We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Are fixed savings account rates driven by the bond market or the BoE base rate?

RG2015

Posts: 6,220 Forumite

I recently heard a finance "expert" saying it was a popular myth that consumer interest rates were driven by the BoE base rate, and in fact they followed the bond market.

I am not qualified in any way to comment on the veracity of this claim. I suspect that there may be some truth in this but that there are far more factors involved. However it is a fact that bond rates have surged recently following recent government announcements.

It is also a fact that 1, 2 and 3 year fixed savings rates have also increased noticeably over the last week or so. More recently some of the highest rate fixes have been withdrawn as bond rates have eased. Coincidence or is it just that their targets have been met with the increased uptake. Again probably a mix of both and more.

I am now wondering whether fixed rates will once again increase with the expected BoE November and December rate hikes. I am looking at no more than one year which is now at about 4.31% with Charter Savings Bank for £5k+.

Can I realistically expect 5% in November or December, assuming no significant increase in bond market rates?

I am not qualified in any way to comment on the veracity of this claim. I suspect that there may be some truth in this but that there are far more factors involved. However it is a fact that bond rates have surged recently following recent government announcements.

It is also a fact that 1, 2 and 3 year fixed savings rates have also increased noticeably over the last week or so. More recently some of the highest rate fixes have been withdrawn as bond rates have eased. Coincidence or is it just that their targets have been met with the increased uptake. Again probably a mix of both and more.

I am now wondering whether fixed rates will once again increase with the expected BoE November and December rate hikes. I am looking at no more than one year which is now at about 4.31% with Charter Savings Bank for £5k+.

Can I realistically expect 5% in November or December, assuming no significant increase in bond market rates?

1

Comments

-

There does seem to be a belief on this forum that fixed rates are "the base rate plus a bit".I'd say it's much more to do with the bond market than the base rate at any given time.

But in turn the bond market is, to some extent, a forecast of what the base rate will be.Normally fixed rates will be a bit higher than immediate, because of the risk of locking your money up.But that shouldn't be confused with "fixed rates are the current base rate plus 2%" or whatever.The market is already expecting base rates to go up, so fixed rates will largely take that into account.That said, bank funding has seized up somewhat, and fixed rates haven't caught up to that.If two year mortgage average over 6%, and the rate banks charge each other to lend is 5.2% (SONIA), it's egregious that the best 2-year fix is 4.6% regular cash or 4% in an ISA.As to whether rates will creep up to more like 5%, or the government and Bank of England will do something to bring SONIA and mortgages down, we will see...2 -

RG2015 said:

It is also a fact that 1, 2 and 3 year fixed savings rates have also increased noticeably over the last week or so. More recently some of the highest rate fixes have been withdrawn as bond rates have eased. Coincidence or is it just that their targets have been met with the increased uptake. Again probably a mix of both and more.This is definitely a coincidence as it is not the first time we've seen that behaviour this year.The main driver of savings interest rates are the savings institution's ability to lend the money they attract profitably and competition between themselves and their competitors to attract this money. Supply and demand, with their underlying lending activities setting a ceiling.2 -

Just to clarify, are you saying that the the surge in bond rates has not driven the recent increase in 1 to 3 year fixed rates?masonic said:RG2015 said:

It is also a fact that 1, 2 and 3 year fixed savings rates have also increased noticeably over the last week or so. More recently some of the highest rate fixes have been withdrawn as bond rates have eased. Coincidence or is it just that their targets have been met with the increased uptake. Again probably a mix of both and more.This is definitely a coincidence as it is not the first time we've seen that behaviour this year.The main driver of savings interest rates are the savings institution's ability to lend the money they attract profitably and competition between themselves and their competitors to attract this money. Supply and demand, with their underlying lending activities setting a ceiling.0 -

That is exactly what I am saying. There was also a surge in mortgage rates and a sizeable shift in forward projections for the BoE base rate.RG2015 said:

Just to clarify, are you saying that the the surge in bond rates has not driven the recent increase in 1 to 3 year fixed rates?masonic said:RG2015 said:

It is also a fact that 1, 2 and 3 year fixed savings rates have also increased noticeably over the last week or so. More recently some of the highest rate fixes have been withdrawn as bond rates have eased. Coincidence or is it just that their targets have been met with the increased uptake. Again probably a mix of both and more.This is definitely a coincidence as it is not the first time we've seen that behaviour this year.The main driver of savings interest rates are the savings institution's ability to lend the money they attract profitably and competition between themselves and their competitors to attract this money. Supply and demand, with their underlying lending activities setting a ceiling.

2 -

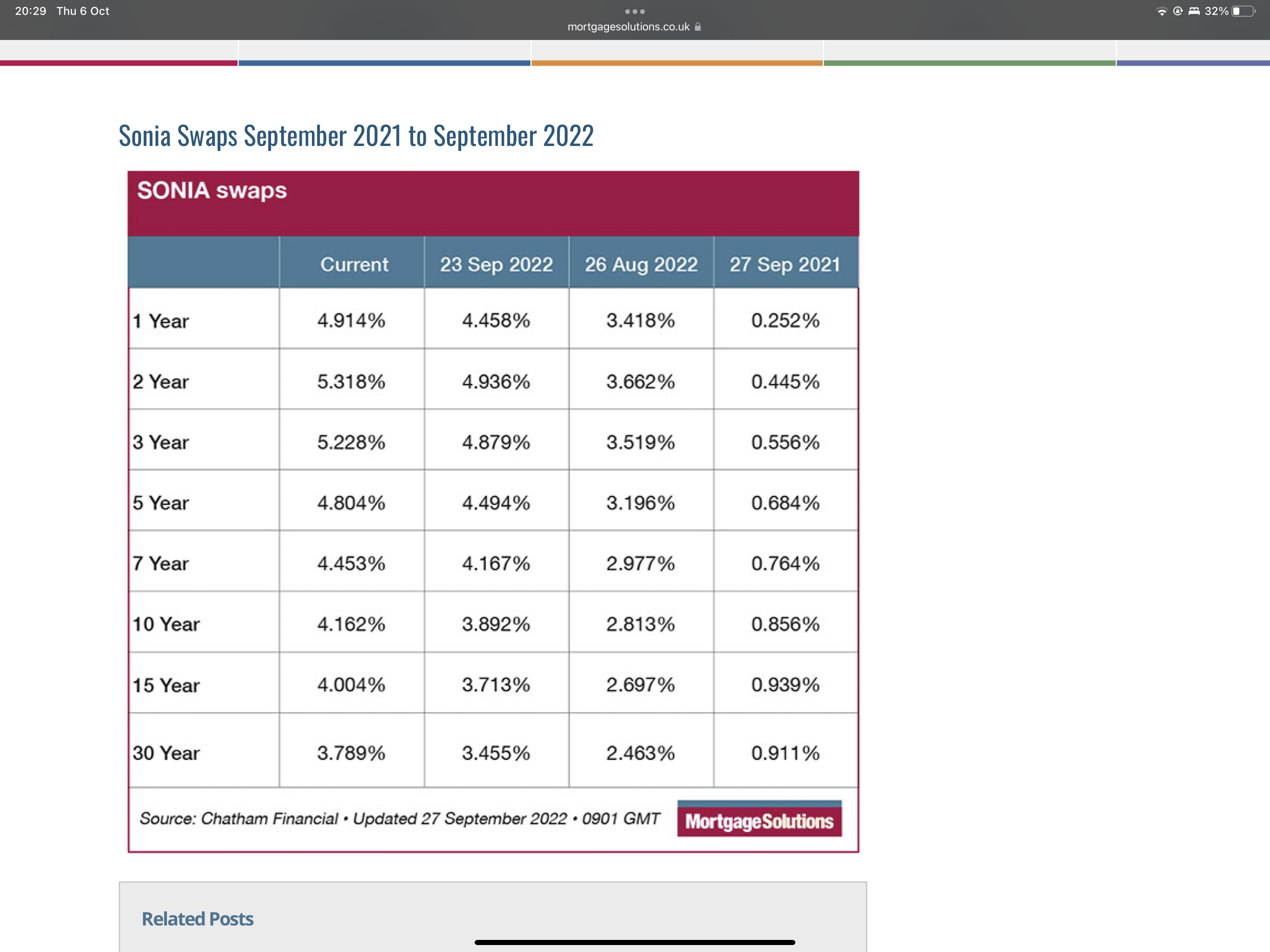

At the time of the financial crisis people in the know were always talking about how mortgage swap rates can drive deposit rates and I've heard them mentioned again in the past couple of weeks.

"Swap rates are based off market assumptions surrounding what interest rates will be over the term of the swap rate, the calculation of which involves a number of factors.They’re all based off current assumptions, so factors like inflation, the conflict in Ukraine, prices, fuel, gas prices and the general economy, will feed into where those forecasts come from.”"

https://www.mortgagesolutions.co.uk/news/2022/05/19/the-lowdown-on-swap-rates-explainer/

The table below is a little out of date but it gives you an idea of how they've changed in the past year.

https://www.mortgagesolutions.co.uk/news/2022/09/27/uk-mortgage-lenders-freeze-in-pricing-dilemma-as-swap-rates-surge/ 3

3 -

Useful, thanks. So today's 3 year swap rate at 5.166% reflects market assumptions that BoE rates will top out at 5.7% next year? In that case the current nationwide 4.75% 3 year fix looks pretty good and whilst it may be beaten, it's unlikely to be beaten by much unless the current assumptions change?wmb194 said:At the time of the financial crisis people in the know were always talking about how mortgage swap rates can drive deposit rates and I've heard them mentioned again in the past couple of weeks.

"Swap rates are based off market assumptions surrounding what interest rates will be over the term of the swap rate, the calculation of which involves a number of factors.They’re all based off current assumptions, so factors like inflation, the conflict in Ukraine, prices, fuel, gas prices and the general economy, will feed into where those forecasts come from.”"

https://www.mortgagesolutions.co.uk/news/2022/05/19/the-lowdown-on-swap-rates-explainer/

The table below is a little out of date but it gives you an idea of how they've changed in the past year.

https://www.mortgagesolutions.co.uk/news/2022/09/27/uk-mortgage-lenders-freeze-in-pricing-dilemma-as-swap-rates-surge/0 -

The only thing driving consumer interest rates, is the desire for retail banks to make money.RG2015 said:I recently heard a finance "expert" saying it was a popular myth that consumer interest rates were driven by the BoE base rate, and in fact they followed the bond market.

It's generally harder for them to do that in the economic conditions that lead to a low base rate & easier in the economic conditions that lead to a higher base rate.

Tracker mortgages are the only thing driven by BoE base rate & the money they borrow to lend to you isn't usually borrowed at BoE base rate either.2 -

I wouldn't commit to any fixed rate before halloween. Everything is still priced on the assumption that the government can convince the market they can balance the books, if they can't then it's going to be brutal.Bobziz said:

In that case the current nationwide 4.75% 3 year fix looks pretty good and whilst it may be beaten, it's unlikely to be beaten by much unless the current assumptions change?

2 -

I heard a chap on the radio today saying that variable rate mortgage rates followed the BoE rate and fixed mortgage rates followed bond rates.

I hadn’t heard that before but it makes sense.0 -

RG2015 said:I heard a chap on the radio today saying that variable rate mortgage rates followed the BoE rate and fixed mortgage rates followed bond rates.

I hadn’t heard that before but it makes sense.It doesn't make sense to me. The money banks use to fund fixed mortgages isn't usually obtained by from them issuing corporate bonds. The rate an institution can borrow at in bond markets is driven largely by their own credit rating. Did the chap on the radio give an explanation as to why bond markets have anything to do with mortgage lending?Tracker mortgage rates follow the BoE base rate, but other types of variable rate mortgages are often disconnected from changes to the base rate. Only those with tracker mortgages saw their rates follow the base rate down to historic lows in 2008-9.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards