Any point in a Cash buffer in Pension Drawdown Account?

Options

Comments

-

As well as UK equities and bonds, my income portfolio includes global equity funds and an Asian equity fund. The yield is just below 4%, and would be higher if you invested in these funds now as the capital values have fallen a bit with the recent correction.You may get approaching 4% from a balanced portfolio of UK equities and bonds, but if you want a global portfolio, you would struggle. It CAN be done but only by selecting high dividend payers, which usually implies low growth, or ITs paying income from capital (like EAT).

Possibly, although my income portfolio with less than 60% equities has similar total returns over the last 3 and 5 years with the VLS60 and HSBC Global Strategy Balanced funds which I also hold. I'm not sure which will fare better going forward, but the thing I like about the income funds is that they should continue to produce dividends of up to 4% of my original investment increasing with inflation, even when the capital is volatile. I would be more wary about drawing 4% from the VLS60 in loss years by selling capital, as I think you are more likely to deplete the growth fund balance if you have a bad run of loss years early on, than if you were just taking dividends and not touching the capital. Do you and others agree?Anyhow my point is, you sacrifice total returns for income.

I agree, and that's why I steer clear of the maximiser/high income funds with yields of 6% and 7%.Compare pretty much any high income fund with their corresponding 'regular' fund and see the difference..0 -

Depends on the term I guess, index linked gilts are around 2.5%...about the same.No; versus CPI it's about -0.5%.

Nor does it much matter because in the UK (unlike the US back then) it's easy to buy an index-linked annuity which would probably do a better job than a ladder of I-L gilts.

Point is that they used an example where a rock solid safe option beats the oft quoted 4%. Not possible now, in the UK at least.Anyway, that's two commenters I've seen who've missed the point. Any more?0 -

Depends on the term I guess, index linked gilts are around 2.5%...about the same. Point is that they used an example where a rock solid safe option beats the oft quoted 4%. Not possible now, in the UK at least.

Except that there's no good reason to suppose that the 4% is going to be achieved in the UK. There's no point changing one side of a comparison and leaving the other side unchanged if you suspect that both sides are/were/will be governed by ZIRP and QE.Free the dunston one next time too.0 -

Bond/gilt yields tend to move with interest rates, dividend yields and share gains don't. So the current very low interest rates lead to low bond yields, they don't necessarily lead to low share yields.Except that there's no good reason to suppose that the 4% is going to be achieved in the UK. There's no point changing one side of a comparison and leaving the other side unchanged if you suspect that both sides are/were/will be governed by ZIRP and QE.

Although personally I think 4% is over optimistic. And I agree with the implication of the article, that if you want a guaranteed income then a guaranteed investment might be a better idea, but I'm happy to adjust my spending depending on investment performance so am happy with a more volatile portfolio.0 -

Historic S&P 500 dividends ..

http://www.multpl.com/s-p-500-dividend-yield/

Those are not dividends, they are yields.Inflation adjusted.

http://www.multpl.com/s-p-500-dividend/

Just the job! Thank you very much.

(i) Do you happen to know: are these true dividends or are they adjusted for the modern tendency to buyback shares instead of distributing dividends?

(ii) Now all the punter has to do is wonder how much they'd be reduced by charges and taxes in his own particular case. For SIPPs and ISAs that would be pretty easy, I'd think.Dividend growth showing the effects of recent downturns.

http://www.multpl.com/s-p-500-dividend-growth

Pretty good. I wonder whether there's an inflation-corrected companion chart. Anyway, only a couple of episodes of negative nominal growth.Same chart in table form showing a 20% cut in 2009 which was reversed by 2011.

http://www.multpl.com/s-p-500-dividend-growth/table/by-year

Thanks again.Breakdown of S&P 500 ratios showing various time periods.

https://www.quandl.com/data/MULTPL-S-P-500-Ratios

Thanks once more.

Is it fair to say that real dividends have been erratic in the past (pre 1951, say), but less so recently? Except, I suppose, that "erratic" should cover upwards movements too so that after the Global Credit Crisis is also erratic.

Ignoring the era of the US Civil War and immediately afterwards, we've got the following pronounced leaps:

(i) Post-1900 (ii) The roaring twenties, (iii) The short-lived false dawn of the mid-late 30s (well done, FDR!), (iv) post-WWII, (v) post-2010 i.e. the era of ZIRP and QE.

I note that real dividends hardly responded to the bursting of the dot.com bubble. That's presumably because the companies in the most trouble had never paid dividends anyway.

There's nothing before 2010 that would encourage me to guess that the post-2010 leap will continue for long, but what's a guess worth?

I wonder what future historians will call the current era? I suppose that depends entirely on what happens next.Free the dunston one next time too.0 -

As well as UK equities and bonds, my income portfolio includes global equity funds and an Asian equity fund. The yield is just below 4%, and would be higher if you invested in these funds now as the capital values have fallen a bit with the recent correction.

Possibly, although my income portfolio with less than 60% equities has similar total returns over the last 3 and 5 years with the VLS60 and HSBC Global Strategy Balanced funds which I also hold. I'm not sure which will fare better going forward, but the thing I like about the income funds is that they should continue to produce dividends of up to 4% of my original investment increasing with inflation, even when the capital is volatile. I would be more wary about drawing 4% from the VLS60 in loss years by selling capital, as I think you are more likely to deplete the growth fund balance if you have a bad run of loss years early on, than if you were just taking dividends and not touching the capital. Do you and others agree?

I agree, and that's why I steer clear of the maximiser/high income funds with yields of 6% and 7%.

One thing missing......"growth" funds tend to take their charges from the income generated (to make the growth look better), whereas "income" funds tend to take them from the the capital returns (to make the income look better), so you often aren't really comparing apples to apples by just comparing fund yields.

Total return (after charges) is where it's at, at least imho.

PS, by growth and income I mean funds targeted toward that specific aim, I don't mean INC or ACC versions of the same fund.0 -

-

There's nothing before 2010 that would encourage me to guess that the post-2010 leap will continue for long.

About the remarkable leap in inflation-corrected dividends post-2010 i.e. post the Global Financial Crisis: I wonder, are companies simply distributing earnings (including share buybacks) rather than making capital investments? If so it bodes ill for future economic growth and future dividends.Free the dunston one next time too.0 -

About the remarkable leap in inflation-corrected dividends post-2010 i.e. post the Global Financial Crisis: I wonder, are companies simply distributing earnings (including share buybacks) rather than making capital investments? If so it bodes ill for future economic growth and future dividends.

This link is a 3 page summary.

https://seekingalpha.com/article/439171-has-dividend-growth-kept-up-with-inflation

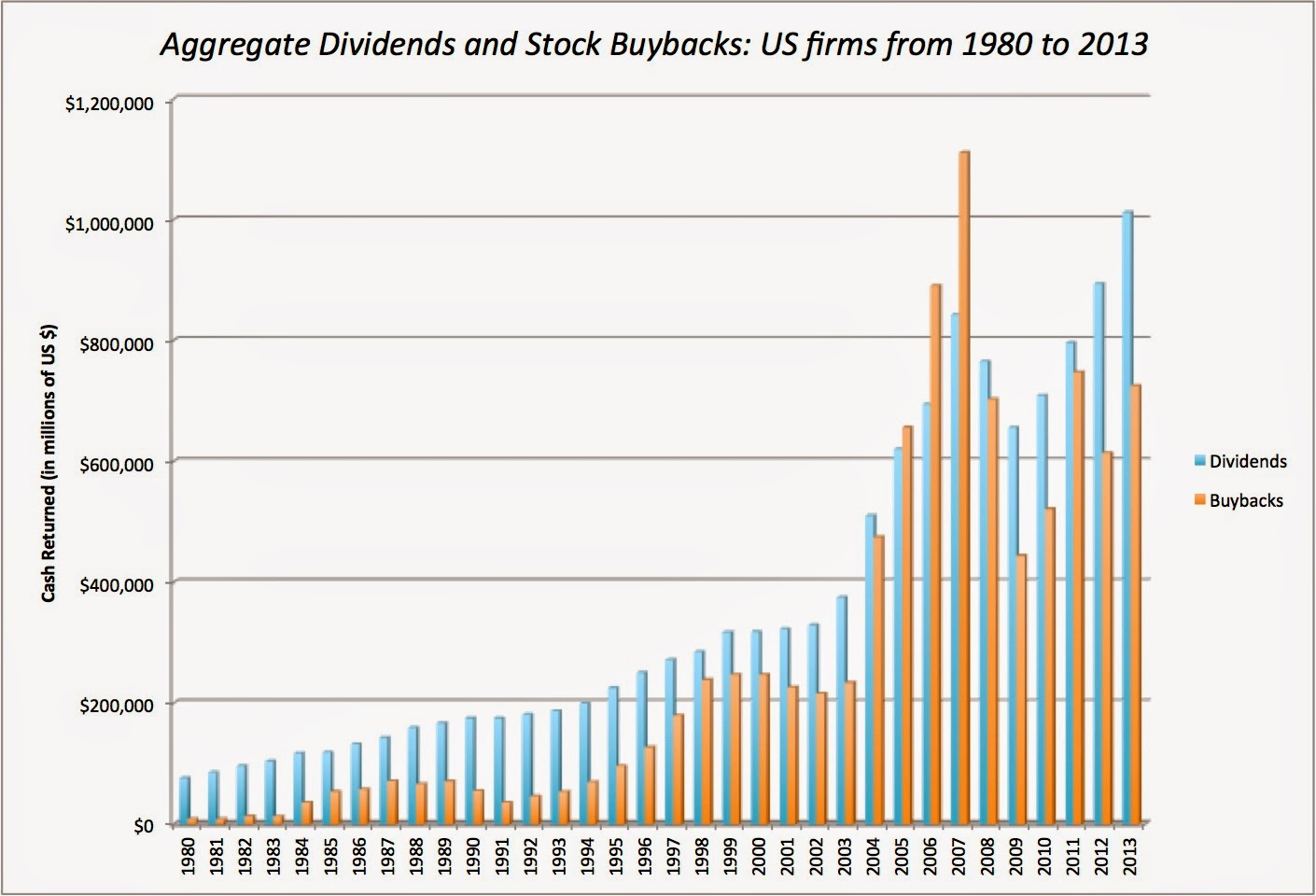

Looking at this it appears buybacks have been pretty solid since 1998.

http://2.bp.blogspot.com/-HxRg5f8YpE0/VB7XtHiJYDI/AAAAAAAABe4/juPlWmLXAVE/s1600/DivBuybackChart.jpg

https://www.globalbankingandfinance.com/are-share-buybacks-a-key-factor-in-the-continued-rise-in-us-equities/

Annuity link

http://www.pensionchoices.com/annuity-rates/index-linked-annuity-rates/0 -

But you have to assess your equity drawdown strategy against a valid comparator. The 'risk free' model they use if frankly stupid as a)it is, as indicated by annuity rates, way more expensive than they than claim, and b)it has a 100% shortfall risk if you live longer than the planned 30 years which I for one would find unacceptable!Except that there's no good reason to suppose that the 4% is going to be achieved in the UK. There's no point changing one side of a comparison and leaving the other side unchanged if you suspect that both sides are/were/will be governed by ZIRP and QE.

The only really sensible option to compare drawdown to is purchasing an index linked annuity as the sharing of longevity risk makes that the cheapest risk free way of getting lifetime income. It will always be the 'best in class' answer for a risk free portfolio - and if you aren't using a risk free option then you need to price in the risk. For the 4% to fail you generally need both a bad overall return and a bad sequence of returns. I agree that this is may have a higher probability than a random period in the past, but it's still pretty unlikely for a globally balanced portfolio.0

{kind=link}

This discussion has been closed.

Categories

- All Categories

- 343.2K Banking & Borrowing

- 250.1K Reduce Debt & Boost Income

- 449.7K Spending & Discounts

- 235.3K Work, Benefits & Business

- 608.1K Mortgages, Homes & Bills

- 173.1K Life & Family

- 247.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 15.9K Discuss & Feedback

- 15.1K Coronavirus Support Boards