Early-retirement wannabe

Comments

-

Personally I'd be very cautious about having a significant amount of my wealth in P2P lending.

It's relatively new and I would be concerned how it would cope during a substantial downturn. You're also putting a large degree of faith in the credit worthiness checks. I think the innovation is great but it has someway to go until I would be convinced it stacked up well against other forms of investing.0 -

-

settingsun wrote: »Excluding my home, my pension pots /sipp would be about 60%, isas about 10%, florida property 10%. This leaves about 20% for p2p. If the p2p was diversified across different platforms as Jamesd suggests that should be a starting point for a plan.

What to do with the pension pots is a bigger concern. Currently a mixture of funds as originally set up by default and low cost trackers.. The isas are mostly fts100 shares with a focus on dividends. Hey but that's another story altogether.

If the p2p lending that you choose is secured on property, this will increase your exposure to property as a whole (although the p2p will likely be against commercial property).0 -

LOL, that's probably because I noticed the interesting potential for some of the secured VCT options and think them worth mentioning vs P2P lending due to the better tax relief. FWIW I roughly doubled my own VCT holdings a couple of weeks ago, part of working to have nearly zero income tax due this tax year, like last, and to get those secured investments.TheTracker wrote: »You get much the same results with a simple search for VCT!0 -

According to a Nesta and Cambridge University's Pushing boundaries: the 2015 UK alternative finance industry report property was about £700 million of the total 3.2 billion in P2P lending and crowdfunding in the UK in 2015. About 1.1 million total lending/investing participants in the year. So lots of property but also lots of non-property.If the p2p lending that you choose is secured on property, this will increase your exposure to property as a whole (although the p2p will likely be against commercial property).0 -

My latest figures seem to show I'll have £300k pension and £53k cash at 57 in 4 years or £380k and £ 80k at 60 in 7. Would prefer to go at 57 but don't think it will be achievable.0

-

Got a tiny pay rise, the most exciting part is seeing my pension contributions going up by £5/m. Thought of this thread

0

0 -

2015/16 update...quick recap...myself and partner both aged 38 now, plan is to retire by about age 45, go travel for about 3 years then return and retire in countryside somewhere...no kids, no intention to have any, both work full-time.

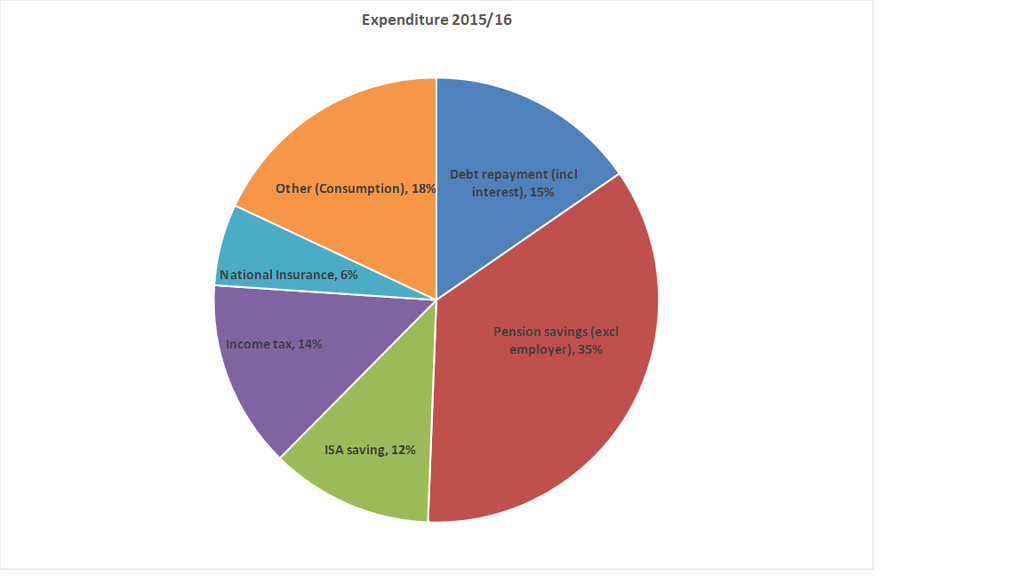

The year was quite dull financially, the most surprising thing being that we consumed less in the year than in 2014/15 despite replacing our car. That has improved the long run position, as future needs are based on current expenditure patterns. Chart below shows 2015/16 expenditure allocation:

Most of debt repayment is mortgage, and most of the slice is mortgage overpayment. In addition to our own pension savings, both my wife and I have occupational Defined Benefit pensions, so get decent employer contributions into those.

Sadly 2015/16 was the last year I will be contributing into a SIPP for a while, as we are approaching having enough pension resources. So the income shown below from my personal pension will be a bit lower than shown. This is because the big risk now is over saving into pensions . My wife has less pension income than I do (although still plenty to cover personal allowance), so we'll keep contributing to that pension for a while yet to remove higher rate liability for her, plus the defined benefit pensions, plus some additional voluntary contributions into another defined benefit scheme which is very valuable (so still lots of pension saving...).

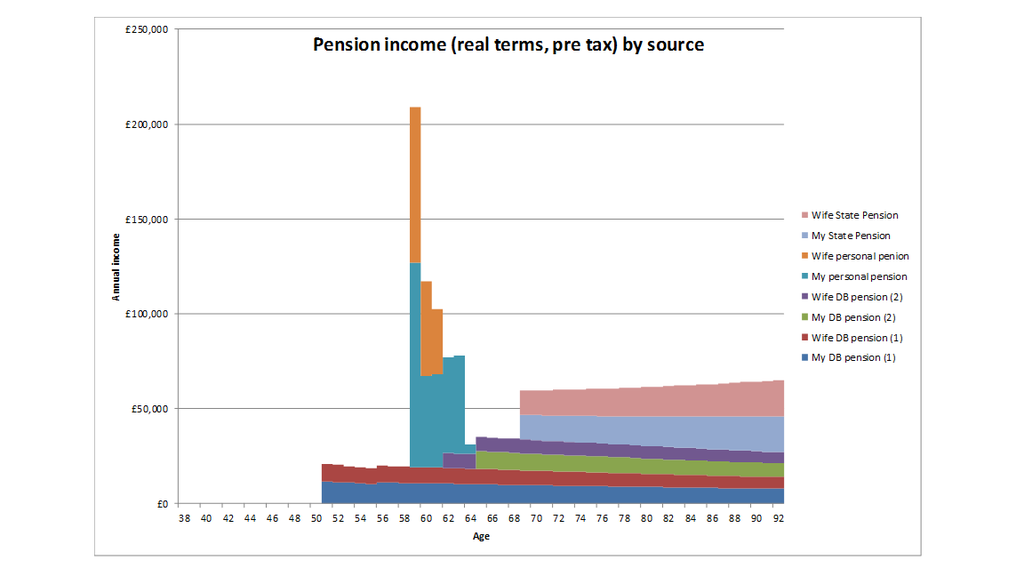

The hardest time in the future will be as we approach age 58, which is the earliest age I assume we will be able to access personal pensions (the pensions being shown from age 50 have protected minimum pension ages from 2006 changes, I have a strong incentive to take them early as I will have nil taxable income, and it significantly reduces their value for Lifetime Allowance purposes). Hence although pension contributions still have a lot of value, the pattern of income they generate doesn't work well for me, as I have a strong preference for pre-58 income. Things such as mortgages or raising money on interest free credit cards may well work, but as I will be returning from travelling I cannot rely on that.

Chart below shows projected pension income, assuming retirement in April 2023, minimal change from last year:

As I will now have higher rate liability due to not making SIPP contributions I have more of an incentive to work less. Fortunately in 2017/18 a great opportunity has come up to go on a three-month trip. Plan is to use up annual leave for a couple of months and take just under a month of unpaid leave. That will all be higher rate income lost, so the trip is effectively subsidised, sort of. Hopefully that can all be lined up with employer given how long in advance I can sort it all out.

One very useful policy development is the launch of the Lifetime ISA. I purchased our current house solely in my name anticipating a future Govt. would offer something very worthwhile to first time buyers, so my wife still has first-time buyer status, and will be slightly under 40 when LISAs are launched. Hence she has opened a Help to Buy ISA which will be moved into a LISA in due course, and we will make maximum contributions to the LISA every year. This is great, as when we are travelling we will still be getting the relief. Then when we return we can access the LISA to buy our retirement home. I'll need to review the rules of the LISA carefully regarding first time buyer definition, but I think it will all be fine looking at rules on help-to-buy ISA.

So a good year, projections largely unchanged, but due to keeping consumption down in particular the plan is in a better position that it was forecast to be this time last year and retirement in 2023 is now looking more of a backstop, with an earlier date probable - especially if something like voluntary redundancy gets offered at a convenient time for one of us.0 -

Hello Hughekevi, you are looking very solid for the future. Keep up the good work.

I am assuming you are both in good health and care about your health. Sod's law always has a part to play in any plans one has.

Good luck.There will be no Brexit dividend for Britain.0 -

I am assuming you are both in good health and care about your health.

Both of us are in good health, so focus is on maintaining that.

This happens to go hand-in-hand with keeping costs down. For example, we both make all our own food (so no spend on food at work) and cycle to work (saving thousands on public transport - we live in London).

Both of us also are not pursuing career advancement - the financial rewards are outweighed by the greater workload, responsibility, etc. We do not need the additional money - even if we both took promotions to the next career level it would only bring forward financial independence by about a year or so (ie changing from 7 years currently about 5-6). I'd far prefer 7 years of stress-free work than 5-6 years of hard work, particularly when I'd be paying large slices of tax on the additional money.Sod's law always has a part to play in any plans one has.

Risk of low probability, high impact events has always been a key consideration, particularly as we have high percentages of wealth in pensions we cannot access (although in the event of ill-health we could of course, and whilst we are still working the Defined Benefit plans would be significantly enhanced in the event of serious ill health).

Now I am past the early part of the plans, security against these type of events is much higher. Quite a large number of the risk scenarios I used to track I have removed, as the risks are no longer an issue should they materialise.

Of the risk scenarios I still track, if we were both made redundant we would be able to pay off mortgage and all debts and still have several tens of thousands available and be able to retire at age 58 without any further pension saving.

Alternatively, we could now afford to purchase our retirement home with no mortgage/debt, and be able to retire at 58 with no further pension saving. Given we have no children, our income needs are not extravagant so we could easily survive even with low wage jobs.

As each year passes between now and 2023, we get noticably more secure in our financial position, until becoming fully financially independent in about 2023.

Knowing the risks faced are small and diminishing in itself is good for health, as it leads to lower stress, etc.

Also worth noting that ill-health is more likely to affect individuals the older they are - as we don't plan to be working in our 50s, the chance of that derailing plans is reduced.0

Categories

- All Categories

- 343.2K Banking & Borrowing

- 250.1K Reduce Debt & Boost Income

- 449.7K Spending & Discounts

- 235.3K Work, Benefits & Business

- 608K Mortgages, Homes & Bills

- 173.1K Life & Family

- 247.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 15.9K Discuss & Feedback

- 15.1K Coronavirus Support Boards