Paying £2880 into pension when retired

Options

Comments

-

But she would still need "relevant earnings" of the necessary amount in the year she wanted to use the "carry forward".

It appears that your wife has no relevant earnings and hasn't had for the past five years.

She is limited to a pension contribution of £2880 net to a scheme offering "relief at source" - £720 tax relief would be added.

Thanks for the reply.0 -

What would happen if after the uplift to £3600 and you did not draw the money out straight away and the pension collapsed to say £2800,ie the same as you invested,if you take the whole amount out would you still be taxed on £2100 ( 75% of total )

I know this is a hypothetical scenario but even if you get the tax back but in theory you have earned £2800 against your taxable income but you started with this and have made no profit,sorry if this question does not make a lot of sense but was on my mind and do not know the answer.

Interesting question. I am startled that the small pension with my former employer has dropped around 5% in value in three months. How do people investing £millions keep their nerve?You could open a SIPP. You could contribute £2880 before 6 April.

The tax relief will be added in May.

You could take the PCLS and draw down the balance monthly - drawing down the balance would trigger the MPAA.

You will have crystallised this pension.

If you transfer the CM/SW pension into the SIPP, you could take the PCLS tax free and draw down the pension monthly - this pension is then crystallised.

You could continue to contribute a net £2880 a year until age 75 even if you have no relevant earnings.

If you get a job and the employer offers a pension remember that if you have taken more than a PCLS from a DC pension, you are limited to a net contribution of £3200 per annum.

Having earned £18k and contributed only £450 into my DC pension this year, can I not put in as much as I dare before 6 April (of my small redundancy payment), then a maximum of £2880 in 2018-19 if I am not working or on a very low income?

Does the transferred DC pension go into a new SIPP that is separate from the one I started with my own money, or are they combined? If I open a SIPP before 5 April with a deposit from my bank account and it would be held by HL as cash, a proportion of it could be moved into a drawdown SIPP. When the DC pension transfers in to them I guess it will need to be invested, not held as cash, regardless of whether I draw any of it, but where exactly would HL place it? Do I have to tell them where I want it to go? And do HMRC find out all they need to know from HL regarding the source of funds for any SIPPs?

Thank you again. Perhaps too many of my concerns are outside the scope of this particular thread, which I have read from beginning to end at least six times and am still putting the puzzle pieces in place.0 -

can I not put in as much as I dare before 6 April (of my small redundancy payment),

This was covered earlier in the thread (post 576/579).

HL are very helpful on the phone - you might try early in the morning of 3rd April?0 -

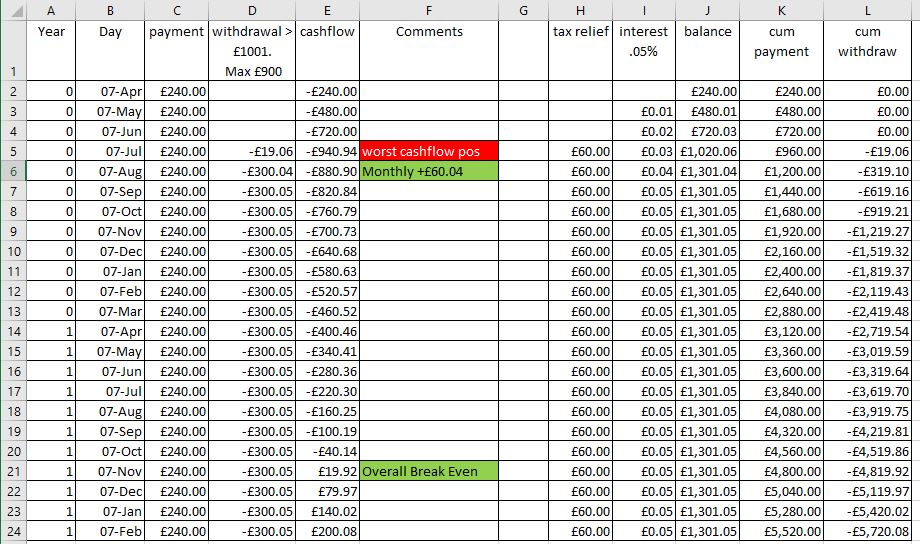

A surprising number of seemingly well off people I speak to about the £720 PA benefit of paying in £2880 a year into a SIPP seem reluctant to follow up on it due to not having a spare £2880 to lock away for many months.

I got to thinking about a perhaps more palatable approach which requires a smaller initial investment and is based on a more simple - pay in £240 once a month and get £300 back in a few days.

For a person with the following financial attributes

1. Over 55 and under 75

2. At least £3,600 available tax free allowance (Income < £8000)

3. No expection for future pension contributions above the MPAA £4k level

4. No other ongoing pension contributions

Simple process to follow

1. Open a HL SIPP with £240 and setup a regular monthly payment of £240

2. Once a month check the balance - if it is greater than £1001 UFPLS drawdown the excess - after a few months this should settle down to be about £300.

Not sure if the withdrawals can be automated with HL without regular cystalisations.

If my calculations in the attached sheet are correct

1. The £60 monthly profit should be available from month 5

2. Month 4 is the worst cashflow position with the net downside being about £940 - which is quite a bit better than £2,880

3. By Month 19 there should an be overall cash profit outside of the SIPP

This is based on using a HL SIPP, with the following constraints

1. Direct Debit payments leave your bank account on the 7th of each month

2. Best to keep balance above £1000 to avoid HL closing the SIPP

3. Tax relief timescale about 3 months

4. Lump sum withdrawals taking 5 working days.

5. No fees other than a £25 closure fee at age 75 - when the remaining £1000 is taken out.

6. Interest rate on cash 0.05%

There are obviously various optimisations to the process that could be applied - but I thought it was best to just keep it simple. 0

0 -

Arranging drawdowns monthly sounds like a significant administrative pain though, for the individual, but perhaps more pertinently for HL - perhaps a sure fire way to tip the balance for them to close this non profitable (to them) option...:o0

-

^^^^^^^^^^^^^^^^^

Noooooooooooooo!0 -

Sorry if this has been asked before but there are 31 pages and after a while I found myself skim reading so may have missed it.

All the posts I read about this suggest opening a new SIPP each year. Can you not use the same one each year?

Also, if you invest the £2880, get the tax uplift, can you take out £900 (25%) without affecting your MPAA?

Finally, assuming I can do as above and pay in the £2880, withdraw the 25% can I pay £2880 next year in to the same pension fund, and be entitled to 25% TFLS on that amount?

Thanks0 -

Interesting reading, im 66 would it make sense to make a payment of £2880 each year plus the £720 tax into the same fund and draw when I!!!8217;m 75.

Thanks0 -

Depends on your tax situation I would think.if you are not paying any tax then it makes sense to drawdown enough taxable money to use for full tax allowanceNo.79 save £12k in 2020. Total end May £11610

Annual target £240000 -

Yes, is the simple answer.Interesting reading, im 66 would it make sense to make a payment of £2880 each year plus the £720 tax into the same fund and draw when I!!!8217;m 75.

Thanks

Depending on your tax situation; how much taxable income you have, what account operation restrictions your SIPP provider may impose, you may be able to withdraw most/all each year.Personal Responsibility - Sad but True

Sometimes.... I am like a dog with a bone0

Categories

- All Categories

- 343.2K Banking & Borrowing

- 250.1K Reduce Debt & Boost Income

- 449.7K Spending & Discounts

- 235.3K Work, Benefits & Business

- 608.1K Mortgages, Homes & Bills

- 173.1K Life & Family

- 247.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 15.9K Discuss & Feedback

- 15.1K Coronavirus Support Boards