig/ulster/ulsterdn.jpg

http://i1017.photobucket.com/albums/af299/badgercraig/ulster/ulsterenvelope.jpg

Can anyone tell me if a>would this deem the notice defective?

and b>is a defective notice really as much of a big deal as you sometimes read?

My current position is that I have 2 recent defaults so another wont hurt + I do hope to clear it which might be easier if the balance was frozen. But I have read that if they terminate on a defective notice that they can only claim the arrears.

I have read on other sites but tbh the whole issue confuses me.

:eek:

This morning I received what I consider a surprise default from ulster.

Its a surprise because although I was 2 months late I have paid 1 and had just agreed to catch up my arrears by paying extra on my monthly payments over 6 months.

Well anyway the notice was dated 22nd but only gave me 17 days to rememdy from the day after the notice which is next friday. It shows as post mark S which is apparently a business wholesale service where the business diy and royal mail deliver next day after receiving.

It is however clear to me that the notice was not forwarded to royal mail till 25th as it was only delivered today.

Ps here is a scan of the dn and a scan of the envelope

http://i1017.photobucket.com/albums/af299/badgercraig/ulster/ulsterdn.jpg

http://i1017.photobucket.com/albums/af299/badgercraig/ulster/ulsterenvelope.jpg

Can anyone tell me if a>would this deem the notice defective?

and b>is a defective notice really as much of a big deal as you sometimes read?

My current position is that I have 2 recent defaults so another wont hurt + I do hope to clear it which might be easier if the balance was frozen. But I have read that if they terminate on a defective notice that they can only claim the arrears.

I have read on other sites but tbh the whole issue confuses me.

:eek:

0

Comments

-

If you are 2/3 months behind they generally send a warning (which you got), by the 3rd month you generally get an actual default which defaults the account.

To your questions.

A1. As the letter says at the top, this is a default notice.

A2. I do not know what you mean by defective notice?

As far as i know, if the bank was to terminate your agreement and default it, then the amount you owe plus cancallation fees will apply. If in your agreement, interest is still chargeable they can charge you your interest rate up until they take you to court. Say you owe £800, they can apply your normal rate say 29.9% up until court date. So say you now owe £1000. That is all the CCJ is granted for and it will not increase. However, they can ask to add 8% to the balence if they have a good reason. So the CCJ could be made out for £1080 + any court fees.Although no trees were harmed during the creation of this post, a large number of electrons were greatly inconvenienced.

There are two ways of constructing a software design: One way is to make it so simple that there are obviously no deficiencies, and the other way is to make it so complicated that there are no obvious deficiencies0 -

Thing is I am only 1 payment in arrears now which is the amount the default is for, I paid a fortnight ago which is registered on this balance. I am slightly over the limit. Infact I think another letter I have even says that no action will be taken providing I pay the arrears within 6 months in addition to my minimum payment.0

-

BCJ

Can you edit your last line.

There are a number of ways in which default notices can be defective; it aloows you to defend a court case. At a basic level this looks OK but you might want to pm 10past6If you've have not made a mistake, you've made nothing0 -

Don't quote me until running it by 10 past 6 but..

I thought a DN had to allow time to be delivered to you and then 14 working days which means weekends are excluded. I'm sure I read somewhere it should be something like 20 or 21 days, but like I said don't quote me.

There is a set way these DN should be set out and the courts should see the finance co as knowing what they are doing. Hope you get it sorted anyway")

I just had another look and it does say 17 days after the date of the notice. I know what I think.Karma - the consequences of ones acts."It's OK to falter otherwise how will you know what success feels like?"1 debt v 100 days £20000 -

Thanks all, well i'm pretty sure this wont be going to court as its a small balance which I will repay once some of my reclaims come in(ltsb pull your finger out son), I was just caught a bit unaware tbh and was happy for this to tick along. Guess its nice to know where you stand ie a defence if they did go to court.

For the record that notice is for 1 months arrears and £40 over the limit.0 -

Interesting.

I have just found the letter I received from them last week.

To Quote

"We are willing to accept a payment of £40 per month for the next 3 months and it will then be reviewed, if at this point your cercumstances have improved your minimum repayment will be put back up to the 3% minimum.

This will be marked on your credit report as an arrangement".

So within 7 days ive been told that it will be marked as an arrangement and ive received a default notice which if I dont pay within 2 weeks i'll be defaulted.

Does this give me any grounds to maybe appeal the default?. Should I write to them now or wait till after?0 -

Well I thought id update this as its a real mixed up affair.

Ulster did accept my repayment plan and had even placed it on my credit report as arrangement to pay, within 2 weeks they terminated the account and now its showing as defaulted despite me paying what was agreed.

Apparently they didn unlawfully rescind the contract by not allowing 14 days to pay the arrears and are therefore only entitled to the arrears(this was advised on cag but I have to write and accept).

Ofcourse I know they wont just accept this but apparently it gives me a good defence if they took it to court, however I do intend on making a f&f within the month.

What a bunch of muppets though(Ulster), I was fully intending on making the agreed payments and they went and terminated.0

{kind=link}

{kind=link}

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.3K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards