We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Lloyds Bank brings fictional fraud to life?

Comments

-

Let me see.....flaneurs_lobster said:

I don't understand this comment.Analyst said:

The FOS did not even name our complaint in the decision, so the decision has no value.flaneurs_lobster said:So, in essence, you have a complaint with Lloyds Bank as to how they calculate the remaining balance on your mortgage.

Lloyds have rejected your complaint.

You have taken your complaint to the FOS and they have not upheld your complaint.

Are you asking for advice on how to take your complaint further?

EDIT : If you add the FOS Decision Reference then those who are interested might be able to comment further.

Could you confirm or otherwise that this is the FOS decision that you mention in your OP and that you claim has "no value"?

https://www.financial-ombudsman.org.uk/decision/DRN-5750324.pdf

Does that decision mention anything about a 5 year term increase being mathematically impossible, given the restraints of an offset mortgage?

Does it mention that that the first term reduction is out by a factor of 7?

Thought not.0 -

Here is a quote:Analyst said:

So what part of "they should instruct a professional" did you not understand? It is demonstrably true, using your example.flaneurs_lobster said:

Manifestly and demonstrably untrue.Also, the FOS will not accept any evidence without a paid for audit, so it is not the free service advertised.

If your case is indeed the one I identified in a previous post (you have not refuted that it is) then the FO decided that in your case...it is not the role of this Service to audit Mr and Mrs S’s mortgage account. If they wish for the account to be audited, then they should instruct a professional to complete this.The vast majority of cases referred to the FOS require no such audit (or the request for one).

“I should firstly say that it is not the role of this Service to audit Mr and Mrs X’s mortgage account. If they wish for the account to be audited, then they should instruct a professional to complete this. So, whilst I have considered all of the information provided by Mr and Mrs X, I will not be commenting on all of the calculations they have provided. I’ll focus on the matters that I consider most relevant to how I’ve reached a fair outcome in keeping with the informal nature of our Service.”

0 -

Here is an example from our third final letter:lfc321 said:Are you able to explain more clearly what you think has happened? I.e. mortgage balances, interest rate, offset balance, term remaining, monthly payments - and how these have changed over time. It’s not possible for any of us to evaluate your claim without these details - it’s too unclear what’s actually happened or what you think Lloyds has done wrong.I would certainly not rely on “AI” for stuff like this: even when it is correct (far from always) much will depend on precisely what you ask it.

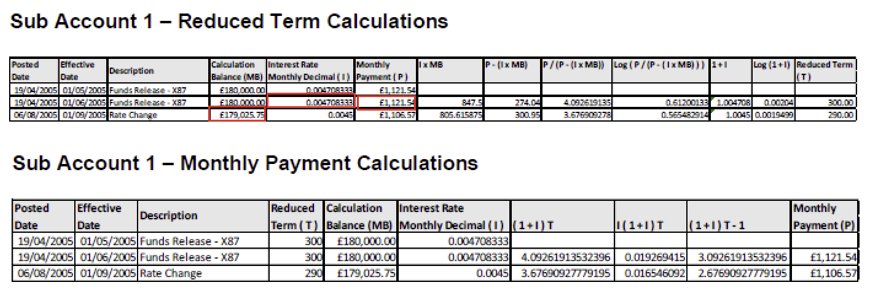

The first formula calculates the reduced term, and then that figure is used as an input to the second formula, to calculate the new monthly mortgage payment.

Lloyds Bank have “proved” they are correct by inputting the (as yet unknown) answer they want from the second formula (the monthly payment) as an input to the first formula (the reduced term). Naturally, if you input the wrong monthly payment, you get the wrong reduced term, and the two will match.

In this example, Lloyds Bank takes the unknown future monthly mortgage payment of £1,106.57 and uses it to “prove” that the reduced term is 290 months. A self-fulfilling outcome, and not a calculation at all.

The correct inputs are highlighted in red. It is the only monthly payment known at the time of the calculation, and the interest rate must match that monthly payment.

So

I X MB = 0.004708333 x 179,025.75 = 842.91284657475

P – (I x MB) = 1,121.54 – (I x MB) = 278.62715342525

P / (P – (I x MB)) = 4.025235825771326

Log(P / (P – (I x MB))) = 0.604791329

I + 1 = 0.004708333 + 1 = 1.004708333

Log(I + 1) = 0.002040004

log[ P ÷ (P - (I × MB)) ] / log(1 + I) = 296.4657564396933

which Lloyds Bank would round down to 296

0 -

If we return to the example I gave earlier, of the Financial Ombudsman blindly accepting, without question, whatever the bank tells them (kindly highlighted by flaneurs_lobster ).

That ignoring the upcoming monthly payment, causes a rise in the monthly payment when interest rates fall. Example decisions include, DRN-3305295 and DRN-5750324.

I noted, that simple logic tells you that something that happens all the time cannot explain an increase. If it is in the previous monthly payment calculation, and in the new monthly payment calculation, then it is not an explanation of a difference.

Well, the numerical example above, is the rare case where ignoring the upcoming monthly payment is done for the first time.

So, if we deduct the upcoming monthly payment from the balance, and calculate the remaining term again, we get an additional 4 month reduction in term. Which equates with a single monthly payment, compounding at the stated interest rate, for the calculated remaining term, as you would expect.

Naturally, if the term reduces, the monthly payment increases. So, in this example, Lloyds Bank’s policy of ignoring the upcoming monthly payment, has reduced the monthly payment. The exact opposite of the Ombudsman’s assertion.

The point I am making, is that we do not have to hunt for examples to fit a narrative. Lloyds Bank provides all the evidence we need, every single time they respond to a question. Our only issue, is we are getting tantrums of a two year old, rather than professional replies, most of the time.

DRN-3305295

DRN-5750324

The latter is such a word salad, that I very much doubt the Ombudsman understood what they were writing. Try finding the above extract, and see for yourself.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards