We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

NS&I 4.00% Guaranteed Growth Bond and 3.97% Guaranteed Income Bond

Comments

-

So you can log into the online service to transfer money from direct saver to premium bonds (and vice versa), but the same online system doesn't allow an online transfer from direct saver to guaranteed growth bond, but you can fill out a form? That's really odd! I've only recently opened an account with NS&I, and they seem to have several weird quirksBooJewels said:

I was wondering about that too. I don't have a DS - and was trying to avoid opening yet another account - I already have more than seem sensible. But the Direct Saver page states:km1500 said:"As I understand it, you only need to use the printed form if you want to transfer funds from another NS&I product, other than a Direct Saver. I want to move some from the Income Bonds I already have"

can you xfer income bonds -> DS and then to the bond ? You can definitely xfer PB -> DS instantly."Can I move money from another NS&I account to a Direct Saver?

Yes! Just fill out a quick online form and we’ll get it sorted for you. Be sure to have the details of the account you want to switch from to hand."

If you want me to definitely see your reply, please tag me @forumuser7 Thank you.

N.B. (Amended from Forum Rules): You must investigate, and check several times, before you make any decisions or take any action based on any information you glean from any of my content, as nothing I post is advice, rather it is personal opinion and is solely for discussion purposes. I research before my posts, and I never intend to share anything that is misleading, misinforming, or out of date, but don't rely on everything you read. Some of the information changes quickly, is my own opinion or may be incorrect. Verify anything you read before acting on it to protect yourself because you are responsible for any action you consequently make... DYOR, YMMV etc.0 -

I think you can move funds from a Direct Saver to other accounts, including the two new Fixed bonds - but not directly from Income Bonds and Premium Bonds.

I have the latter two accounts and can seemingly transfer between them, but not to anything else. I don't have a Direct Saver. It looked like I could open one and transfer funds from the IB account, but working through the links for that process brought me to a similar form to print out and post - so was no advantage.

Yes, it all seems very odd and some of it contradictory.1 -

No, you can do Direct Saver to Guaranteed Income/Growth Bonds online but the issue is it can’t be funded from Income Bonds without using a form. But agree odd!ForumUser7 said:

So you can log into the online service to transfer money from direct saver to premium bonds (and vice versa), but the same online system doesn't allow an online transfer from direct saver to guaranteed growth bond, but you can fill out a form? That's really odd! I've only recently opened an account with NS&I, and they seem to have several weird quirksBooJewels said:

I was wondering about that too. I don't have a DS - and was trying to avoid opening yet another account - I already have more than seem sensible. But the Direct Saver page states:km1500 said:"As I understand it, you only need to use the printed form if you want to transfer funds from another NS&I product, other than a Direct Saver. I want to move some from the Income Bonds I already have"

can you xfer income bonds -> DS and then to the bond ? You can definitely xfer PB -> DS instantly."Can I move money from another NS&I account to a Direct Saver?

Yes! Just fill out a quick online form and we’ll get it sorted for you. Be sure to have the details of the account you want to switch from to hand."

2 -

You’re welcome, glad to helppoppystar said:Great, thanks Galactica - that’s what I suspected but it’s good to see it so clearly.") 0

0 -

Ned... Could you give some examples of money market funds... Or point me towards a list...NedS said:

Do you specifically want to hold NS&I products in a SIPP, or do you just want any risk free 4% return for cash in your SIPP? If it's just the latter, there are money market funds that will give you near BoE base rate at very low risk, or if you prefer a fixed rate product, consider individual government gilts (although not yet yielding 4%)Ciprico said:Any one know of a SIPP that can hold these NSI products...

It seems Interactive Investor don't, but do any of the major platforms....

From: https://www.nsandi-adviser.com/sipps-and-ssassSIPP and SSAS schemes may allow investment into some NS&I products. These are known as ‘permitted investments’ held by the scheme trustee. Before recommending NS&I investments we suggest you check that the SIPP or SSAS provider will accept them, and that the investment will not be subject to tax penalties on any gains.

Our investments that may be held in a SIPP or SSAS are:

- Fixed Interest Savings Certificates

- Index-linked Savings Certificates

- Guaranteed Growth Bonds

- Guaranteed Income Bonds

- Income Bonds

Thanks...0 -

Funds showing on DS but when I try to transfer to GB it shows DS as zero balance. I just opened and placed funds yesterday so guessing tho showing, won't be transferable until tomorrow.0

-

Ciprico said:

Ned... Could you give some examples of money market funds... Or point me towards a list...NedS said:

Do you specifically want to hold NS&I products in a SIPP, or do you just want any risk free 4% return for cash in your SIPP? If it's just the latter, there are money market funds that will give you near BoE base rate at very low risk, or if you prefer a fixed rate product, consider individual government gilts (although not yet yielding 4%)Ciprico said:Any one know of a SIPP that can hold these NSI products...

It seems Interactive Investor don't, but do any of the major platforms....

From: https://www.nsandi-adviser.com/sipps-and-ssassSIPP and SSAS schemes may allow investment into some NS&I products. These are known as ‘permitted investments’ held by the scheme trustee. Before recommending NS&I investments we suggest you check that the SIPP or SSAS provider will accept them, and that the investment will not be subject to tax penalties on any gains.

Our investments that may be held in a SIPP or SSAS are:

- Fixed Interest Savings Certificates

- Index-linked Savings Certificates

- Guaranteed Growth Bonds

- Guaranteed Income Bonds

- Income Bonds

Thanks...@Ciprico Here is a search on HL for "Money Market" and "Short Term Money Market" funds:https://www.hl.co.uk/funds/fund-discounts,-prices--and--factsheets/search-results?sectorid=123,138&start=0&rpp=20&lo=0&sort=fd.full_description&sort_dir=asc

I am a Forum Ambassador and I support the Forum Team on the Benefits & tax credits, Heat pumps and Green & Ethical MoneySaving forums. If you need any help on those boards, do let me know. Please note that Ambassadors are not moderators. Any post you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own & not the official line of Money Saving Expert.0 -

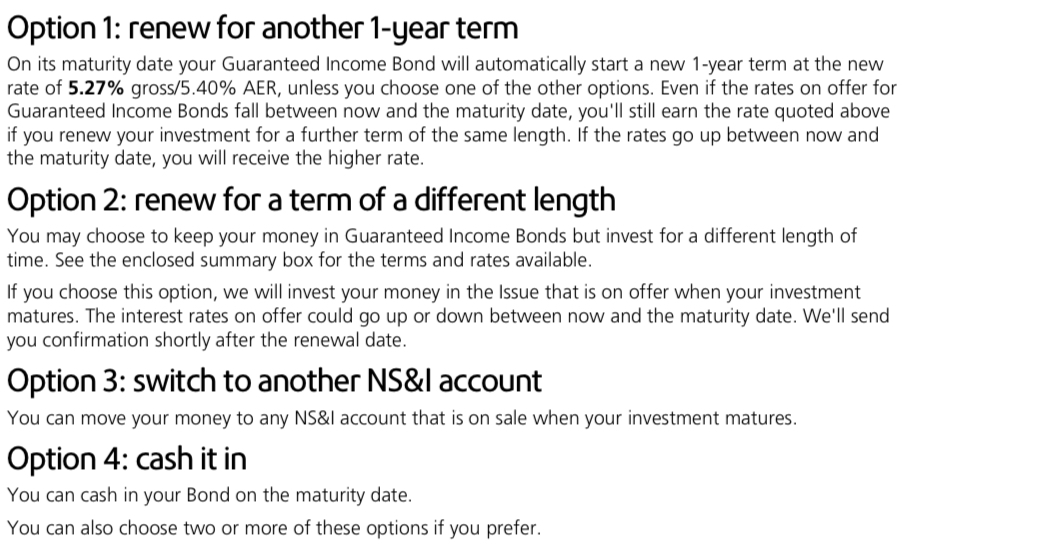

I’ve received the first maturity letter (out of 3) from NS&I for the Guaranteed Income Bond I opened in February 2023.

If I let it auto-renew (default option) the new 1-year rate will be 5.27% gross/5.40% AER.

As things stand at the moment, it seems to be a good rate of interest for a 1-year term.

4 -

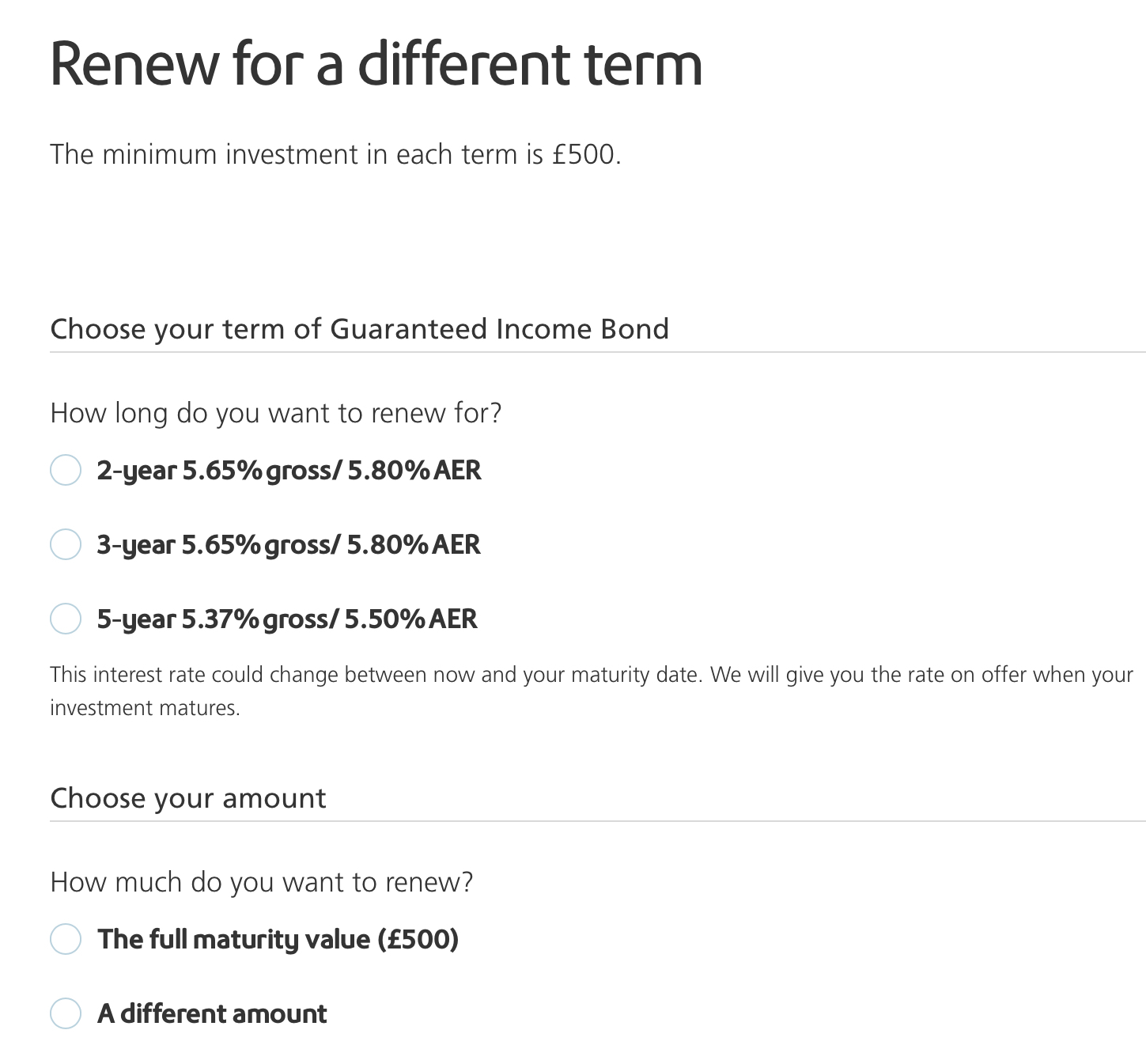

I've got one maturing early February too @GalacticaActual - I downloaded their document with maturing terms a week or two ago when I was digging around for what they might be offering and it was 5.65% gross for 2 and 3 year terms - which would be of interest to me - are those the terms still being offered in your email? The document doesn't appear to have changed since I looked and it's dated 4th December.

Although I note that your posted graphic shows that they'll offer different lengths of bonds at the prevailing rate on maturity day - which with a month to go, could well drop by then.1 -

Hello BooJewels, I have just checked my online messages and the second bond maturity letter was available to view (the first two bonds I purchased were on the 3rd and 4th February 2023 for £500 each). The other bond matures on the 7th February 2024, which is for several thousand pounds.BooJewels said:I've got one maturing early February too @GalacticaActual - I downloaded their document with maturing terms a week or two ago when I was digging around for what they might be offering and it was 5.65% gross for 2 and 3 year terms - which would be of interest to me - are those the terms still being offered in your email? The document doesn't appear to have changed since I looked and it's dated 4th December.

Although I note that your posted graphic shows that they'll offer different lengths of bonds at the prevailing rate on maturity day - which with a month to go, could well drop by then.

The options to renew for a different term are shown below for the first two £500 bonds:

3

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards