Vanguard life strategy

Comments

-

The Vanguard US site shows how US Lifestrategy equivalents have done over the last 10 years. Although they don't have a 100% equity fund.0

-

The Vanguard US site shows how US Lifestrategy equivalents have done over the last 10 years. Although they don't have a 100% equity fund.

That's quite useful to give some context to the very high performance that resulted from the particular economic conditions experienced in the last few years by a GBP investor with high equities and high US allocation.

As you say, the US VLS page doesn't list a 100% equities version but the most aggressive one, "growth" is 80:20 equities to bonds.

The return for that over the last decade to August, a ten year economic cycle, including a major crash and some mini crashes and corrections, was a little under 5% annualised.

Compare that to the UK VLS80 over last five years which produced almost 80% return or something like 12.5% annualised for that period.

And then consider, if it might only be going to deliver on average 5% over the decade (and bear in mind that it could be worse than that), but in the first five years it already delivered +80%... how much of that will you have to perhaps "give back" to finish in line with your revised expectation for the decade.

As financial advisors like dunstonh are fond of saying, in investing it is not one way traffic - you get up years, down years and sideways/ nothing years. VLS will have given five or six good years in a row for an investor buying in at launch.

If the UK product had existed and they'd' been able to invest a couple of years earlier that would probably be seven or eight good years. To assume or even hope that would continue, rather than taking the turn of having the bad years or nothing years, is pretty naive. The 10 year return from the US product history tells the story of what you might have to accept.

Granted, ten years ago was a market high so the performance might look worse than a long term average. However, it's more blinkered to put your head in the sand and exclude the massive 50% credit crunch crash, than to just accept it as something that could and will happen at some point if you have a high-equity portfolio.0 -

Thank you exactly what I'm looking for, going by that the VLS100 has consistently went up over the last 5years. I know it might be different over the next 5 years but all good so far

Thats because thats whats happened to global stockmarkets. Its nothing to do with Vanguard.

If you want a fund that goes up every year you should not invest in an index fund.0 -

AnotherJoe wrote: »Thats because thats whats happened to global stockmarkets. Its nothing to do with Vanguard.

If you want a fund that goes up every year you should not invest in an index fund.

Then perhaps by extension, one should not invest at all??

Generally, returns from stock markets has performed better than cash in the long term, even accounting for volatility. The case is for adequate risk management to account for the volatility of markets and expectations of the investor.

Save 12K in 2020 # 38 £0/£20,0000 -

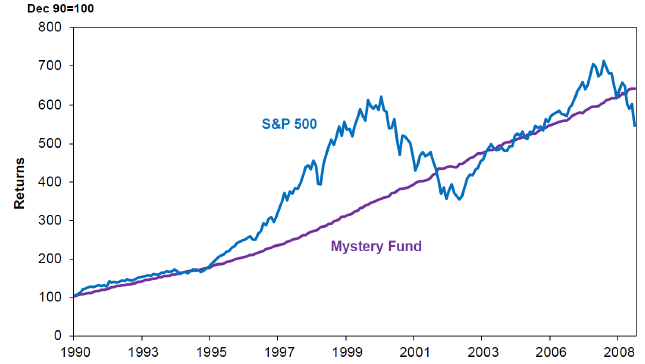

AnotherJoe wrote: »If you want a fund that goes up every year

... then should you invest in this mystery fund:

?

all is revealed in this article: https://www.advisorperspectives.com/commentaries/2013/12/05/no-silver-bullets-in-investing

but, basically: if it looks too good to be true, ...Then perhaps by extension, one should not invest at all??

either that, or get used to the idea that your fund will go down in some years, and learn to live with it. you don't have to like it, but you do need to live with it (i.e. not panic-sell after a crash).0 -

Then perhaps by extension, one should not invest at all??

Generally, returns from stock markets has performed better than cash in the long term, even accounting for volatility. The case is for adequate risk management to account for the volatility of markets and expectations of the investor.

Indeed you shouldn't if like the OP you are under the severe misapprehension that a fund that rose every year of the last five gives an indication that's what it will do for for the next 20, or thinks that an index fund does anything other than follow its index, so you should investigate the index(es) the fund is following.

The OP acts as if VLS is actvely doing something to create that performance when it's the exact opposite, it's the index that is doing the heavy lifting. So it's the indexes they need to investigate. Once they decide they like those indexes they can pick the lowest cost fund that follows that index. Whats the OP going to do when markets fall over months to years, if they are of such mind that they wouldn't invest if it fell last quarter ?0 -

@anotherjoe I never once said that I was looking for a fund that went up every year (although that would be nice) it was merely for me to see past performances and perhaps some reassurance.0

-

@anotherjoe I never once said that I was looking for a fund that went up every year (although that would be nice) it was merely for me to see past performances and perhaps some reassurance.

If you are looking for reassurance, are you sure VLS100 is the right fund for you?

How reassured are you going to be when it next loses half its value?I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

@ duntosh maybe I worded that wrong I am aware of the risks and perfectly prepared to lose half the the value. This may change the more I have in it but as I have said before I am in this for 20 plus years.0

-

@anotherjoe I never once said that I was looking for a fund that went up every year (although that would be nice) it was merely for me to see past performances and perhaps some reassurance.

Your started off by saying that you wanted to look at last months performance to decide if you should double your investment for the next 20 years.

Then you said you were reassured by the fact it went up for 5 years but if course it did because the markets did.

You still don't seem to understand that the performance of this fund is a direct reflection of the stock markets it's invested in. It's performance is not affected by management decisions in contrast to a fund managed by Smith or Woodward.

You may have some reassurance because it's gone up over 5 years but that's nothing to do with Vanguards management and it's false reassurance based on a llack of understanding. . It's all amd oniy to do with the markets. When the markets fall (which they will) so will this fund.

I'm not saying that's a bad thing but you seem to think that because the markets went up 5 years In a row they will continue to do so.0

This discussion has been closed.

Categories

- All Categories

- 343.2K Banking & Borrowing

- 250.1K Reduce Debt & Boost Income

- 449.7K Spending & Discounts

- 235.2K Work, Benefits & Business

- 608K Mortgages, Homes & Bills

- 173K Life & Family

- 247.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 15.9K Discuss & Feedback

- 15.1K Coronavirus Support Boards