We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

CCA valid?

thenightporter

Posts: 74 Forumite

Hi,

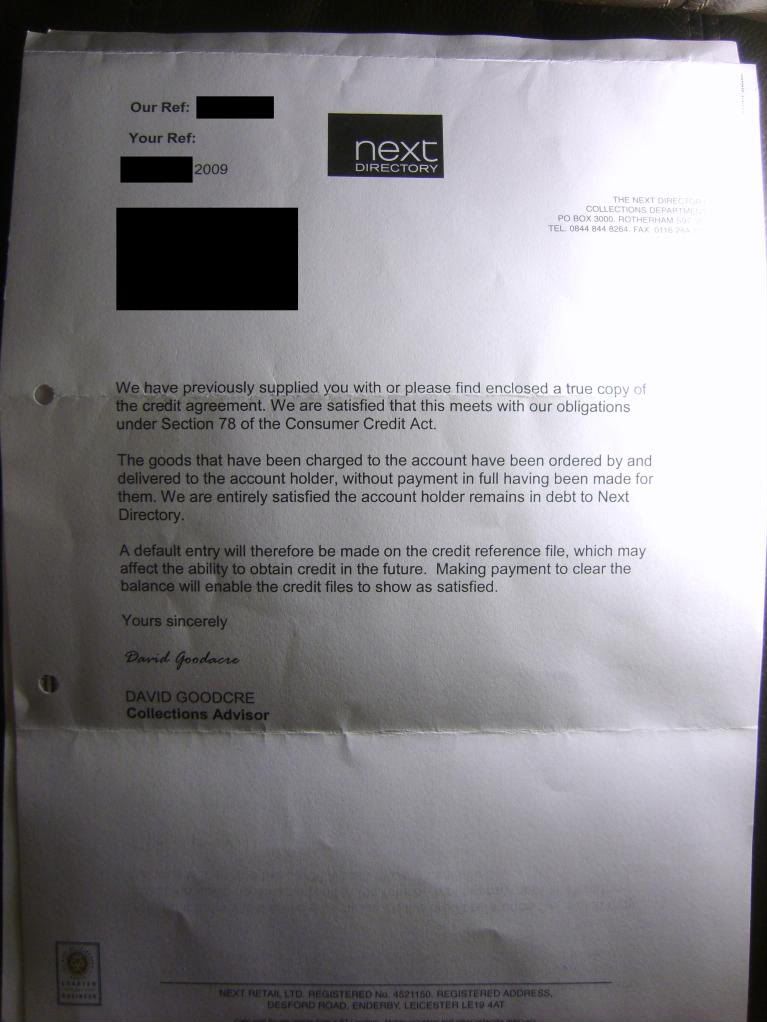

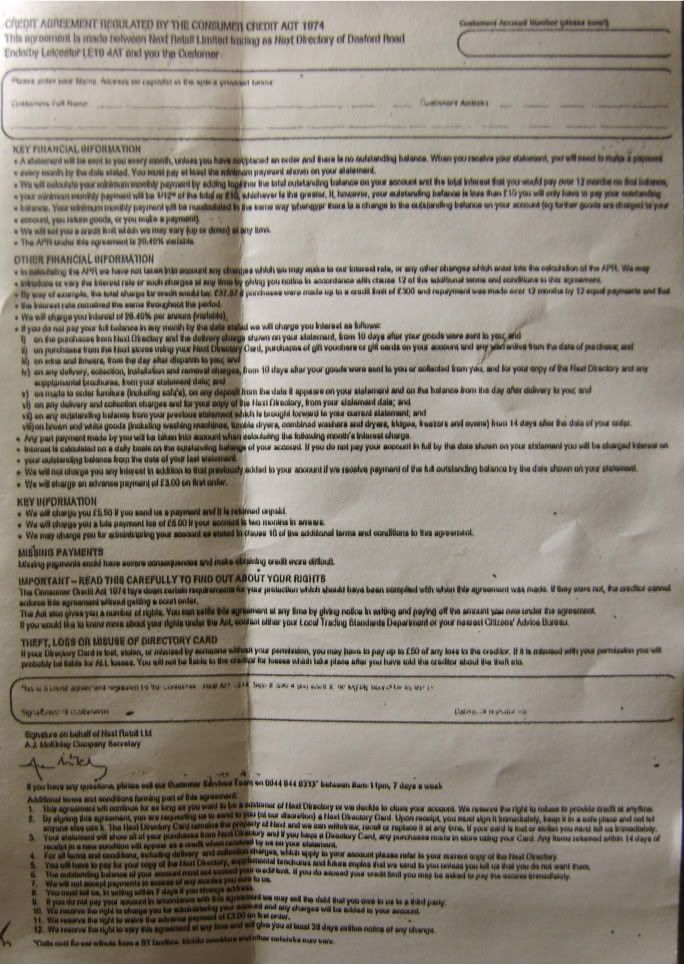

We requested a CCA from Next on the 17/03/09 and received this this morning:

http://i715.photobucket.com/albums/ww154/thenightporter_bucket/coop_cca2.jpg

http://i715.photobucket.com/albums/ww154/thenightporter_bucket/coop_cca1.jpg

(the links say coop but they are from Next - my mistake naming the pictures!)

This appears to be a copy of their current T&Cs. I opened this account in 1998. I does not refer to me in any way at all, could this possibly be a valid CCA?

We are about to start a CCCS DMP and our creditors know this. We want to keep paying Next under a DMP but we don't want to get taken to court and we want them to stop the interest/charges which is why we requested a CCA. What do we do now, assuming this isn't valid? Do we wait for the 12+2 to expire and sent the account in dispute letter but continue as we planned with the DMP payments?

Many thanks

We requested a CCA from Next on the 17/03/09 and received this this morning:

http://i715.photobucket.com/albums/ww154/thenightporter_bucket/coop_cca2.jpg

{kind=link}

http://i715.photobucket.com/albums/ww154/thenightporter_bucket/coop_cca1.jpg

{kind=link}

(the links say coop but they are from Next - my mistake naming the pictures!)

This appears to be a copy of their current T&Cs. I opened this account in 1998. I does not refer to me in any way at all, could this possibly be a valid CCA?

We are about to start a CCCS DMP and our creditors know this. We want to keep paying Next under a DMP but we don't want to get taken to court and we want them to stop the interest/charges which is why we requested a CCA. What do we do now, assuming this isn't valid? Do we wait for the 12+2 to expire and sent the account in dispute letter but continue as we planned with the DMP payments?

Many thanks

0

Comments

-

CCCS won't become involved the the lagality of a CCA, it's for you to decide whether you inculde the debt in your DMP.

The attachhment is not what you requested, in view of that, send them the following letter:

I DO NOT ACKNOWLEDGE ANY DEBT TO YOUR COMPANY

Account Number: XXX

Re; your recent reply to my request under section 77-79 of the Consumer Credit Act 1974

I note that you have replied to the above by sending your companies current Terms and conditions I must inform you that this is not sufficient to comply with the request and that your company is still in default under the act.

To clarify, just sending the Terms and Conditions is a breach of the Act and Regulations as, apart from the information that the Regulations provide that you may exclude, the copy must be a “true copy” of the agreement.

This breach of the agreement can be demonstrated as follows;

As you will know section 180(1) (b) authorises, “the omission from a copy of certain material from the original, or the inclusion of certain material in condensed form.” This refers to statutory instruments made under the heading Copies of document regulations and in this care in particular to SI 1983/1557.

Before leaving section 180 there are two other sections that should be remembered these are:

Section 2(2) (a) A duty imposed by any provision of this Act (except section 35) to supply a copy of any document is not satisfied unless the copy supplied is in the prescribed form and conforms to the prescribed requirements;

And more importantly

Section 2(b) A duty imposed by any provision of this Act (except section 35) to supply a copy of any document is not infringed by the omission of any material, or its inclusion in condensed form, if that is authorised by regulations.

You will see that this quite clearly states that whilst certain items may be left out of the copy document the rest of the document must be in the form and contain all items as prescribed by the regulations.

Turning to the regulations regarding what may be omitted from these copies these are contained with SI 1983/1557.

The regulations state:

(2) There may be omitted from any such copy-

(a) any information included in an executed agreement, security instrument or other document relating to the debtor, hirer or surety or included for the use of the creditor or owner only which is not required to be included therein by the Act or any Regulations thereunder as to the form and content of the document of which it is a copy;

(b) any signature box, signature or date of signature (other than, in the case of a copy of a cancelable executed agreement delivered to the debtor under section 63(1) of the Act, the date of signature by the debtor of an agreement to which section 68(b) of the Act applies);

It is quite clear what can be omitted from the copy document, this again asserts that all other details of the agreement should presented in form and content as required by the regulations.

The requirements of the Agreement regulations 1983/1553 are very explicit in describing the form and content of an agreement and this as I have demonstrated also applies to the copy of any such agreement with the above mentioned proviso.

Nowhere within these regulations does it state that part of the agreement can be presented on a separate document headed terms and conditions.

It does state that all terms and conditions should be within the agreement document and is explicit of the form in which it is presented.

I hope this explains why your reply was unacceptable I await a True copy of my agreement and would remind you again that whilst the request has not been complied with the default continues

Yours faithfully

PRINT ONLY - DON'T SIGN YOUR NAMEClick here for Martins (MSE) advice on who to contact with Debt Issues - YOU HAVE NO REASON TO USE A FEE PAYING DEBT MANAGEMENT COMPANY- THEY CANNOT DO ANYMORE FOR YOU THAN THOSE LISTED IN MY LINK ABOVE.

All information given by myself is offered informally and without prejudice - if in doubt seek help from a qualified and insured professional0 -

Sorry but most next cards are taken out on line or phone . Rules change in April 2007 , so the signing of a CCA does not apply.0

-

Did you not see this from the OP?Sorry but most next cards are taken out on line or phone . Rules change in April 2007 , so the signing of a CCA does not apply.

As The Consumer Credit Act 1974 (Electronic Communications) Order 2004 came into force in December 2004 any online agreements entered into prior to this date still need a signed executed credit agreement.thenightporter wrote: »I opened this account in 1998

You may find this helpful, it's worth bearing in mind, electronic signatures weren't considered valid until this date.Click here for Martins (MSE) advice on who to contact with Debt Issues - YOU HAVE NO REASON TO USE A FEE PAYING DEBT MANAGEMENT COMPANY- THEY CANNOT DO ANYMORE FOR YOU THAN THOSE LISTED IN MY LINK ABOVE.

All information given by myself is offered informally and without prejudice - if in doubt seek help from a qualified and insured professional0 -

That agreemant is post may 2005, so is not a 'true copy' of what you would have signed in 1998, so they have not fulfilled your sec 78 request even allowing for the excuse of sec 3(2) of the Consumer Credit (Cancellation Notices and Copies of Documents) Regulations1983 so Next are still in default;)

The section MISSING PAYMENTS

Missing payments could have severe consequences and make obtaining credit more difficult. did not come into force until the amendments of the Consumer Credit (Agreements) Regulations 1983 where introduced on the 31 of may 2005Thats it, i am done, Blind-as-a-Bat has left the forum, for good this time, there is no way I can recover this account, as the password was random, and not recorded, and the email used no longer exits, nor can be recovered to recover the account, goodbye all …………. 0

0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.4K Banking & Borrowing

- 254.1K Reduce Debt & Boost Income

- 455K Spending & Discounts

- 246.5K Work, Benefits & Business

- 602.8K Mortgages, Homes & Bills

- 178K Life & Family

- 260.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards