We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

I think it's time I joined DFW...

Andos_2

Posts: 38 Forumite

I am not entirely sure what help this may be; however, just talking about the situation I am in might help, even just a little bit - it's got to be worthwhile.

I have come to the realisation that I do have a problem with my debt situation. A week or so ago, I found myself feeling defeated and calling a company for what I thought was a debt consolidation loan - only to be told that my situation is TERRIBLE etc and I can't afford to live and DMP is my only option.

Now, I have always, always said I wouldn't go down that route - I personally find DMP morally wrong in that it means not fulfilling the credit agreement you have agreed to with your creditors.

The company DFH Financial Solutions, did seem very helpful and made everything seem so easy - £280 a month, debt all gone in 4 years... etc etc

Admittedly I almost went through with it until I came on here and did some research on that very company (thankfully) and obviously swiftly told them I changed my mind.

So here, I am now still in the same boat... I have a salary of about £21000. And my debt accumulates to approximately £12000.

Halifax Loan £7000 (£173 per month)

Halifax Credit Card £2800 (Pay about £150 a month then use it again)

Halifax Overdraft £1500 (£30 per month)

Creation Financial Services (Curry's) £500 (£45 per month)

Wonga loan £300 (Recurring ave of £50 per month)

So, yes, I now have all the above costing me approximately £450 per month and I am ready to fight back and get that debt gone as much as I can.

The problem I am having is...

Obviously - in an ideal world, a £12000 loan, paid over 4 years of £300-350 would be perfect and I could easily do this.. However, no-one is going to give me that, without the 100% knowledge that the loan will be paying everything else off.

My credit score is apparently bad; however - I have never in the last few years missed a payment, always made them on time or early and no CCJ's or anything like that.

Yet I still find myself here, helpless with no money every month, using payday loans to fill the gap and struggling.

Can anyone else relate? What do I do?

I have come to the realisation that I do have a problem with my debt situation. A week or so ago, I found myself feeling defeated and calling a company for what I thought was a debt consolidation loan - only to be told that my situation is TERRIBLE etc and I can't afford to live and DMP is my only option.

Now, I have always, always said I wouldn't go down that route - I personally find DMP morally wrong in that it means not fulfilling the credit agreement you have agreed to with your creditors.

The company DFH Financial Solutions, did seem very helpful and made everything seem so easy - £280 a month, debt all gone in 4 years... etc etc

Admittedly I almost went through with it until I came on here and did some research on that very company (thankfully) and obviously swiftly told them I changed my mind.

So here, I am now still in the same boat... I have a salary of about £21000. And my debt accumulates to approximately £12000.

Halifax Loan £7000 (£173 per month)

Halifax Credit Card £2800 (Pay about £150 a month then use it again)

Halifax Overdraft £1500 (£30 per month)

Creation Financial Services (Curry's) £500 (£45 per month)

Wonga loan £300 (Recurring ave of £50 per month)

So, yes, I now have all the above costing me approximately £450 per month and I am ready to fight back and get that debt gone as much as I can.

The problem I am having is...

Obviously - in an ideal world, a £12000 loan, paid over 4 years of £300-350 would be perfect and I could easily do this.. However, no-one is going to give me that, without the 100% knowledge that the loan will be paying everything else off.

My credit score is apparently bad; however - I have never in the last few years missed a payment, always made them on time or early and no CCJ's or anything like that.

Yet I still find myself here, helpless with no money every month, using payday loans to fill the gap and struggling.

Can anyone else relate? What do I do?

0

Comments

-

Hi Andos and welcome

You have come to the right place - and well done for not going through with the fee charging company.

I disagree that a DMP is morally wrong - its right in some circumstances, but always best to use a free provider.

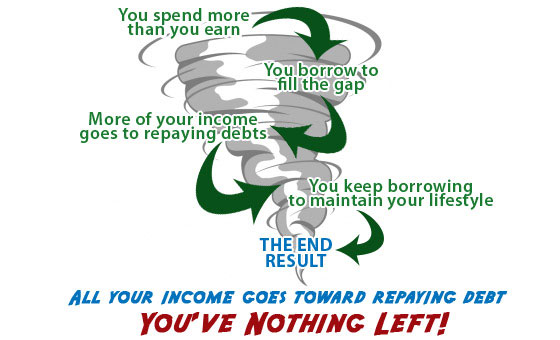

So looking at your pic - the first step is to stop spending more than you earn, and from that you can start to get on top of things.

Have you been through all your expenses to look at what you could reduce? I'd recommend posting up a statement of affairs so people can help you find savings/cutbacks you could make as a starting point.

Then you need to tackle your debts in the correct order - paying off the most expensive first. That wonga loan is obviously a killer for you - so first task will be to find a way to pay that off. Thats from a combination of cutbacks, maybe 1 or 2 very frugal months and perhaps you could find some old possessions you could sell or other ways to boost your income to hep you clear that £300?

Once the first debt is gone it becomes much easier to 'snowball' to clear your debts off in the most efficent way.

Statement of affairs calculator here - http://www.makesenseofcards.com/soacalc.html

and snowball calculator on the same site.A smile enriches those who receive without making poorer those who giveor "It costs nowt to be nice"0 -

Thank you Tixy, I'll have a go at that later.

Thankfully, a god send - My company have sent me to London to work for 5 days this month and therefore are paying me an extra £50 a day for that inconvenience.. I WILL pay that payday loan off this month and WONT be taking another one out! (This is my first committment)

Payday loans are the DEVIL.

Re: DMP's - It all seemed so good until they said I had to start a new bank, cancel direct debits etc and it just felt as though I was quitting on the creditors and myself for some reason (and I've never been one to quit)0 -

Thank you Tixy, I'll have a go at that later.

Thankfully, a god send - My company have sent me to London to work for 5 days this month and therefore are paying me an extra £50 a day for that inconvenience.. I WILL pay that payday loan off this month and WONT be taking another one out! (This is my first committment)

Payday loans are the DEVIL.

Re: DMP's - It all seemed so good until they said I had to start a new bank, cancel direct debits etc and it just felt as though I was quitting on the creditors and myself for some reason (and I've never been one to quit)

That's a stroke of luck! Welcome to the board. Tixy has given you some good advice. A spending diary would also help you find out where all you money is going. I find Martin's demotivator tool helpful. You key in how much you spend a day/week/month for a particular expense eg coffees or lunches at work and it calculates how much you would spend over the year in that area and how long you would have to work to pay for it.

Good luck with you debt-free journey!0 -

I have also just recently committed to a Sunday job - My mate owns a fruit market and so I am helping do that. Only £70 every other Sunday but every little helps.

")

I need to become obsessed with saving money... This is the place for that right??0 -

-

Situation this month...

Income

Work 1,343.00 standard wage

& London 200.00

TOTAL 1,543.00

Outgoings (Split with girlfriend so below is what I pay)

Rent £312.50

C/Tax £53.50

Water £22.50

TV £6.50

Sky £39.00

Gas £0.00

Electric £0.00

Car Ins £27.50

£470.00

My personal Finances

Wonga£300.00

Loan £173.00

P/Bill £42.00

Laptop £45.00

Halifax £10.00

Overdr £30.00

Credit Ca £100.00

Gym £0.00

Savings £0.00

£700.00

This means Rent/Bills and personal finances =

£1,170.00

£373.00 for the rest of the month including topping up car diesel and buying food

Food £120.00

Diesel £50.00

£203.00

Spending for the rest of the month...

Does anyone split their remainder money into 4 piles? so their money lasts... It's something I think I should do.

ON A SEPERATE NOTE; I am currently banking at Halifax where all my debts are...

Should I be changing banks???0 -

Hi Andos.

My first thought is - do you need Sky tv? does your package include internet etc? can you change to a cheaper package? We've actually kept Sky despite our debts because we got a good deal on internet/phone with them (Hubby thraetened to cancel, doesn't always work) and we vowed to watch more movies and go out less. I know a lot of people advise getting rid of it though.

Cetainly splitting your moeny and allowing yourself a weekely budget can work IF you stick to that weekly budget (something I'm still practising to do)

People also recommend not banking where your debts are but I've no experience of this to advise you.

Finally, search these forums for all the advice you can. There are threads to help you up your income, save money, support you - it's a fab place to be and has helped me no end.

Good luck!0 -

The Sky is for a box upstairs and downstairs/internet and phone...

Whilst I appreciate it is high - I do actually believe it saves money in the long run as a night in with a film is cheaper than a night out to the movies. (Obviously this only applies if we don't actually go out)

I have never split my money, but I am definitely considering it as each month I find myself spending anything I have before the 2nd week of the month.

My objectives over the next month are:

-Work Sundays for extra money

-Pay off my payday loan and by;

-spreading my spending over 4 piles of weekly amounts; hopefully not taking out another.

I think this is a good starting point for myself and I thank all your input... Just by writing those 3 things down, it helps me appreciate it as an ACTUAL target as opposed to something I'll consider doing in my head.

I shall let you know if I am successful.0 -

Add to that - I have been decluttering, listing all my clothes I don't use on ebay. 0

-

Well done on the targets and good luck with them.

You have nothing down for gas or electric, is that because someone else pays for that? Also if you have a car you need to budget for maintenance, road tax & MOT. How about other insurance, TV licence, (or was the £6.50 your half of that?), xmas, birthdays, haircuts etc.CCs @0% £24k Dec 05 £19,621.41 Au £13400 S 12600 Oct £11,981 £9481 £7500 Nov £7250 D £7100 Jan 6950 F £5800 Mar£5400 May £4830 June £4660 July £4460 Aug £3200, S £900, £0 18/9/07 DFW Nerd 0420

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards