We'd like to remind Forumites to please avoid political debate on the Forum... Read More »

We're aware that some users are experiencing technical issues which the team are working to resolve. See the Community Noticeboard for more info. Thank you for your patience.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

L and G to Fidelity

Options

Comments

-

Frank241 said:Can anyone offer me some advice as to whether this is normal/acceptable, and whether I should cut my losses and close this ISA and move on? Many thanks.It will be down to the performance of the underlying investment(s) rather than if the ISA wrapper is with L&G or Fidelity. I understood that in most or all cases the customers would have stayed in the same investment with the charges adjusted such that at least for the first year the overall cost of ownership is not higher.Which funds(s) are you invested in? My guess is that you are holding low to moderate risk funds with a material allocation to fixed interest bonds which have been steadily rising in recent years until this year when their asset valuations have been steadily falling as they are less attractive in an era of higher inflation. This is essentially reversing out some of the capital growth you should have seen in previous years when the return on bonds was higher than their underlying fixed interest payments.

2 -

Since then, it has steadily gone down, and is now worth £7,723.88. While I understand there are market fluctuations and shares can go up or down in value, a £425 loss for someone like me is a catastrophe really, and seems an incredibly high loss based on my past experience with ISAs, having had many for most of my adult life.That is a tiny loss of 5.2%. You say its a high loss based on your past experience of ISAs (I assume that means investing). You say you have had many for most of your adult life. Yet that is not consistent with reality. Perhaps you were not looking previously when negative events occured.

Obviously, the scale of losses will depend on your risk profile and you haven't actually mentioned anything about what investments you hold. However, here is some recent history....

2020 - Markets fell 35%

2018 - 20% drop at the end of the year

2015/16 - 20% drop over that period

2008/9 - 45% drop

2000-2003 - 43% drop.

And many periods of 5-10% losses in the last 22 years.I've never encountered such a steady haemorrhage from an ISA before.5% is not a haemorrhage. it's a minor negative.I have contacted Fidelity for advice, but they refuse to give any, as is their policy apparently, and they simply cite market fluctuation as the cause.Fidelity are not advisers and do not hold the regulatory permissions to give advice. If you want advice, you would employ an IFA.Can anyone offer me some advice as to whether this is normal/acceptable, and whether I should cut my losses and close this ISA and move on?If a tiny 5% loss is catastrophic for you then it indicates a couple of things

1 - you don't have enough money to be investing

2 - you don't have sufficient investment knowledge and understanding to be investing

My gut feeling is that you have gone heavy in gilts and fixed interest securities. However, to be sure, you need to tell us what you have invested in. And tell us why you invested in that fund(s).

Gilts and fixed interest securities have had over a decade of above long term average returns. That cycle is over and it is reversing. There is going to be no such thing as low risk investing for the next decade. You are probably looking at a balance of cash savings and then 100% equities to control your volatility. There may come a point where the natural yield of fixed interest securities will be high enough to counter the unit price decline before then but as things currently stand, you don't want to be heavy in fixed interest securities.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.3 -

It's just a coincidence that markets have turned a bit negative in the last few months after a few years of steady growth .

As said a 5% drop is a pinprick in investing terms .1 -

For many years now warnings are clearly given on all investment product literature.Frank241 said:Hi. I'm new here so I apologise if I'm going over old ground. I was transferred to Fidelity from L&G last December. I have a stocks and shares ISA, which at that point was worth £8,163.25. Since then, it has steadily gone down, and is now worth £7,723.88. While I understand there are market fluctuations and shares can go up or down in value, a £425 loss for someone like me is a catastrophe really, and seems an incredibly high loss based on my past experience with ISAs, having had many for most of my adult life. I've never encountered such a steady haemorrhage from an ISA before. Every time I check the balance, it has gone down. While with L&G, despite flatlining at times it never made a loss as far as I can remember. I have contacted Fidelity for advice, but they refuse to give any, as is their policy apparently, and they simply cite market fluctuation as the cause.

Can anyone offer me some advice as to whether this is normal/acceptable, and whether I should cut my losses and close this ISA and move on? Many thanks.

The value of investments and the income you get from them may fall as well as rise and there is no certainty that you will get back the amount of your original investment. You should also be aware that past performance may not be a reliable guide to future performance.

1 -

MX5huggy said:What is the ISA actually invested in? That is the name of the fund.If a 5% loss in value over short term is “catastrophic” then Stocks and Share ISA is not for you. What are your long term aims for this saving?

Thanks for your responses. 'Legal & General Mixed Investment 40-85%' is the name of the fund. 'Catastrophic' was a poor choice of word perhaps. I'm merely saying it's a lot of money to me. My long term aims are to try to accumulate enough for a deposit on a house. I have other investments outside of this one, which is the only stocks and shares ISA that I have.Alexland said:Frank241 said:Can anyone offer me some advice as to whether this is normal/acceptable, and whether I should cut my losses and close this ISA and move on? Many thanks.It will be down to the performance of the underlying investment(s) rather than if the ISA wrapper is with L&G or Fidelity. I understood that in most or all cases the customers would have stayed in the same investment with the charges adjusted such that at least for the first year the overall cost of ownership is not higher.Which funds(s) are you invested in? My guess is that you are holding low to moderate risk funds with a material allocation to fixed interest bonds which have been steadily rising in recent years until this year when their asset valuations have been steadily falling as they are less attractive in an era of higher inflation. This is essentially reversing out some of the capital growth you should have seen in previous years when the return on bonds was higher than their underlying fixed interest payments.Albermarle said:It's just a coincidence that markets have turned a bit negative in the last few months after a few years of steady growth .

As said a 5% drop is a pinprick in investing terms .

Thanks. Perhaps I am panicking unnecessarily. Comforting words.

Many thanks. I think you're correct in saying that I may have not noticed previous years ups and downs as much. Perhaps the fact that I have seen this loss is making me check the investment's value more often than I would have normally, and that may be giving me a skewed impression of it's performance.dunstonh said:Since then, it has steadily gone down, and is now worth £7,723.88. While I understand there are market fluctuations and shares can go up or down in value, a £425 loss for someone like me is a catastrophe really, and seems an incredibly high loss based on my past experience with ISAs, having had many for most of my adult life.That is a tiny loss of 5.2%. You say its a high loss based on your past experience of ISAs (I assume that means investing). You say you have had many for most of your adult life. Yet that is not consistent with reality. Perhaps you were not looking previously when negative events occured.

Obviously, the scale of losses will depend on your risk profile and you haven't actually mentioned anything about what investments you hold. However, here is some recent history....

2020 - Markets fell 35%

2018 - 20% drop at the end of the year

2015/16 - 20% drop over that period

2008/9 - 45% drop

2000-2003 - 43% drop.

And many periods of 5-10% losses in the last 22 years.I've never encountered such a steady haemorrhage from an ISA before.5% is not a haemorrhage. it's a minor negative.I have contacted Fidelity for advice, but they refuse to give any, as is their policy apparently, and they simply cite market fluctuation as the cause.Fidelity are not advisers and do not hold the regulatory permissions to give advice. If you want advice, you would employ an IFA.Can anyone offer me some advice as to whether this is normal/acceptable, and whether I should cut my losses and close this ISA and move on?If a tiny 5% loss is catastrophic for you then it indicates a couple of things

1 - you don't have enough money to be investing

2 - you don't have sufficient investment knowledge and understanding to be investing

My gut feeling is that you have gone heavy in gilts and fixed interest securities. However, to be sure, you need to tell us what you have invested in. And tell us why you invested in that fund(s).

Gilts and fixed interest securities have had over a decade of above long term average returns. That cycle is over and it is reversing. There is going to be no such thing as low risk investing for the next decade. You are probably looking at a balance of cash savings and then 100% equities to control your volatility. There may come a point where the natural yield of fixed interest securities will be high enough to counter the unit price decline before then but as things currently stand, you don't want to be heavy in fixed interest securities.

Really? I hadn't seen those. Thanks for enlightening me. Very helpful.Thrugelmir said:For many years now warnings are clearly given on all investment product literature.

The value of investments and the income you get from them may fall as well as rise and there is no certainty that you will get back the amount of your original investment. You should also be aware that past performance may not be a reliable guide to future performance.0 -

What do you consider to be long term, and does your investing profile align with that timeframe? If it's to be your first property and you're young enough, are you using a Lifetime ISA?Frank241 said:

'Catastrophic' was a poor choice of word perhaps. I'm merely saying it's a lot of money to me. My long term aims are to try to accumulate enough for a deposit on a house. I have other investments outside of this one, which is the only stocks and shares ISA that I have.0 -

. 'Legal & General Mixed Investment 40-85%' is the name of the fund.Here is the past performance of that fund over the last 6 months, 1 year, 5 years and since launch.

From this, you can see plenty of zigzagging.'Catastrophic' was a poor choice of word perhaps. I'm merely saying it's a lot of money to me. My long term aims are to try to accumulate enough for a deposit on a house.How far are you away from wanting to buy?

An economic cycle is around 15 years nowadays (used to be closer to 10). So, unless you are investing for a whole cycle, you are taking some risk that the money will be lower when you need it. Realistically, the majority of 5 year periods result in an excess. Although there have been a very small number of 5 year periods where losses have occurred. This is why you often see advice that says a minimum of 5 years.

if you want to buy in less than 5 years time, then you shouldn't really be investing.Perhaps the fact that I have seen this loss is making me check the investment's value more often than I would have normally, and that may be giving me a skewed impression of it's performance.In the past, people used to get an annual statement. They wouldn't look at it beyond that. If you look at it annually, then there have only four negative years in the last 21 calendar years (2018, 2008,2002,2001).

The majority of negative periods are short term and recover inside the year. A minority will take longer. The worst of which can take 5 years or in extreme, very rare events, longer.

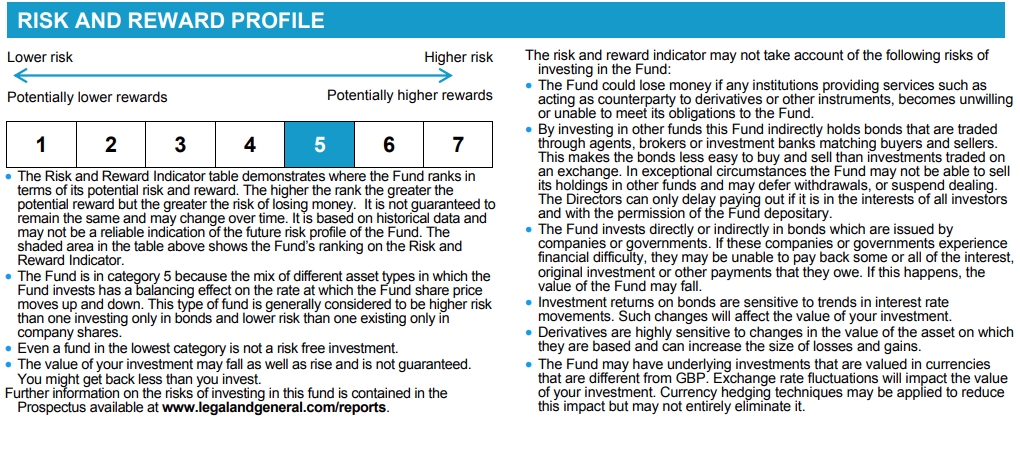

If you check the values often, you get to see all those daily ups and downs and that can be bad for your health during negative periods. You cannot take the long term gains without accepting the short term losses.Really? I hadn't seen those. Thanks for enlightening me. Very helpful.All investment documents have it. Advised investments would be more prominent but non-advised still have them but you need to read it. The L&G KIID, which you confirm you have read when you buy the fund says this:

edit: the board software compressed the image and made it a bit blurry but you can make out the warnings.I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 350.8K Banking & Borrowing

- 253.1K Reduce Debt & Boost Income

- 453.5K Spending & Discounts

- 243.8K Work, Benefits & Business

- 598.7K Mortgages, Homes & Bills

- 176.8K Life & Family

- 257.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.6K Read-Only Boards